I must say that I like that more and more Finnish companies have started distributing dividends in multiple installments. It nicely smooths out cash flow during the year (both for myself and for the company).

Hopefully, share buybacks would also become more common as part of profit distribution.

Regarding the third phase of the strategy 2026>, we will hear more in connection with the Capital Markets Day in June 2025, according to Horst’s section in the financial statement release. Some time has already passed since the previous CMD, which was in June 2022.

Here is Outsa’s (Outokumpu’s) own press release and a couple of excerpts related to nuclear power.

“The results of the preliminary study are very positive and support the further development of the small modular reactor project. The completion of Outokumpu’s preliminary study demonstrates interest in utilizing the opportunities offered by developing nuclear power technology. Although we have now made a strategic decision not to expand our business into energy, we expect to be able to hand over the project for further development to a partner interested in continuing the project and investing in energy production,” says Stefan Erdmann, Chief Technology Officer at Outokumpu.

Energy accounts for approximately 10% of Outokumpu’s costs, and Outokumpu is Finland’s largest electricity buyer. Outokumpu is at the forefront of the steel industry in reducing carbon dioxide emissions.

I didn’t have time to properly listen to the Q&A, but what stuck in my mind was that the majority - almost all - of the cold-rolled material in Mexico stays in Mexico. It remained unclear what portion returns to the US locally with the manufacturing of parts and products.

More on the US investment at the 6/2025 CMD, something is in mind but the CEO didn’t reveal what.

Last time, products that were “melted & poured in USA”, i.e., from foundries like Calvert, remained outside the tariffs.

This is not within their sphere of influence, so it would be rather pointless speculation at this point.

However, Kati seemed to state well that those economies are so closely intertwined, including the automotive industry. So that is a fairly direct reference indicating that they don’t really see this as a high probability at this point. Of course, there have been temporary disruptions, but no significant impact in the long run.

There was also a point where I noticed a smile-like comment, whether it was related to volume or prices, as they don’t comment in principle. I guess that could somehow be taken as a positive sign that things are moving in a better direction. I need to re-examine that part and think about what can actually be read from it.

I largely agree with your view, Grape. Outokumpu is now “in good hands” and in good shape for an upward cycle that will surely begin at some point. Ter Horst indeed seems like a firm CEO and stated directly that no “unreasonable” investments will be made, if one can express it that way.

The dividend is quite high at €0.26, and I think that’s a very good thing. The company has the ability to pay it, and it keeps investors engaged with the stock. Special congratulations to the short-sellers, above all, for the hefty dividend

I noticed the same thing. It seemed to be about an analyst’s insistence on improving price levels. So, if I remember correctly, the analyst was looking for the guided 10-20% growth in deliveries to be a greater improvement than usual seasonal variation, and that it would be unlikely without prices rising. CEO ter Horst tried several times to avoid commenting on future price levels, as is customary, but indeed, a visible and twitching smile at the corners of his mouth, along with comments at the same time that you can draw your own conclusions based on the fact that order books have clearly strengthened. In another context, the CFO stated that delivery growth is similar in both Europe and the Americas.

I need to watch the press conference again and/or read the transcript when it becomes available. The overall impression from the press conference and also the Inderes interview was very positive. The market situation has improved and restocking has begun; they didn’t dare to say yet whether there has been a permanent turn for the better in end-demand. ter Horst also strongly emphasized the message regarding keeping the dividend unchanged, stating that the company is confident and positive about the future – this, in my opinion, is an important indicator in the dividend proposal.

This potential investment in increasing capacity for something other than cold rolling in the USA remained behind a veil of fog, but I understood from ter Horst’s comments that we will hear more about it on June 11th at the CMD – if it were about some acquisition intention or something similar, then one could perhaps imagine that it would happen around the CMD or slightly before it, because one wouldn’t “speculate” in advance about intentions to acquire some operation.

Inderes raises the target price after yesterday’s earnings day:

3.5 eur (Add) → 3.8 eur & Add

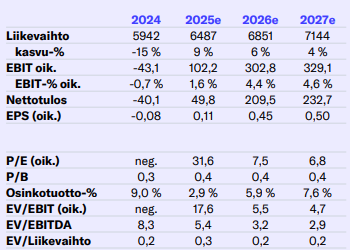

Valuation is low relative to through-cycle earnings

With this year’s weak earnings, the stock’s valuation multiples are high (P/E ratio 32x and EV/EBIT 18x), but relative to through-cycle earnings, we believe the stock is moderately priced (P/E ratio ~ 8x and EV/EBIT ~ 6x). The same valuation picture is also drawn by the valuation relative to the long-term historical average free cash flow (P/FCF just under 10x). Thus, reflecting the moderate valuation and the financial position that carries beyond the current subdued cycle, we consider the stock’s return/risk ratio attractive, even though the start of the next upturn is still pending. At the same time, we remind that the aforementioned valuation methods do not work for timing purchases, which supports temporal diversification of additional purchases.

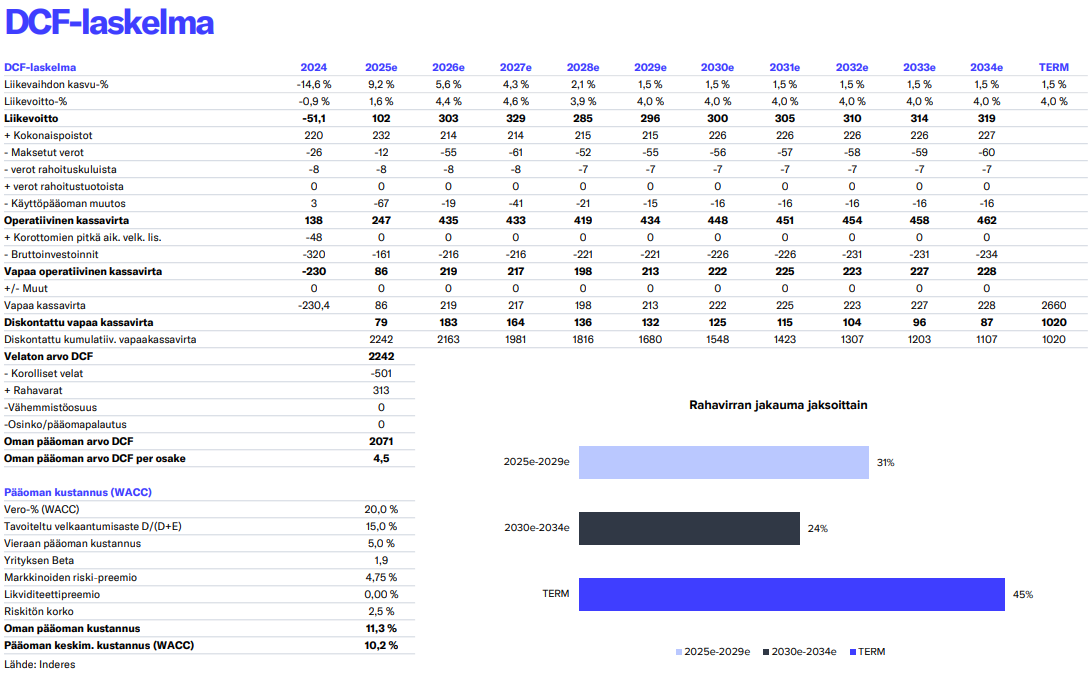

According to the latest analysis, the DCF calculation would give a fair value, or at least the present value of discounted cash flows, of 4.5 EUR, taking into account interest-bearing debts and assets.

One can always speculate how easy it is to predict even the next quarter, but this is how it looks when an EBITDA level of approximately 500-550 MEUR (i.e., operating profit + depreciation) has been used in the DCF calculation from 2026 onwards.

This level is therefore a level pegged by Outokumpu itself, despite all cost savings and other excellences.

At that EBITDA level, an EPS of 50 c/share seems achievable, and at the current share price, a P/E ratio in the range of 7-8.

And if 4.5 EUR were the level justified by cash flows, i.e., an above-cycle average, and if the observed approx. 3 EUR is the bottom, then correspondingly 6 EUR/share would be the ceiling for the share price.

Here’s a challenge for the new CEO: how to achieve something more than just deliveries above the aforementioned cycle level, so that the earnings level would genuinely rise from the current one.

Of course, Outokumpu’s descent into cyclical troughs and subsequent rise offers great opportunities for emotional experiences, perhaps better than Elisa, but the numbness would be reduced if the wave curve progressed not only along the x-axis but also, on average, along the y-axis (i.e., on the positive scale).

Outokumpu’s Q4 results did not offer any major surprises following the profit warning issued in December. The highlights of the report were – considering the weak market – surprisingly good volume guidance for Q1 and the dividend remaining stable compared to the previous period. Risk factors still include political strikes in Finland, global trade policy, and uncertainty related to the timing of the industrial cycle’s recovery. Analyst Joona Harjama elaborates on the company’s Q4 and outlook in the video.*

The impact of potential steel tariffs is mitigated by the fact that Outokumpu is already partly locally present in the US market. One could imagine this.

“In the Americas business area, customers are served by the Calvert melt shop and cold rolling mill in Alabama, United States, and the San Luis Potosí cold rolling mill in Mexico. Our market share in the USMCA region is approximately 23% and in the United States approximately 21%. The San Luis Potosí cold rolling mill is Mexico’s only stainless steel production facility, and we are the market leader in Mexico. Americas’ share of Outokumpu’s revenue was 27% last year.”

“The Americas business area is well-positioned to meet the growing needs of the American markets. As part of the preparations for the third phase of the strategy, we announced in August and November our desire to strengthen our position as the market’s second-largest producer.”

At the same time, competition in Europe intensifies if other European manufacturers’ exports to the United States decrease. Tornio will have to show its mettle there.

Edit: I should have written “exports of other European and Asian manufacturers” because, of course, if exports to the United States decrease, the pressure to dump Asian overcapacity into Europe will only increase.

Yes, this time, however, both the EU and Outokumpu have experiential readiness for what’s to come…

To refresh your memory, the mere title should tell you all that’s essential, so the paywall won’t be much of a hindrance:

==>

This time, due to the global cycle, the situation is still very much “up in the air,” or rather premonitory…

(=it could truly, for once, be quite opportune for Outokumpu, in the end)

Around the time of the financial crisis (before the financial crisis) in 2008, Outokumpu’s share cost over €70 per share. Can someone explain what accounts for Outokumpu’s peak share price at that time and why the share price has not recovered anywhere near that peak figure but has remained “stagnant”?

P.S. I am not familiar with the history of Outokumpu company and its shares that far back. This might even be a “silly question”, but I’m asking now because it’s really bothering me.

The peak price is explained by the much smaller number of shares at the time. At that time, the number of shares was 181,345,338, from which it swelled more than 50-fold after several massive issues when the Inoxum deals had to be settled. From your chart, you can see how the owners’ value has been diluted in the issues. Below is a link where you can see the change in the number of shares in more detail