Have you found out which bank offers the best interest rate for a savings account from which you can withdraw money anytime? Euribor is soon at 3% levels, at which point even a savings account can yield quite a decent return, at least nominally.

11 Likes

Svea 1.15%. They say it’s the highest.

edit. Now they say it’s competitive

3 Likes

You can get an interest rate of 1.6% on Nordea’s JoustoTalletus (Flexible Deposit) account. The savings period is 12 months, the money is freely available, and interest is paid according to the lowest balance during the savings period.

7 Likes

Is this a new product from Nordea?

Seems good, but the terms and conditions stated the following:

“The bank determines the minimum and maximum deposit amount for each Flexible Deposit (JoustoTalletus) period. If the account balance falls below the minimum amount during the Flexible Deposit period, no deposit interest will be paid for that Flexible Deposit period. If the account balance exceeds the maximum amount during the Flexible Deposit period, no deposit interest will be paid for the exceeding amount for that Flexible Deposit period. If the account agreement expires during the Flexible Deposit period, no deposit interest will be paid for the current Flexible Deposit period.”

The bank also has the right to change the terms and conditions and the price list.

1 Like

Hypo:

The return on the deposit is agreed upon in advance, and for Hypo Tuotto fixed-term accounts, we can currently offer the following fixed interest rates:

- 6 months - 1.3%

- 12 months - 1.9%

- 24 months - 2.0%

The minimum deposit is 10,000 euros. Hypo’s fixed-term deposits are covered by the Finnish deposit guarantee scheme.

1 Like

The minimum and maximum amount for the period refers to a range defined by the bank itself, within which one must operate. For the current period on sale, the minimum is 500 euros, and the maximum is 100,000 euros. The account cannot have funds above or below this range.

Example 1:

If you deposit 10,000 euros into the account and keep the money in the account for a year, you will receive interest based on 10,000 euros after the end of the period.

Example 2:

If you deposit 10,000 euros into the account and later deposit an additional 5,000 euros, you will receive interest based on 10,000 euros (the lowest balance during the period) after the end of the period.

Example 3:

If you deposit 10,000 euros into the account and later withdraw 5,000 euros from the account, you will receive interest based on 5,000 euros after the end of the period.

Example 4:

If you deposit 10,000 euros into the account and later withdraw 5,000 euros from the account and then deposit an additional 2,000 euros, you will receive interest based on 5,000 euros (the lowest balance during the period) after the end of the period.

Example 5:

If you deposit 10,000 euros into the account and later withdraw 9,600 euros from the account, the amount in the account will fall below the allowed minimum amount (500 euros), and thus no interest will be paid at all, and the account agreement will terminate.

6 Likes

Too complex a product when simpler ones are available (at least from other banks). Investing should be simple, not complicated.

3 Likes

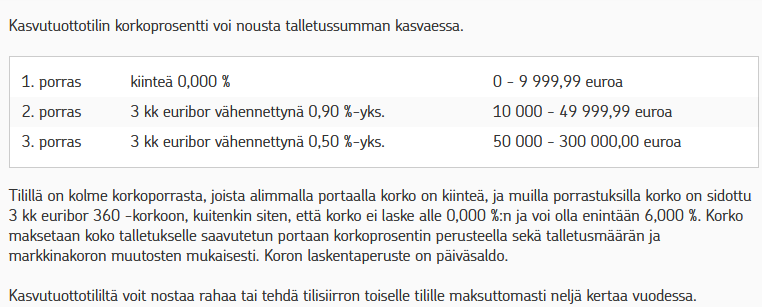

OP’s Kasvutuotto account:

The 3-month Euribor is currently ~1.97%, meaning the interest for €50k would be ~1.5%.

OP’s fixed-term Tuottotili, on the other hand, seems to give 1.5% for as little as €10k if taken for a year (this is a fixed-term account – no withdrawals allowed).

7 Likes

The same interest rate tiers apply to OP Kerrostuotto (OP Apartment Yield) as well.

You can withdraw and deposit unlimitedly, free of charge.

The only difference seems to be in the calculation method for interest capital, i.e., the average deposit of the calendar month, whereas OP Kasvutuotto (OP Growth Yield) uses the daily balance.

This is used as a so-called second account so that not everything is in the debit card account, easy to transfer as needed.

I also kept tax refunds there.

5 Likes

In principle, the best return would probably come from investing in a short-term bond fund that holds the bonds until maturity. For example, Seligson’s money market fund might fit the bill, and quite a few people have used it as a savings account.

OP’s 3-month Euribor -0.5% is relatively good, but still quite a hefty “cost” when you also have to put in 50k.

The downside of funds, of course, is that even with short-term rates, you get small daily fluctuations.

That Seligson Money Market Fund is pretty lackluster, with fees of 0.18% per year:

I haven’t ventured into those funds; some crash just happens to occur when there’s more money in them.

1 Like

With the rise in key interest rates, interest rates on savings accounts, and especially fixed-term deposit accounts, have also been slowly increasing. Among savings accounts, Svea now offers 1.15% and BROCC offers 1.1%. Apparently, Bigbank offers 2.1%/12 months for fixed-term deposits, but of course, a bank like Hypo might be a more reliable option. Banks’ “flexible accounts” offer quite decent returns, but if you make many withdrawals, the returns will plummet accordingly.

However, interest rates are expected to continue to rise, so better returns are likely in store. Let’s monitor the situation.

Did you expect a fund aiming for short-term interest market returns to do anything other than lose money in a zero and negative interest rate market? Besides, the 0.18% annual fee is included in those figures. It has performed quite well, considering what one gets from short-term interest. When I had a cash reserve there before zero interest rates, the return was pretty much in line with the 3-month Euribor return. Now that short-term interest rates have risen again, the return has also turned positive (1-day and 1-month).

In my opinion, it’s better than OP’s 3-month Euribor - 0.5% or 0.9%. And there are no subscription/redemption restrictions. The only downside is that it’s not covered by deposit protection. So, if several banks were to go bust, you could theoretically lose capital in it.

2 Likes

I think Kerrostuotto is only for Private customers?

1 Like

Well, look at that, Kerrostuotto is no longer among OP’s account options. It’s been there for several years; back then, you could get it as a second account even as a basic customer.

Svea 1.3% from Dec 15.

3 Likes

Interest rates on Nordea fixed-term deposit accounts today:

6 months - 1.30%

12 months - 1.50%

Flexible deposit account 1.60%, but interest is calculated based on the lowest balance of the year and the account cannot be emptied except by closing the entire account.

The best fixed-term deposit accounts still seem to be at the Finnish branch of the Estonian Bigbank (covered by deposit protection):

- 1-5 months 1.0 %

- 6-11 months 1.5 %

- 12-23 months 2.1 %

- 2-10 years 2.5 % / 2.45 %

The lower interest rate applies when interest is paid annually rather than at the end of the deposit term.

1 Like

Svea’s interest rate is rising at a good pace, considering the previous rate hike was only two weeks ago. Personally, I’ve been quite satisfied; it’s a no-nonsense place to park liquidity for a rainy day, providing at least some small consolation against the bite of inflation.

10 Likes

How often has Svea raised interest rates towards the end of this year? I noticed that Bank Norwegian raised them once on 4.11.22 from 0.75% → 1.05%. I’m wondering if Svea is a bit more agile in this regard in a rising interest rate environment.

A small nuance is that Svea seems to withhold taxes directly from the interest, but BN does not; instead, it’s handled during final taxation.