Outokumpu is indeed in favor of the project, with the following development suggestions.

Apparently, that third suggestion refers to the idea that EU requirements for components should also apply to the steel they contain.

Outokumpu further encourages the Commission to

introduce an EU low-carbon steel label, which would enable steel manufacturers to demonstrate their products’ carbon dioxide emissions and help buyers choose cleaner materials,

introduce low-carbon criteria for stainless steel as well, so that the criteria take into account differences in manufacturing processes and also consider the high emissions in the supply chain, and

expand Made in EU requirements to also cover steel, as excluding products containing steel from the list of preferred European products can lead to high-emission steel being imported into Europe, resulting in final products with a large carbon footprint being manufactured here.

Here are some more comments from the EU steel lobbyist Eurofer regarding the steel-related aspects of the Industrial Accelerator Act.

The hope is for a tighter framework to ensure the involvement of EU companies, presumably in case the CBAM (Carbon Border Adjustment Mechanism) and tariff reforms are bypassed. The EU has a tendency to be a bit naive, so there really should be more foolproof systems, considering that today’s global trade policy and geopolitics are what they are—i.e., heading in a different direction than before.

Edit: It’s worth noting that according to this, the IAA would only require a 25% low-carbon share in public procurement, which would correspond to about 5% of total consumption. This could also be based on non-EU trade agreements.

The proposal offers some welcome foundations that could stimulate demand for low-carbon steel.

But the demand signal remains limited.

The proposal requires 25% of steel in public procurement and public support schemes to be low-carbon - yet it does not require that this steel be produced in Europe.

This matters.

25% of public procurement represents less than 5% of the total steel market, and public support schemes vary widely across Member States.

Without stronger and clearer demand signals, these measures may not provide the long-term certainty needed for major industrial investments.

To make lead markets work, the EU must ensure it supports low-carbon steel made in Europe, not made in third-countries.

The Industrial Accelerator Act is a welcome start - but it must go further to increase demand for green steel made in Europe.

EUROFER therefore calls for:

a clear definition of “Made in Europe” for steel, based on steel melted and poured in the EU and EEA the application of both low-carbon and European origin criteria in the Industrial Accelerator Act a robust labelling framework to support lead markets affordable electricity prices to further enable steel decarbonisation.

After years of adjusting the Carbon Border Adjustment Mechanism (CBAM), the EU has realized that carbon leakage does not only occur at the raw material level, but also at the product level.

This is an obvious issue that could have been addressed when CBAM was being designed and implemented.

However, some kind of plan is emerging, with a timeline of January 1, 2028, which is just over 1.5 years away.

It is reassuring, however, that now that a fix is known to be in the works, an EU producer no longer needs to flee in terms of EU demand, and on the other hand, an importer has time to make investment decisions regarding their production if they wish.

It is still personally unclear to me whether an EU producer’s exports outside the EU are burdened by the EU’s carbon regulations and their fees.

These are typically higher than elsewhere in the world, and at the same time, EU producers’ competitors live quite leisurely in terms of the carbon world, not only for raw materials but also for the entire rest of the ecosystem…

According to the draft, a broad group of products particularly those with high steel and aluminum content will be included in the mechanism as of January 1, 2028. Within this scope, many items will fall under CBAM obligations, including fasteners such as screws, bolts, and nuts, as well as pipes, tanks, construction components, and railway materials. In addition, more complex products such as engines, pumps, white goods, industrial machinery, electrical equipment, and certain commercial vehicles will also be covered.

It’s said that steel 232s are being adjusted.

IF I understand Fast Markets’ interpretation correctly, then in Calvert, the melted & poured roster can come from Mexico with lower tariffs. And if the final products have sufficiently few metals, the metal content is no longer sanctioned by 232 tariffs.

And metal-intensive products will not enjoy 50% tariffs on their metal content, but 25% tariffs on the full value of the entire product.

It’s difficult to say what all this would mean for Outsa’s Americas/MX segment, or if it means anything in practice…

But I suppose this will become clear at the latest during the earnings call, which isn’t until May 12th.

Also, “products made abroad but entirely with American steel, aluminium and copper will be subject to lower tariffs of 10%,” according to the proclamation, and products made of 15% or less steel, aluminium or copper will no longer be subject to Section 232 metals tariffs.

Derivative articles substantially made of steel, aluminium or copper will pay a flat 25% duty on their full value, according to the presidential proclamation on Thursday, a departure from the previous method of collecting 50% tariffs on just the metals component of a product imported into the US.

The EU’s new restrictions are moving forward. Negotiators from the Council and Parliament have reached an agreement and will proceed to votes in May. The new, stricter restrictions will come into force after the current ones expire, i.e., on July 1, 2026.

In connection with Aperam, Jefferies estimates that CBAM and new EU trade defense measures will bring an approx. €200m EBITDA increase (pricing, capacity utilization).

Aperam’s EBITDA (2025: €340m) is estimated to rise to €484m in 2026 and €650m in 2027.

Significant increases, then, and logically Outokumpu Europe will enjoy similar benefits.

The steelmaker is projected to see up to €200 million in EBITDA gains from European Union policies, including the Carbon Border Adjustment Mechanism (CBAM) and new trade defense measures.

These policies are expected to support pricing and utilization starting in the second half of 2026, with a potential utilization uplift of 7% to 10%.

For the full year 2026, Jefferies estimated EBITDA at €484 million, rising to €650 million in 2027. First-quarter 2026 EBITDA is expected to reach €86 million, up from €67 million in the previous quarter, driven by seasonal volume recovery in Europe.

This improvement comes despite mid-single-digit million-euro headwinds from higher energy costs.

Significant impacts estimated for Aperam’s profitability. A similar effect is also seen for Outokumpu; the earnings level is now set to take a leap. Earnings forecasts and target prices will continue on an upward trend. Outokumpu also commented today on the development of EU safeguard measures.

I still can’t help but be amazed, however, that the EU—which has been able to talk about carbon leakage forever—has still left such basic products as pipes, steel wires, or steel bars out of the new legislation…

If things are as Outokumpu mentions in its release.

A clear change from the old:

-melted & poured rule

-roughly halving the tariff-free quota

-roughly doubling the tariff on imports exceeding the tariff-free quota

While free trade is a good principle, it is nonsensical to be the sole torchbearer.

The unpredictability of 2020s geopolitics has proven this once and for all.

Six months after the regulation enters into force, the Commission will evaluate whether the scope should be extended to cover additional steel products, such as pipes, certain steel wires, or forged steel bars, and may propose legislative changes if necessary.

Long Products was sold, of course; I was mainly thinking from the perspective that protected stainless steel isn’t needed in Europe if processed goods made of stainless steel are imported into Europe.

Pipes and other quite basic products would, in my opinion, have been fairly easy to include.

Then a more complex story is products that contain stainless steel and steel, such as washing machines.

The Americans certainly knew how to take this into account, and it’s no more complicated than requiring importers to provide a breakdown of raw materials according to a bill of materials and applying tariffs. At least that’s what I remember from Harvia’s sauna heater business. The tariff on steel to the US is higher than on the heater.

Analysts are currently quite optimistic about stocks’ future, which is also reflected in Outokumpu’s share price performance. However, forecasting institutions do not share the same view – for example, the International Monetary Fund has even hinted at a recession risk. Geopolitical risks still exist, although the escalation of the situation in Iran has calmed down for now.

Outokumpu’s stock is indeed supported by several factors: EU safeguards, Germany’s stimulus package, and expectations of growing defense investments. A significant reduction in short positions may also contribute to price formation.

The question arises: is the chrome mine already priced into the current share price? If plans for chrome processing progress, could spinning off the mining operations and listing them as a separate public company create more shareholder value? Chrome production and processing differ significantly as a business from stainless steel manufacturing, so a separation could make the mine’s value more visible.

In any case, the role of shorters has clearly diminished Outokumpu is no longer among the most shorted companies, and there is only one shorter left on the Financial Supervisory Authority’s (Finanssivalvonta) list. The share of shorted stocks has dropped to approximately 0.51 percent of all shares.

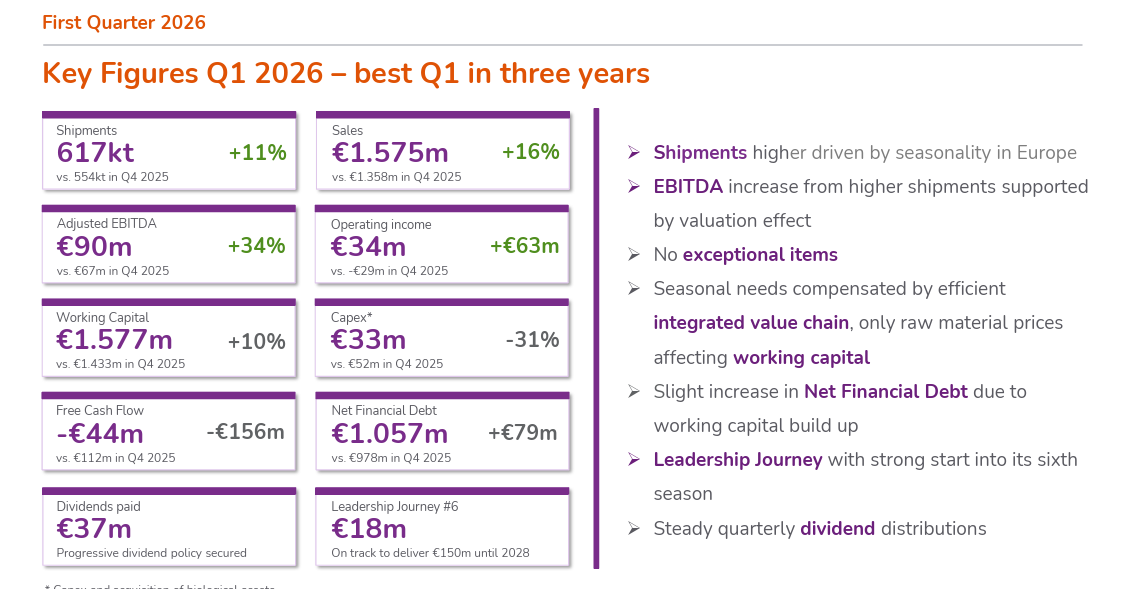

Outokumpu is getting a boost today (+5%) from Aperam’s results, in addition to which it seems a colleague from SEB has raised the target price and likely reiterated the previous buy recommendation.

Aperam reported its best Q1 in three years. The company has a somewhat different business structure than Outokumpu, but comments regarding the European market are, of course, always interesting. It is positive that according to Aperam, imports fell to 12% in Europe in Q1’26, i.e., to the level of import quotas. Although underlying demand has not picked up in Europe, the company benefits from the decrease in import supply and says: “In Europe, we are not just waiting for a market recovery - we are benefiting from a structural shift.” So, the Commission’s actions seem to be taking effect, and this also benefits Outokumpu.

The company is also guiding for a better result for Q2, driven by higher capacity utilization and rising prices. All in all, the market situation seems to be developing in a good direction for Outokumpu, but it would be important to get the European economy and, consequently, stainless steel demand growing. That is when prices would really start to rise, and through that, Outokumpu’s earnings.

Here are Petri’s pre-result comments as Outokumpu is set to release its Q1 results on Tuesday

We forecast that earnings have improved from the comparison period in both stainless steel business areas, but the absolute earnings level remains somewhat subdued, particularly due to low stainless steel deliveries. It is expected that in its short-term guidance, the company will guide for increasing stainless steel deliveries and growing EBITDA for Q2. We will review Outokumpu’s results on Tuesday morning in a live broadcast starting at 8:50 AM on inderesTV.

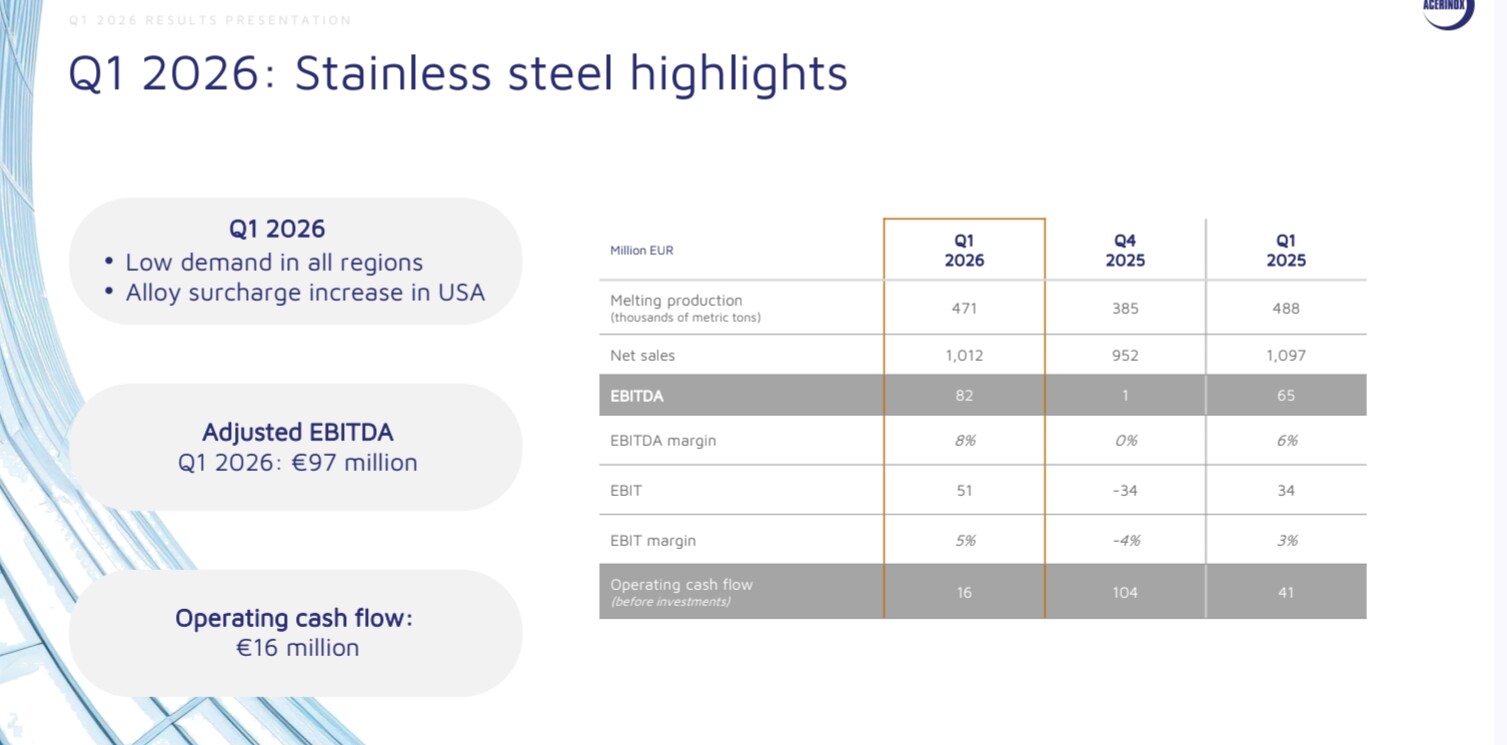

Briefly, the stainless steel division’s Ebitda rose from the zero level of 4Q25 → 82 million USD. Adjusted to 97 million USD.

Company-level guidance for 2Q26 ebitda is ‘Higher than’ 1Q26.

By division, the Stainless Steel division reported an EBITDA of 82 million euros (compared to 1 million in Q4 2025), driven by a gradual recovery of prices in key markets. Nevertheless, the rising cost of raw materials and energy has slowed the recovery of margins in Europe.

Outlook for Q2

Acerinox faces the rest of the year with caution due to geopolitical uncertainty. However, the company is optimistic thanks to its geographic diversification and the normalization of production in Europe.

“We expect Q2 EBITDA to be higher than in Q1. The improvement in order books in Europe and the United States, added to the decrease in imports, will allow us to improve sales volumes in the coming months”, the Group has stated.

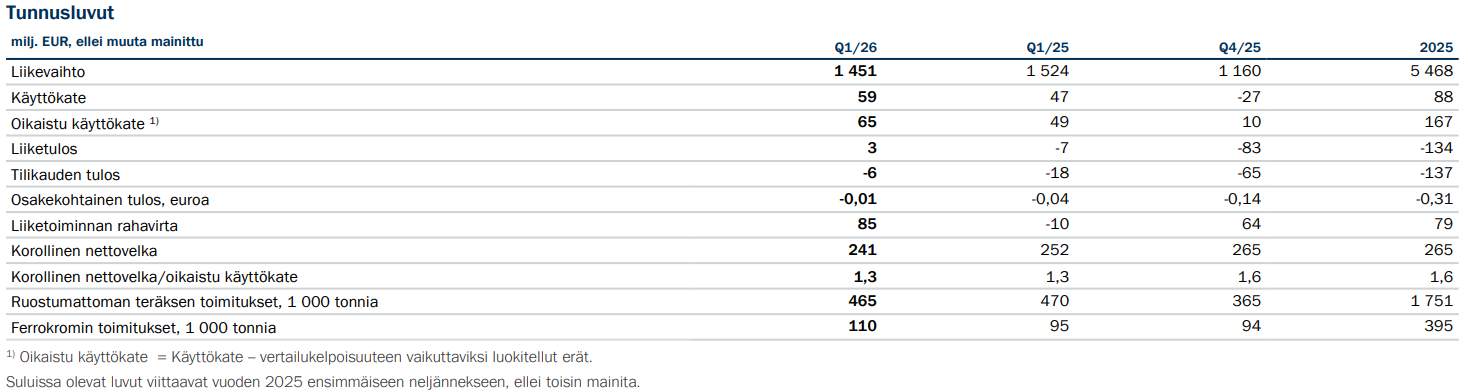

Adjusted EBITDA increased from the previous quarter to EUR 65 million. Growth was supported by improved profitability in the Europe business area, resulting from higher delivery volumes, and in the Americas business area, mainly due to a higher average selling price for stainless steel.

Stainless steel market activity improved due to seasonality and the Carbon Border Adjustment Mechanism (CBAM). Deliveries increased by 27% from the previous quarter to 465,000 tonnes.

The ferrochrome market remained balanced, supporting price increases and favoring Outokumpu’s low-emission European offering. Deliveries rose by 17% from the previous quarter to 110,000 tonnes.

Operating cash flow strengthened to EUR 85 million, mainly due to a stronger result, which was also supported by the release of working capital. Net debt decreased to EUR 241 million.

The restructuring program is progressing as planned, targeting annual cost savings of EUR 100 million by the end of 2027, with approximately half expected to be realized in 2026.

The EVOLVE growth strategy is progressing:

In the United States, construction of the pilot plant is moving forward. The facility will pilot the scaling of developed technology for the production of low-emission enriched ferrochrome and chrome metal. Production is scheduled to start in the first half of 2027.

Development of higher-margin specialty products in the ferrochrome business is progressing.

A large-scale circular economy ecosystem has been launched at the Kemi mine to utilize side streams.

The investment in the Tornio annealing and picking line is still under review.

The study regarding the investment in the Avesta melt shop continues, enabling the company to further expand into high-nickel alloys.

A bit muted due to Europe, otherwise strong momentum. Last year’s order backlog, or the large share of it, apparently eroded margins in Europe, and additionally, there have still been challenges with the ERP system. Hopefully, these are starting to be left behind; some clarification on this in the press conference would be welcome. Now is the time to get the engine running efficiently as the market and price levels improve in Europe as well.

First quarter of 2026 compared to the fourth quarter of 2025

Sales rose to EUR 955 million (Q4/2025: EUR 675 million) mainly due to

significantly increased stainless steel deliveries. Deliveries

grew by 46% primarily due to seasonality and the Carbon Border Adjustment Mechanism, and additionally,

the challenges in implementing the ERP system’s supply chain planning solution

were less significant than in the previous quarter.

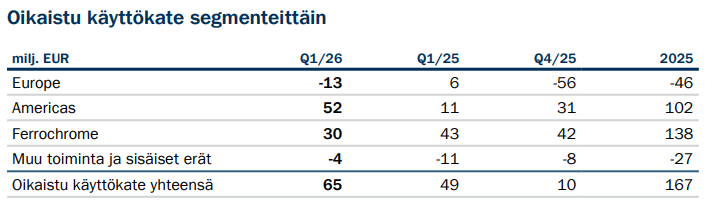

Adjusted EBITDA was EUR -13 million (Q4/2025: EUR -56 million) mainly due to

the growth in deliveries and the decrease in raw material costs secured in the previous quarter.

This positive development was partially offset by the high share of order backlogs

from the previous quarter, reflecting the temporary challenges in implementing

the ERP system’s supply chain planning solution. The margins on these deliveries

were lower than those for orders in the first quarter of 2026. The raw

material-related inventory and metal derivative gains/losses were EUR -11 million (Q4/2025: EUR 1 million).

@Petri_Gostowski the \n - ERP system\n - - supply chain planning solution\n - - - implementation\n - - - - challenges\ndeserve to be addressed properly in the interview!\n\nIn the 4Q2025 interim report, the matter was somewhat of a side note etc., but in 1Q2026 there was a clear change in the sense that deliveries rose significantly, and the poorer margins of old orders flowed through to the results, affecting the weakness at the entire group level.\n\nSo: \n -has Outsa’s management now gotten a handle on the situation?\n -are there still backlogged deliveries?\n -have many customers and deals been lost to others because of the inability to deliver?\n\nIn my opinion, Outsa’s management is leaving the matter unnecessarily open because they don’t clearly state that the situation is now OK. Is there an “excuse mode” on?\n\nWhen looking at delivery volumes in Europe, 4Q2025 is indeed in a huge pit, i.e., -60 ttons vs 3Q2025.\nAnd the massive increase in 1Q2026 vs 4Q2025 sort of offsets the pit left by 4Q2025\nBUT, even so, 1Q2026 is not any larger than 1Q2025\nSo it’s as if the pit has merely shifted\nUnless the “pit volume” has permanently disappeared into the hands of competitors…\n\nReview of delivery volumes in Europe:\n1Q2026: 324\n4Q2025: 223\n3Q2025: 284 \n2Q2025: 324\n1Q2025: 318\n4Q2024: 287\n3Q2024: 316\n2Q2024: 316\n\nFrom the 4Q2025 interim report:\n> Fourth quarter 2025 compared to the third quarter 2025\n> Adjusted EBITDA was EUR -56 million (Q3/2025: EUR -12 million).\n**> • Stainless steel deliveries decreased by 22% due to a weaker**\n**> market and temporary challenges in the implementation of the ERP system’s supply chain**\n**> planning solution.\n> • The decrease in average stainless steel selling prices was offset by an\n> improved product mix.\n> • Sales decreased to EUR 675 million (Q3/2025: EUR 859 million).\n> • Profitability was supported by a relatively smaller share of fixed costs, while\n> variable costs rose. Inventory and metal derivative gains related to raw materials\n> were EUR 1 million (Q3/2025: losses of EUR 4 million).\n> • Return on capital employed was -8.5% (Q3/2025: -7.1%), mainly due to weaker\n> profitability.\n\nFrom the 1Q2026 interim report:\nFirst quarter 2026 compared to the fourth quarter 2025\nSales rose to EUR 955 million (Q4/2025: EUR 675 million) mainly\ndue to significantly increased stainless steel deliveries. Deliveries\ngrew by 46% mainly due to seasonality and the Carbon Border Adjustment Mechanism (CBAM), and additionally\nchallenges in the implementation of the ERP system’s supply chain planning solution**\nwere lower than in the previous quarter.\nAdjusted EBITDA was EUR -13 million (Q4/2025: EUR -56 million) mainly due to the growth\nin deliveries and the decrease in raw material costs secured in the previous quarter.\nThis positive development was partially offset by a large share of order backlogs from the\nprevious quarter, reflecting temporary challenges in the implementation of the ERP\nsystem’s supply chain planning solution. The margins on these deliveries\nwere lower than for orders from the first quarter of 2026. Inventory and metal\nderivative results related to raw materials were EUR -11 million (Q4/2025: EUR 1\nmillion).