2023Q2 hit guidance, and forward guidance remained slightly soft, projecting roughly the same as previous quarters. The market seemed to take it fairly neutrally.

NS went and acquired a small ML team from San Diego. The purchase price is likely not significant, but the potential technical competence and strategy get you thinking. Based on my understanding, it’s some sort of PoC shop focused on Edge AI/Low-Power AI ML. When considering the synergies with NS’s other new technology initiatives, there’s a pretty clear link to the RISC-V focus that started a while ago (which was also reinforced recently when they were one of about ten semi (PJ) firms that formed a RISC-V alliance). One of the great features of RISC-V is how easy it is, both technologically and licensing-wise, to create accelerators and other similar auxiliary blocks for the processor. For example, learning, energy-efficient image or audio processing where the power budget doesn’t break NS’s core ultra-low power concept. I could well see NS products being released in a couple of years that have truly significant accelerator cores integrated into the same package with NS’s core technology.

On LinkedIn at least, there’s been a massive amount of new product releases during and after the summer. Some have been more marginal products, but I’ve personally noticed that these new public references are significantly more mature “proper” products compared to before, where the majority felt like “yet another BTLE beacon.”

Across the wider semiconductor (PJ) industry, it’s estimated that demand will turn upward in early 2024 instead of the previously expected 2023H2. That is, half a year later than the consensus was, for example, at the start of the year. Of course, there are exceptions. Most notably Nvidia, which is driven by AI chips and their demand. AI chips need (high-speed quality) memories. Demand for these is expected to grow significantly already during the remainder of this year. NS has nothing to do with companies like Nvidia. Six months ago, NS’s valuation still fluctuated heavily with the semi index, but now my gut feeling says that’s not so much the case anymore. Nvidia’s share price no longer reflects as strongly on NS’s share price.

The company sees Q3 sales at $135-140m (prev. $145-165m) and gross margin at 50-51% (prev. over 52%).

Demand is soft across all markets, and there have been no signs of improvement. Visibility for the remainder of the year remains limited, and the company is not providing guidance for the fourth quarter.

This is what we’ve been waiting for, the spiritual successor to the highest-volume product in the NS catalog, the nRF52.

The specs and marketing talk look quite good. This isn’t some world-shattering, fancy new chip, but rather a better iteration of its predecessor. The biggest individual takeaways from the marketing materials are the internal RTC and the TSMC 22nm ULL node. The internal RTC removes the need for an external crystal, making the processor’s footprint considerably smaller. In addition to the crystal, this also removes (depending on the crystal) two capacitors. The internal RTC is also said to be more power-efficient. The 22nm technology should significantly improve power consumption. Even the clock frequency is quite moderate. Based on these factors, the low-power characteristics should be really good. The old nRF52 was also low-power, with peak consumption of a few tens of mA with the radio on and <1uA while sleeping. The radio’s peak power will likely remain roughly the same, but there should be a significant difference in the processor’s active and sleep modes.

Nordic Semiconductor’s Q3 interim report is on Tuesday, 17 October 2023. A good summary of Nordic Semiconductor’s previous figures can be found on Euronext. Links below.

It’s going to be a rough ride today with these numbers

Q3 Highlights:

■ Revenue of USD 135.0 million (-33%)

■ Gross margin of 50.5%

■ EBITDA of USD 13 million (-79%)

■ Acquired US based cutting-edge AI/ML technology

and team

■ New nRF54H Series - offering world-leading

processing performance and processing efficienc

The guidance was quite a cold shower. Naturally, one wouldn’t have hoped for this after the profit warning. The report and webcast clearly state that the results are supported by Tier 1 customers and, to a lesser extent, a surprisingly large legacy business (proprietary segment, mainly consisting of PC peripherals).

NS itself would have the capacity to deliver both new and old nodes, but the market is very grim. They are not providing guidance for 2024 at all. In the general industry thread, ASML, for example, sees that we are currently in the deepest trough. That remains to be seen.

NS also mentioned cost-cutting of $5M per quarter and resource allocation that prioritizes projects generating revenue in the near-to-mid term at the expense of long-term projects.

I guess there’s nothing else to do but wait for the upswing and potentially buy quality for cheap. P/E is around 30 atm.

Svenn-Tore Larsen, who has successfully led the company for over two decades, is stepping down. He started as CEO in 2002. During Larsen’s tenure as CEO, the company grew from a small consulting firm into a global semiconductor company. Revenue grew from less than 10 million dollars to 777 million dollars (2022). A brilliant performance and a great career!

Highlights Q4

■ Revenue of USD 108.2 million (-43%)

■ Gross margin of 52.0%

■ EBITDA loss of USD 6.9 million, including

restructuring charges of USD 4.9 million

■ Successful bond issue of USD 93 million

■ Implemented cost cuts that will take full effect

from 2024

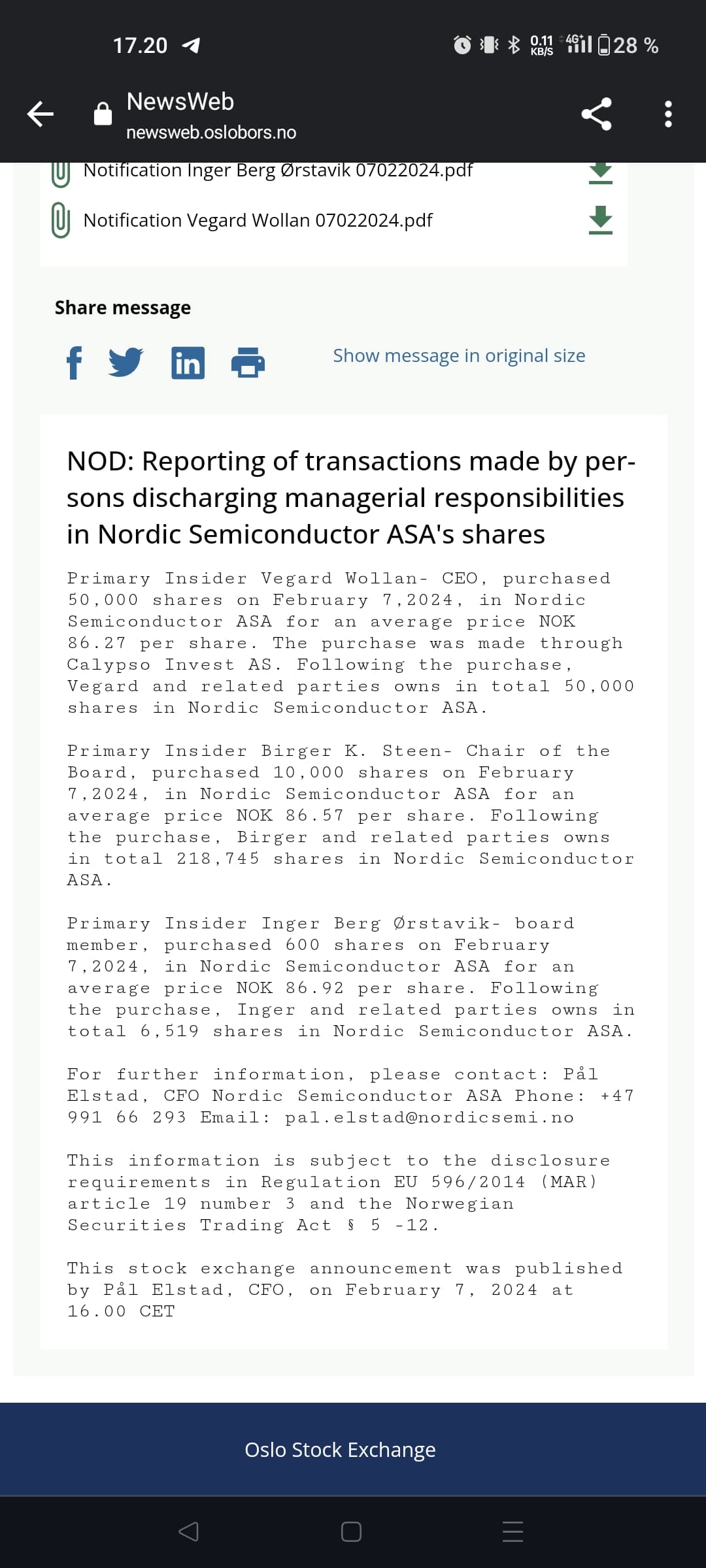

■ Vegard Wollan appointed new CEO from

January 1, 2024, succeeding Svenn-Tore Larsen

Revenue was USD 108.2 million in the fourth quarter 2023 and USD 542.9

million for the full year 2023. This corresponds to year-on-year declines of

43% and 30%, respectively, reflecting a cyclical downturn in the electronics

industry among both consumer and industrial customers. Bluetooth revenue

declined by 48% year-on-year in the fourth quarter and by 28% for the

full year. Nordic maintained a high and stable design win market share

throughout the year.

Kylmä oli Q4 kuten odotettiinkin ja pöytä on putsattu uudelle CEO:lle

It was even colder than expected. Revenue was 12% below consensus, and the EBIT expectation of -6.5 was optimistic compared to the actual result of -18 million.

And the guidance is very bleak:

‘‘Although Nordic remains confident in the long-term

market potential for its products and technologies, the

market is in a cyclical downturn with macro headwinds.

Nordic hence sees low revenue in the first quarter of

2024 due to continued inventory adjustments as well

as more normal seasonality. Total revenue is expected

to fall within the range of USD 70-80 million in the

first quarter.’’

‘‘Gross margin came in at 52% for the fourth quarter,

and is expected at around 50% for the first quarter

2024’’

No longer-term guidance was even provided. Unfortunately, the share price reaction seems quite deserved.

Interesting new products were indeed listed in the report, but apparently the consumer side is now completely frozen and there is still unsold stock in the warehouses. What would turn this around, and when? I have no idea myself, but could there be something coming in the VR headset segment, if/when a breakthrough occurs there.

This European interest rate shadowing doesn’t help a continent in recession and its consumers one bit…

That was a rough ride. I watched the conference call this morning. It added some context to the report. Key takeaways:

The cooling of the global economic winds is visible and will continue to be for at least the next quarter.

In the future, guidance will only be provided for the next quarter. Longer-term guidance is too uncertain. Also, some data points will be censored going forward to protect customer profiles. Apparently, it has been possible to read between the lines and see what major customers have ordered, etc.

Tier-1 customers are attractive in their volumes. Demand has slumped significantly in the “others” sector.

There were a lot of costs during Q4. Some Q3 expenses shifted to Q4. Also, two tape-out processes were carried out during Q4. These typically cost at least tens of millions or around a hundred. The nRF54 tape-out was exactly 100m in the middle of last year, if I remember correctly.

Out of about 1500 employees, around 100 are being/have been laid off. The impact will start during Q1.

On a positive note, the company released a couple of new products at the end of the year.

On a positive note, the portfolio seems to be very well positioned for when the economy starts to pick up again.

There was good organic growth in the cellular segment.

Market share in new designs was slightly up, with a share of over 40% of the total market.

I’ve been keeping a close eye on China, which has been a major market for NS’s legacy products. The macro winds there are still very cold. China’s recovery to normal should be clearly reflected in NS. Another thing I would also keep in mind is BTLE Audio products, including the nRF54. If these start selling well, there could be a lot of potential on the bottom line.

Lots of talk about other MCU manufacturers and their ecosystems, but also opinions on NS. In the OP’s post, NS is at the second-best level, and many comments recommend raising NS to the top category. This is the reason why I originally created this whole thread on this forum; a great developer experience. Developer friendliness, based on my gut feeling, ranks as the third most important factor in any project after technical and financial aspects. A 40+% design win ratio supports this well.

Several analysts have raised their TPs. This is the first time during the downtrend that new TPs show upside potential. Analysts’ TP bottom has been reached.

A few product launches. Iterative product family additions to existing lines.

Somewhat soft Q1/24 figures, but the outlook for the rest of the year is positive and the upcoming share price bounce is already pricing this in. The auction seems to be lasting quite a long time.

Q1 was pretty much right in the middle of guidance. The bottom line was slightly better, while revenue, on the other hand, was a bit weaker. However, the guidance was very welcome news, and a +30% jump compared to yesterday’s close seems well-deserved. In other key metrics, the same old story continues: design wins with the same dominant grip, with the majority of the result coming from BT chips. Cellular was once again a real wild card, this time falling slightly short of at least my expectations. However, the new CEO mentioned in the conference call that customers have many projects in the pipeline that are not yet on the market. There were also a few percent from PMIC chips marked on their own line. There is also potential to gain new market share there. A quick Google search shows the PMIC market as a whole is 35 billion and is expected to grow to 65 billion by 2030, according to analysts. I couldn’t find similar figures for low power.

NS’s valuation has seen a good tailwind in the aftermath of the previous earnings report. The share price has nearly doubled from the lows in the 80s. If the forward-looking guidance for the next quarter is strong, I believe in very strong valuation growth for the rest of the year as well.