Nordic’s CMD arrived, and at the same time, the share price made a significant correction of about 20% towards the southeast (heading down). I was wondering about it myself at first. Let’s break it down:

-

New strategy under the new CEO. The CEO changed at the beginning of the year when the long-time predecessor retired. The new CEO was an engineer at NS 20 years ago. Since then, he has gained experience elsewhere in the MCU industry and has now returned to NS.

-

NS is targeting a 25% EBITA margin by 2028. Similarly, 20+% growth.

-

4 business areas, each with targets and responsibility for their performance: BT, Cellular, BT, and others (PMIC). If results aren’t achieved and targets aren’t met, heads will start to roll. This wasn’t said directly but was implied. Especially the WLAN and PMIC sides are under the magnifying glass.

-

The market is soft. Especially in Europe. Elsewhere, the market is performing well. Europe’s softness is particularly evident in the industrial segment.

-

NS’s core problem with current profitability is that they are unable to scale their costs as the market and volumes decrease. Work has been done to solve this. If volumes were higher, profitability would be too. Overhead is too much. However, when the market recovers, this provides a good ability to meet demand without additional costs.

-

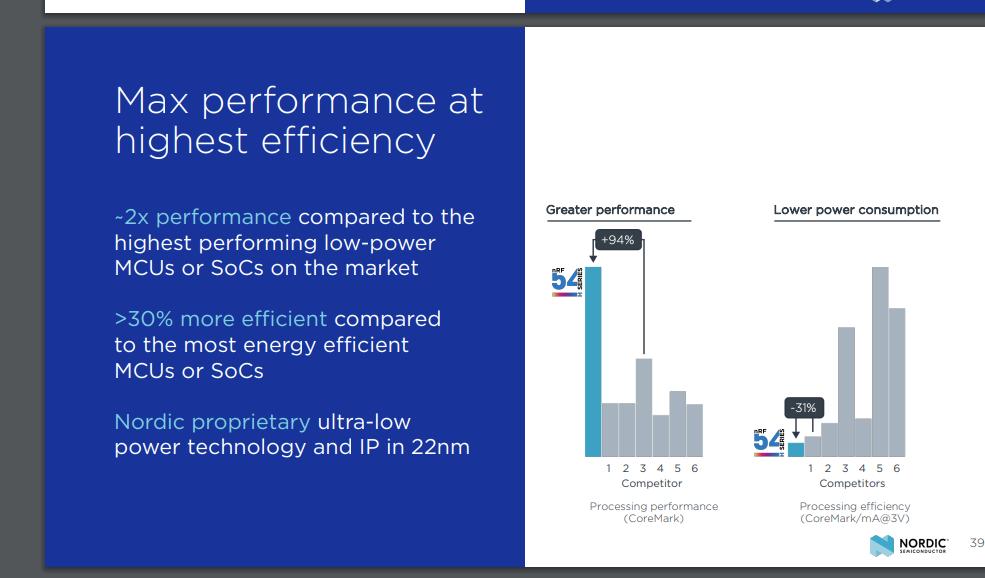

The transition to 22nm is a big deal. Both the upcoming 54 series and the new 91 series are technologically a decade ahead of their competitors in power, power consumption, and RF performance.

-

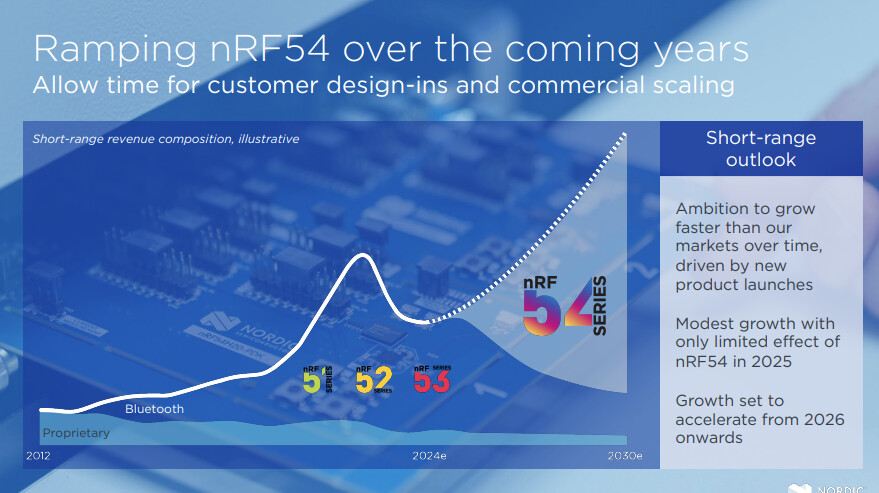

nRF54 market plan

Both the H and L series have been sampled with 200 customers. Feedback is reportedly very, very good. Customers are interested in both horizontal and vertical transitions (52 → 54L and 52 → 54H). -

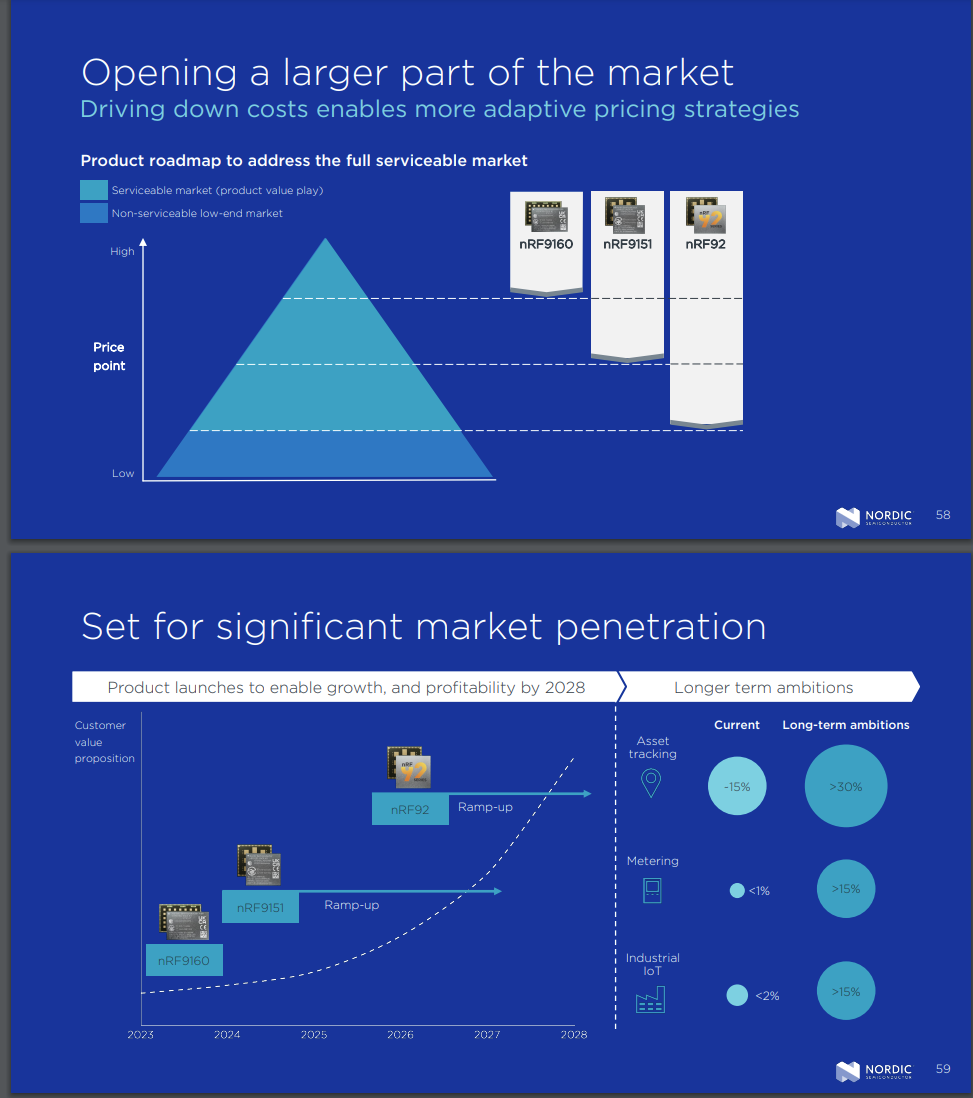

A bit of slow scaling on the cellular side. The new smaller and better price-point 91 series is reportedly very well-liked.

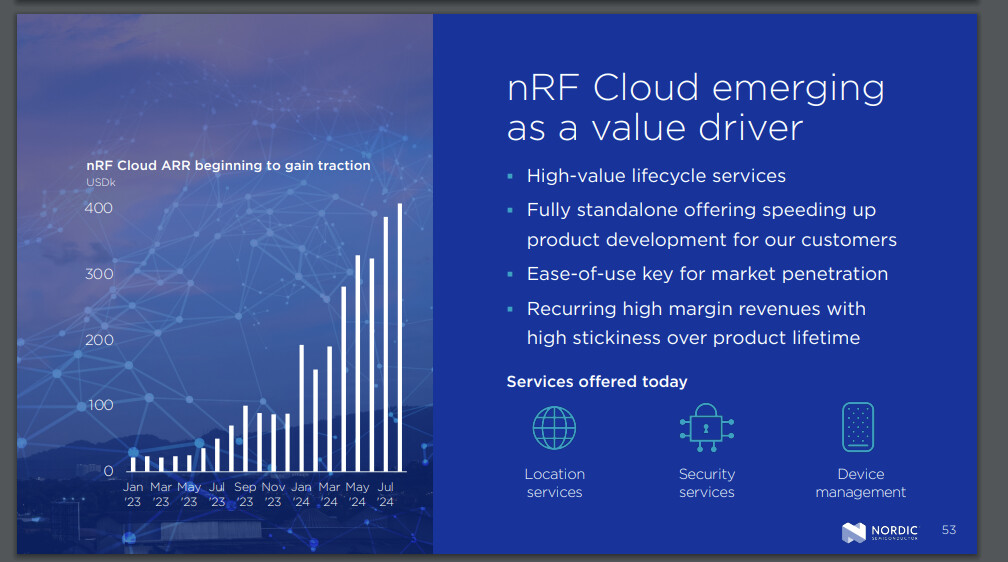

Best in class. On the cellular side, the cloud service business has reportedly gained good momentum. Still small, but the potential is huge.

-

71 series WLAN chip coming. Includes something 54-like from the MCU side and a Wi-Fi 6 (WLAN6) capable radio.

-

A big surprise whose impact I don’t think should be underestimated: the 53 series has found its way into the Samsung Ring, or more familiarly, Oura’s toughest competitor.

-

Market analyses of all customer vectors were credible and looked healthy

-

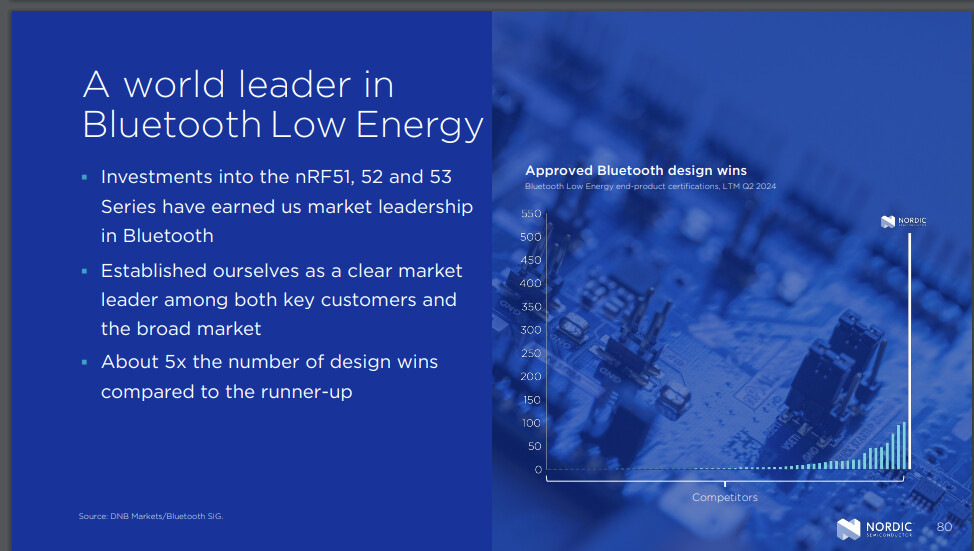

Clear number one in design wins

Technologically, this CMD was quite positive. Why, then, did we go down 20% during the day? At the end of the CMD, there was a Q&A moderated by two analyst representatives. 50+% of all analyst questions were about the 2025 guidance and the fear that one significant healthcare customer might have switched technology. This was asked many times in many different ways. The CEO and CFO denied everything they could and also appealed to the fact that they only provide guidance one quarter ahead. It felt like this was the biggest negative factor. I personally can’t take a stand on this kind of speculation—whether it’s true or not and what the impact is.