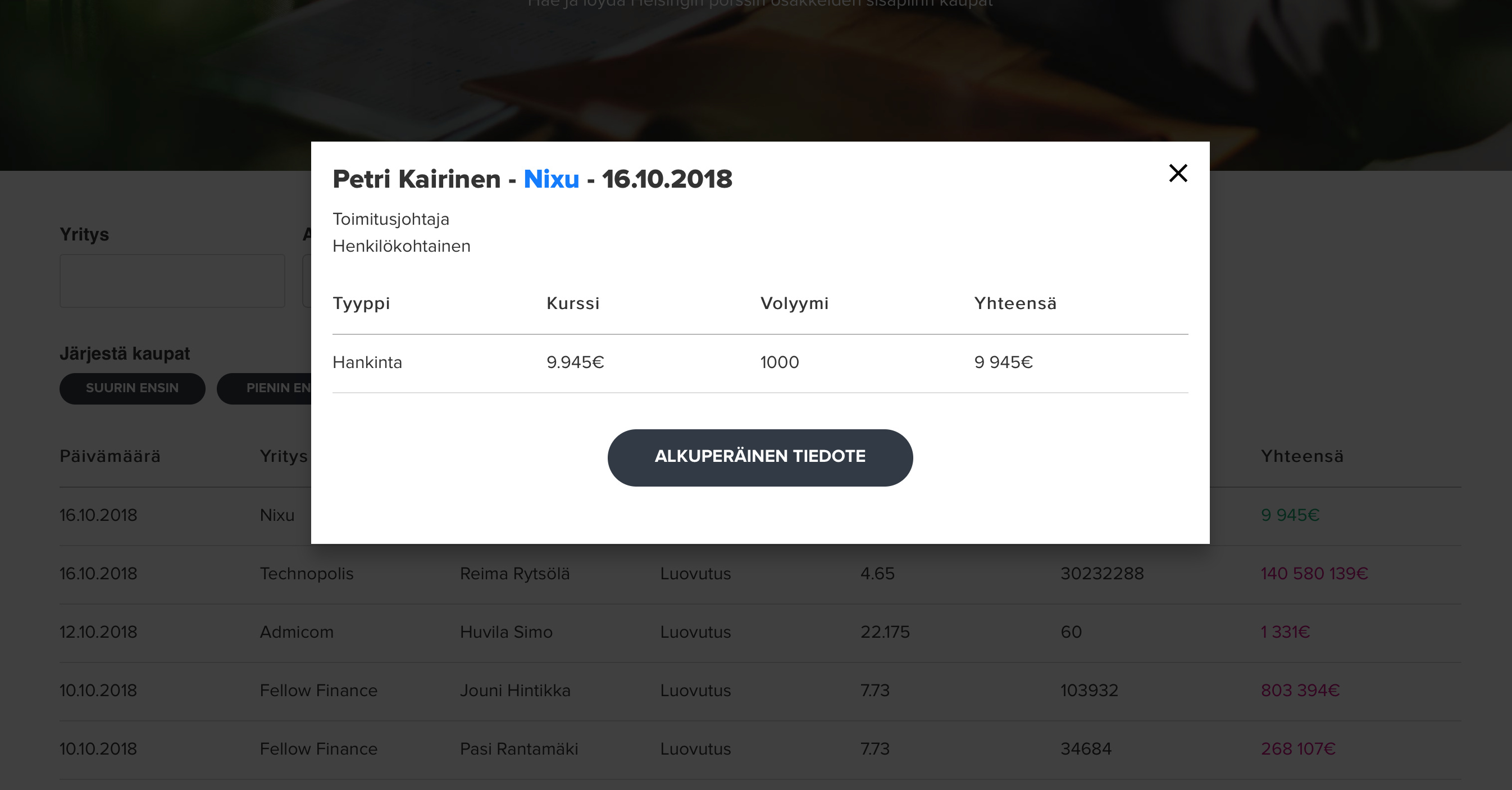

I noticed that Nixu’s CEO, Petri Kairinen, had bought about €10,000 worth of Nixu shares just before the earnings release period. What do you think? Could it be a signal? I checked the insider trades.

4 Likes

Nixu already published its revenue figures yesterday, and Kairinen put on his buying pants today. In any case, it’s a vote of confidence. However, one shouldn’t make buying decisions based solely on these insider purchases.

4 Likes

In the H1 section, profitability improvement measures were promised, and such measures will inevitably slow down growth. So, there are two ways to look at this:

- If the 17% growth seen in the beginning of the year could be achieved in Q3 despite applying the brakes, and profitability also clearly improved, then that sounds very good.

- If the brakes are only applied in Q4, meaning this growth comes with H1’s profitability, then I share Inderes’ concern.

It’s difficult to assess without seeing the EBITDA, so we’ll be wiser after Christmas.

Regarding insider purchases: I recall Inderes moving to a “reduce” stance on Innofactor this spring, cutting the target price sharply at the same time. Shortly after this, CEO Ensio bought a significant amount of shares, and since then, the share price has fallen by about a third. Hopefully, Kairinen fares better ![]()

4 Likes

I also noticed Petri’s (Petri) purchases right after we lowered our target price ![]()

In my opinion, it’s a well-managed and well-led company; I have no issues with the management’s trustworthiness, having followed the company since its listing. As an investor, I would currently pay attention to the possibility of a small “digestion phase” after the rapid growth seen in recent years. The company has grown aggressively, especially abroad and through acquisitions. Now, there are small signs in profitability that suggest the machinery needs to be fine-tuned occasionally to keep it in top shape so that strong growth can continue. Currently, the combination of growth and profitability is weak, but I expect the situation to look very different in 12 months. However, the risk is elevated as long as aggressive growth has been sought abroad through acquisitions, and the profitability of international operations is clearly in the negative.

The long-term story is strong, which is why it holds a small slice in my own portfolio, even though I have reduced my position this year.

5 Likes

I agree with Ritva. It’s hard to say anything about the CEO’s salary, but it’s bound to be mostly a symbolic gesture to compensate for the fact that there wasn’t much positive to say (at least not publicly) in the earnings report.

The CEO’s actions are partly negated by the fact that both the board and the management team have a couple of individuals with no ownership, and no one except Kairi has bought (or sold) anything in two years. DNV Cyber

3 Likes

Looking at the news flow from peers (Vincit’s zero growth, Siili’s negative outlook, F-Secure’s negative outlook), Nixu’s performance published on Monday doesn’t seem bad at all in relative terms.

4 Likes

Well, Nixu just gave a negative outlook, although Inderes probably already expected it:

“The company’s EBITDA was previously estimated to be low but slightly positive in 2018. Based on preliminary unaudited information, EBITDA is now estimated to be slightly negative. This is affected by several unrelated factors. The biggest change from before was the costs of a service development project implemented during the first half of the year and written down at the end of the year (approx. €100k). In addition to this, the company’s result will be burdened by the write-down of goodwill (€372k) regarding the customer value of the acquired ESSC BV, due to one large but non-strategic customer terminating its contract at the end of 2018.”

If I read that correctly, in an exaggerated sense, the much-hyped growth investment has been written down (i.e., failed), and too much was paid for the acquisition?

1 Like

Nixu has clearly read Nokia’s playbook. The announcement attempts to shift focus to future improvements. Over 20 percent organic growth and a clearly positive operating margin undoubtedly sound good; now it just needs to be achieved.

The warning came quite late. At least the write-down resulting from the contract’s termination should have been known earlier. Hopefully, this doesn’t indicate communication problems between the operating countries and parent company Nixu. Otherwise, this leaves an even cautiously positive impression due to the strong 2019 guidance.

I was thinking the same thing, that it’s not a very negative negative.

Guidance is guidance. A year ago, in February-March, the guidance for 2018 was as follows:

"Financial guidance for 2018

Nixu continues to aim for profitable growth and faster growth than its operating markets. The mid-term goal is over 15% annual revenue growth and over 10% EBITDA level.

Driven by strong organic growth and completed acquisitions, the company aims for significantly faster revenue growth in the 2018 financial year than its mid-term target. We will continue growth investments during the current financial year, which is why the EBITDA is estimated to remain below the mid-term target."

So, there was positive guidance back then too, but profitability was not achieved (revenue growth was). I personally suspect that the same risk exists for this year and that growth is not yet profitable enough to support the stock price. Therefore, I am not in a hurry to buy (more) shares, even if I were to speculate that consolidation would occur (in the role of buyer or seller). I will get involved more significantly when management proves it can achieve profitability, not just expensive growth.

Does anyone have a precise view on whether the growth comes through price competition or why profitability weakens even though revenue increases?

3 Likes

I recall Kairinen stating in interviews that the healthy margin level of the core business has not been compromised. The development of technology-based services requires investments, and when these are not capitalized on the balance sheet, the reported profitability during the growth phase suffers. Furthermore, the parent company has been generating positive EBITDA for some time, and net losses are coming from abroad – which is, of course, somewhat concerning, and I, for one, am keenly awaiting new data on this development. Proving the profitability of international growth would, in my opinion, justify the return of a “cybersecurity premium” to the stock’s pricing, but based on the H1’18 results, there is still a lot of work to be done.

3 Likes

Good comments and observations! I’d say that 2018 was a “digestion year” after the M&A and strong growth phase (plus the main list transfer burdened the company quite a bit), and at the same time, the stock returned to reasonable levels from overvaluation. Now the company is getting back on its normal growth trajectory, and the stock has returned to more sensible prices. As a long-term case, it’s starting to look more attractive again, although the company doesn’t yet have proof of a turnaround in profitability… so that’s needed this year to confirm that the challenges are short-term rather than structural.

2 Likes

Nixu’s growth seems to be keeping analysts busy day and night, as a quick comment was posted at 5:53 AM. I had already been wondering where Inderes’ perception of less than 20% organic growth for the current year, as presented in their last company report, came from, but the latest release put an end to that, and forecasts are once again under upward pressure.

The new deals sound strategically very compatible, but evidence of the successful profitability turnaround of international operations is needed in general before one can jump for joy due to new acquisitions. Of course, there is faith in this, so I view these acquisitions with a fundamentally positive attitude.

Nixu’s new option program, by the way, sounds good to an owner’s ear: options are granted if 1) one participates in the personnel offering, i.e., puts their own skin in the game, and 2) the company achieves its growth and customer and employee satisfaction targets. Since the subscription price is based on the share price without discounts or free distributions, the option will likely be worthless if the above targets are not achieved profitably, so this perspective is also taken into account. In other words, if the management succeeds in getting rich with options, everyone else will benefit too.

2 Likes

This is the million-dollar question. Is this a threat or an opportunity? Historically, these acquisitions have not gone 100% smoothly (cf. H2 write-downs and weakening profitability). Of course, that doesn’t mean they won’t succeed - but I often wonder that the seller always tends to have more information than the buyer. ![]()

I mostly agree with this. What has puzzled me is the share of free riders in the current board and management team. Until now, they haven’t been interested in buying, even though the CEO praised it as cheap on Twitter in the autumn. Apparently, this program has been in the works for some time, and they have been waiting for it?

It’s worth noting that to fulfill the option conditions, one doesn’t need to make a single euro of profit. The criteria were satisfaction (customer and employee) and revenue. Of course, Mr. Market will hopefully ensure that one only gets rich if shareholder value (whatever that may be) is created.

2 Likes

Inde got Nixuun going ![]()

But the stock price faded…

…and it’s off to the races again.

+6.67% EUR 11.20 24.5. 15:58

Quite a rollercoaster in one day.

1 Like

So, the guys at Inderes have a vested interest here, as we can see from the forum. This is semi-interesting… if not fully, there could be some suction here…

Hello everyone, Petri from Nixu here. Since I found such a well-named thread here, I decided to join the discussion.

We decided to try to serve private investors through this Inderes discussion forum, so that investors can get answers to similar questions that institutional investors can ask in their own events.

As a pilot, I commit to being active on the forum until the end of September and answering questions with reasonable notice. In practice, an answer may take a day or two, and additionally, we cannot comment on some matters unless they have been officially reported. You probably noticed that the H1 earnings release is now out, and you are welcome to ask about it and related topics!

34 Likes

Great, Petri. Welcome ![]() Here, only a few companies have individuals participating in the discussion for work purposes. Yes, there are questions, and a potentially delayed response time is also fine. First things first…

Here, only a few companies have individuals participating in the discussion for work purposes. Yes, there are questions, and a potentially delayed response time is also fine. First things first…

Congratulations also on the excellent turnaround in results. As investors, we seek growth, but profitability would also be a nice thing.

Now to the questions.

What do you think, could a merger between F-Secure and Nixu work? You come from different directions, F-Secure from the product side and Nixu from the services side, roughly speaking. I understood from the earnings release that you are also interested in sellable products.

Second. What is your growth target? Is there a market size where it’s easier to be (more) profitable?

Third. Is Nixu’s goal to (first grow big and) then be acquired? Lately, many great Finnish companies have transferred to foreign ownership. Have you been courted?

These are not directly related to the earnings release, but I would be interested to hear. Of course, I understand if there are restrictions on answers.

12 Likes