I don’t dare to present myself as a Nordnet expert, but I hold the stock with a small ~4% weighting in my portfolio. I can tell you what I personally paid attention to.

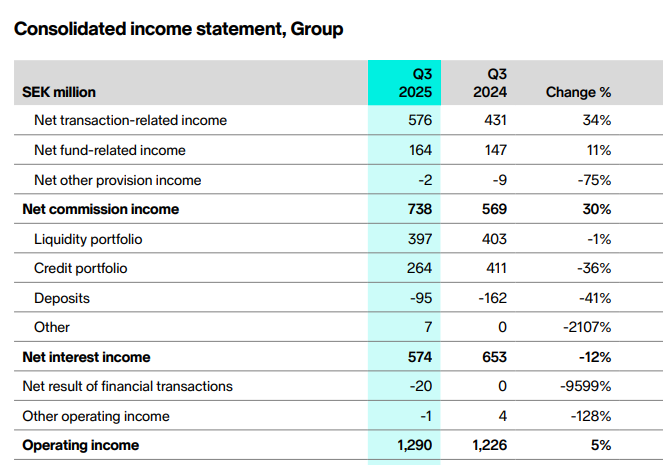

The company’s profit has grown “modestly” in recent quarters relative to the growth in users and AUM. In my understanding, this is due to the Nordic preference for variable-rate loans, which, with falling interest rates, have affected the company’s net interest income. The best image to illustrate this is a broader income statement:

As can be seen, “brokerage income” (net commission) and “banking income” (net interest) are roughly equal but moving in different directions. In my opinion, it is essential to understand that banking income is expected to stabilize as interest rates stabilize. Thus, in the future, the growth of the brokerage side (a massive +30% atm) will determine the group’s growth, as the net interest income will no longer hinder growth.

I thought the result was good because the company’s gross margins remained high despite expansions into new exchanges (Portugal/etc.) and investments in Germany. There are no signs of the brokerage side’s growth stopping. Ask yourselves: If your acquaintance wanted to start investing and asked you to suggest a broker for this purpose, why would you recommend anything other than Nordnet? IMO, the company has found a winning concept, at least in the Nordics.

The biggest question in the coming years will, of course, be Germany and the company’s ROI as it expands there.