We probably don’t have a buying pants thread for this year’s recession yet, so here’s one. Of course, the recession hasn’t been officially declared yet, I guess, but some people are already putting on their buying pants, and the negative signs in both the market and portfolios are such that we can soon start talking about bargain hunting. In addition to the valuation multiples recovering.

So the question for everyone: What stock are you buying, for a short-term or long-term portfolio, and why? Bonus points if you can specify the level (or event) at which you plan to buy.

Three clearest examples from my list:

HIMS

Trust in the company’s growth despite all the chaos. Health is something for which people will continue to try to find more cost-effective solutions than what American healthcare offers.

Additionally, it’s on a long-term trend line, for a short-term portfolio.

Alphabet

Along with Microsoft, the safest-feeling MAG7 options to date. Core business on the most stable footing and relatively fewer dependencies on Chinese supply chains. Would be nice to buy for a long-term portfolio, but only if there’s a margin of safety.

Fortum

The evergreen favorite of the dividend party (and long-term dividend portfolio) is starting to interest again as multiples improve and the dividend yield climbs. Not as risky as banks, but with a dividend yield like a bank’s.

Practically, the buying criterion for all of them is this current chaos calming down, or an announcement of some “deal” that triggers a relief rally and a trend reversal.

The S&P opened already at the time of writing with a 2% drop… 2% → 3% → 1% rise (!), so there’s a risk that buying pants will have to be dug out and put on soon.

Nurminen Logistics addition under consideration. Reason: Logistics is needed as long as only rats are left.

WithSecure also an addition to the list. They seem to be slowly getting the machine humming.

Bioretec has been beaten down. When it rises, I bet it will take off strongly. The steps are in hand.

Disclaimer: I’m trying to keep my portfolios to a reasonable number of holdings, and now is not the time to switch (nothing tax-deductible is even properly at a loss yet) – so I’m mainly looking at what I want to add based on existing holdings.

I myself have been considering adding more Nordea (already overweight) simply because I don’t believe in any doomsday scenario in the financial markets, even if the sky is a bit dark. Fortum also tempts me if it gets even a little cheaper because it’s a boring basic business (already own some). I’ll put more money into one of these again soon.

From the US, I’m mainly looking at GOOG (stable business, mostly non-physical so tariffs don’t affect it much, in my opinion a good AI story bonus).

I myself have thought about adding more Vaisala to my portfolio (which is a very “long-term” portfolio). This will probably happen quite soon. Vaisala is a quality company, always a bit too expensive but now relatively cheaper than some time ago. The company is “boring” in many ways, which is a good thing.

Then I’ve thought about waiting for Berkshire’s annual meeting and listening carefully to Buffett’s answers to current questions (this year there will certainly be plenty to ask). After that, I’ll go shopping, targeting some quality companies, but I need to think more carefully about potential companies while waiting.

Now I just have to be patient and wait almost a month; I’m really eager to go shopping already.

Personally, despite everything, I currently see the greatest potential in the US. Shopping list:

US defense industry companies have declined due to defense budget savings plans and now even more. However, they are among the best companies in their field, and replacement sales will likely come from the EU and elsewhere.

US residential REITs have now fallen to an attractive level. Tariffs do not affect rents, and new construction is becoming more expensive. Tax cuts sufficiently support Main Street’s purchasing power, so rent-paying ability is maintained. Falling interest rates support stock prices.

The trade in used goods increases as prices for Chinese goods rise. For example, eBay benefits from this and grows, even if the economy generally weakens.

Healthcare diagnostics and research sector stocks, e.g., Thermo Fisher, have fallen a lot. Perhaps the Trump administration influenced this, but I don’t believe the situation is permanent, and megatrends will support the industry.

Additionally, I am following:

Industrial automation companies: e.g., Rockwell, Emerson, etc.

Semiconductor manufacturing side. These have also fallen a lot, and megatrends continue to support them.

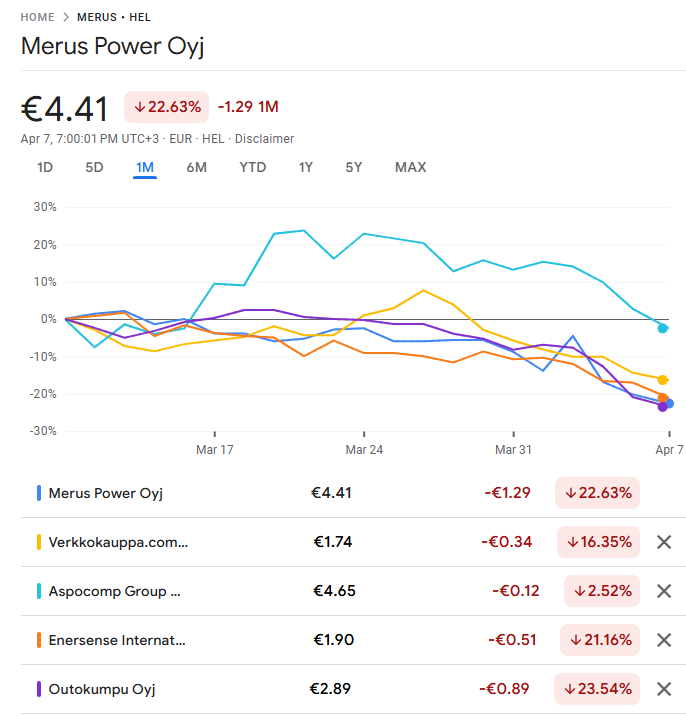

You can find them on the domestic stock exchange too. In Finland, small companies (excluding the slightly larger Outokumpu from the list) are also quickly forgotten, so for example, these are just for monitoring:

Of course, Canatu or Finnair, which crashed, could also be added to the list.

Surprisingly, Tulikivi has held its share price quite well, so I left it off the list, but it’s an interesting one to follow.

And Intrum is certainly in a promising position; debt restructuring is largely a sure thing, but it’s not yet reflected in the share price.

On my potential shopping list are (quality) stocks whose businesses I don’t foresee long-term impacts on, but whose prices are falling along with the rest of the market; here are a few examples:

Visa - Tariffs should not affect Visa’s business, though if the US falls into recession and consumption stalls → payment transactions will decrease, which will be reflected in Visa’s business.

S&P Global - Credit ratings and indices. Tariffs should not affect the business. Of course, a stock market decline and recession are not good for either business, but if interest rates fall in the US, this should be a positive driver for both.

Hims & Hers - I don’t see tariffs affecting the business. A potential recession could, of course, be detrimental to the business in the short term.

A couple of examples from Finland whose businesses tariffs should have no impact on, but are falling along with the rest of the market:

Puuilo

Lapwall

Then, some thoughts. I believe that the ECB will start cutting interest rates at an increasingly accelerated pace, especially if the Eurozone heads towards a recession. I don’t see inflation being a problem in Europe. I therefore believe that we will return close to zero interest rates during this year, which should be reflected positively in the business of Finnish asset managers. I am following the following with particular interest:

eQ - In my opinion, a safer choice among Finnish asset managers.

I already bought. Today, at least, it seems it was worth it, as green is flashing again for a change.

Yes, I mainly bought cyclical Helsinki stocks. I added, among others, Outokumpu (at a price of €2.86), Wärtsilä (€14.30), Neste (€7.50, I wonder if it’s going bankrupt soon?), Taaleri (€6.32), and Metso (€7.98). It’s possible that they will still go down a lot, but I’ll buy more!

From the US, I’m currently most interested in GOOGL, MSFT, and PFE.

Not the sexiest business, but if one is considering a global, defensive, and local business, then Huhtamäki seems quite interesting. Around 30 euros or below, it’s probably not the worst miss if you don’t crave drama from portfolio companies.

Black diamond group - Primarily rents modular buildings in Canada. Good business, and the market can still be consolidated.

Dentalcorp - Dental clinic roll-up. The business is defensive, has pricing power, and best of all, has so much debt that if a proper recession hits and interest rates potentially fall, net income will grow as interest expenses decrease.

Lensar - Manufactures cataract treatment devices. A month ago, it was announced that the company would be bought out from the stock exchange for $15. Now the stock is at $13, which suggests that the market does not believe the deal will go through due to the current environment. I’m still waiting for better prices, but it’s an okay deal even now, even if the transaction doesn’t go through.

Blackline Safety Manufactures meters for gas leaks, etc., and adds SaaS services on top. A proper Rule of 40 company. It was just about to turn cash flow positive, but there’s so much cash on the balance sheet that it’s perfectly fine if there’s a lean year.

Currently, orders are also open for German basket stocks Nfon and Q.Beyond.

ASML Holding: I took the first 3% on the dip. Still planning to add a couple of tranches to reach about a 10% level, quickly or slowly. Reasons simply: Strong moats and no viable competitors. Even the Americans have to buy from ASML if they want to get chips, or if they can still get them from Taiwan currently, or if China escalates.

Huhtamäki: Added to position. Progressed according to strategy. Local production in different market areas, and even if demand suffers due to the erosion of purchasing power, margins can be moderately defended through pricing.

As before, we will try to hunt for quality companies from the domestic stock exchange that would pay (rising) dividends long into the future. Now we just wait patiently, if/when the price drops low enough. At least on the watchlist:

Huhtamäki

Wärtsilä

Sampo

Olvi

Harvia

Revenio Group

Väisälä

Marimekko

If the valuation completely crashes through the floor, we might consider:

For the long-term portfolio, I intend to add Seligson Top 25 Brands and Top 25 Pharma. I already buy these monthly, but now I could increase the buying volume - you get so many top businesses with the same effort (and since there’s no subscription fee, it’s easy to diversify, e.g., monthly purchases to a weekly level if the dips are concerning).

Domestic stocks under observation:

Sampo (not currently in the portfolio, but I’d gladly take it back)

Viafin Service (a bit of a wildcard, but boring is good if the price is right :D)

Nordea (already have some, but if it drops low enough, I’ll add more generously

International additions to existing portfolio holdings:

Storytel

Investor AB

Berkshire Hathaway

Other potential candidates:

Meta: I’ve been out of this for several years (maybe shouldn’t have been, but the AR strategy/tragedy didn’t convince me )

Nasdaq 100 ETF: this will surely take more hits, but in the long run, it’s hard to see that there wouldn’t be big winning companies in this group in the future as well.

PYN Elite: If I manage to gather enough for a 10k entry, this could be good at some point, as things are quite volatile in Vietnam right now.

Dick’s Sporting Goods: strong performance, but the valuation was quite high. Perhaps good opportunities will open up in the future.

Shopify: great product, but the valuation has been at its peak. Perhaps buying opportunities will open up now.

Shopify’s and Apple’s stock prices seem absurd; they should be at rock bottom with these tariffs, shouldn’t they? Dropshipping is completely dead if every piece of Chinese junk gets a 150% tariff, but Shopify’s stock price is still at November’s levels.