Inderes raises the target price after yesterday’s earnings day:

3.5 eur (Add) → 3.8 eur & Add

Valuation is low relative to through-cycle earnings

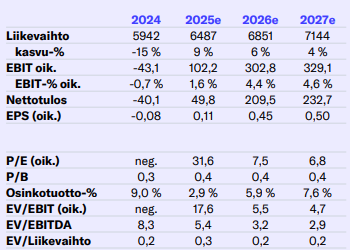

With this year’s weak earnings, the stock’s valuation multiples are high (P/E ratio 32x and EV/EBIT 18x), but relative to through-cycle earnings, we believe the stock is moderately priced (P/E ratio ~ 8x and EV/EBIT ~ 6x). The same valuation picture is also drawn by the valuation relative to the long-term historical average free cash flow (P/FCF just under 10x). Thus, reflecting the moderate valuation and the financial position that carries beyond the current subdued cycle, we consider the stock’s return/risk ratio attractive, even though the start of the next upturn is still pending. At the same time, we remind that the aforementioned valuation methods do not work for timing purchases, which supports temporal diversification of additional purchases.

https://www.inderes.fi/research/outokumpu-q424-matala-arvostus-houkuttaa-roikkumaan-kyydissa