Mietin tässä, että pitäisikö ottaa 78% ja 15k turskat tästä. vai vieläkö jaksaisi uskoa tähän. Melkein tekisi mieli myydä kaikki pois, mutta toisaalta tässä vaiheessa ei se nyt niin merkittävästi huonompi ola, vaikka ei myisikään ja laskisi vielä 100%

Joku muu ketju varmaa kuvastaisi tätä enemmän, mutta varmasti enemmän vähemmän samassa veneessä ollaan me bagholderit. Itse vannotin, että katson 2025 vuoteen tämän casen ja katson kannattavuuden yms kehitystä josko ois parempaan suuntaan ja jos ei niin otan vähennyksinä. Ei tuo suunta ainakaan minua ole vakuuttanut vaikka oikeita elementtejä on. Kannattavuus ei vaan ole toistaiseksi parantunut ja bswap yhteistyöt eivät ole kantaneet niin paljon hedelmää mitä olisin uskaltanut toivoa. Tällä burn ratella ollaan kohta uuden annin äärellä…

Mutta ei siinä, ei kukaan täällä voi mitään suositella niin sinun pitää tehdä oma päätös mille haluat ruveta tämän kanssa ![]()

Joo, kaukana ollaan siitä, mitä toivottiin aikanaan. Mutta yhä uskon siihen, että noi BSwap yhteistyöt tuo kyllä “juoksevaa revenueta” jatkossa. Siitähän on ollut myös puhetta, että noi voisivat olla “varavirtalähteinä”, vai miten sitä ei sähköalaa opiskellut voisi kuvata.

Kilpailuhan on hurjaa autoissa, volyymibisnestä. ET9 on huima vekotin, katsotaan vaan miten saavat sitä myytyä.

Joo onhan tosta ollu puhetta, että ne tukis kriittistä infraa ja siitä varmaan jotain pientä korvausta vois tulla. Yhteistyöt varmasti jotain tulee tuottamaan, mutta kysymys on kauanko siihen menee. Kaikki maksaa ja jos rahaa ei tule, on se sijoittajan lompakolle tympiä juttu.

Et9 on siisti peli, mutta skaalautuvaisuuden nimissä toivoisin, että enemmän laitettaisiin bswappii paukkuja kuin autojen kehitykseen.

NIO Inc. antaa helmikuun 2025 toimituspäivityksen

- 13 192 ajoneuvoa toimitettiin helmikuussa 2025, kasvua 62,2 % edellisvuodesta

- 27 055 ajoneuvoa toimitettiin kumulatiivisesti vuoden 2025 alusta, kasvua 48,8 % edellisvuodesta

- *Kumulatiiviset toimitukset saavuttivat 698 619 kappaletta

7 tykkäystä

Näillä näkymin. Mikä meni vikaan Niolla.

Ihan lyhyesti vaan, kiitti.

Ehkä nyt menee parempaan suuntaan ![]()

Nio Stock Rallies On Partnership With CATL To Develop Battery Swap Network: Retail Turns Extremely Bullish

2 tykkäystä

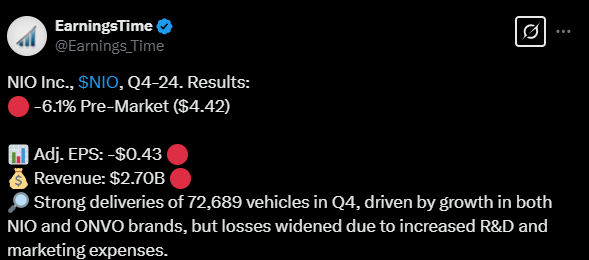

NIO:n tulos jäi jälleen odotuksista ja kannattavuushaasteet jatkuivat korkeiden kehitys- ja laajentumiskulujen vuoksi.

Yhtiö erottuu akkukennonvaihtoteknologiallaan, mutta kova kilpailu Teslan, BYD:n ja muiden kiinalaisvalmistajien kanssa vaikeuttaa yhtiön asemaa markkinoilla. Euroopan laajentuminen etenee, mutta taloudellisen tilanteen kestävyys herättää huolta.

https://x.com/Earnings_Time/status/1903033053875753415

2 tykkäystä

Erottuuko positiivisesti vai negatiivisesti maailmassa jossa ladataan megawattiteholla akkuja? Alkaa näyttää siltä että rahaa on heitetty kankkulan kaivoon oikein olan takaa.

2 tykkäystä

AI analyysi Nion huipusta ja nyt aallokon pohjassa;

Nio oli aiemmin todella paljon hypetetty osake ja yritys mediassa. Vuosina 2018–2020, NYSE-listautumisen ja varhaisten menestysten, kuten EP9-superauton ja kasvavien toimitusten myötä, Nio oli kuuma puheenaihe. Media rakasti korostaa heidän premium-asemaansa, akunvaihtoteknologiaansa ja kunnianhimoisia suunnitelmiaan, ja heitä kutsuttiin usein Kiinan “Tesla-tappajaksi”. Viime aikoina kuitenkin heistä on ollut hiljaisempaa, ja siihen on useita syitä.

Ensinnäkin Nion taloudellinen tilanne ei ole vastannut odotuksia. Vaikka heidän tulonsa vuonna 2024 olivat 9 miljardia dollaria (65,7 miljardia RMB) ja he toimittivat 221 970 ajoneuvoa (viimeisimmän raportin mukaan 21. maaliskuuta 2025), he raportoivat edelleen suuria tappioita – arviolta 3,4 miljardia dollaria koko vuodelta 2024. Se on parannus aiempiin vuosiin verrattuna, mutta ei riitä vakuuttamaan sijoittajia tai mediaa nopeasta käänteestä. Verrattuna kilpailijoihin, kuten Xpengiin, joka on pienentänyt tappioitaan nopeammin, tai BYD:hen, joka on jo kannattava, Nio vaikuttaa vähemmän tehokkaalta, mikä on laimentanut innostusta.

Toiseksi Kiinan sähköautomarkkinoiden kilpailu on räjähtänyt käsiin. Tesla, BYD, Li Auto ja Xpeng ovat vieneet paljon huomiota, erityisesti kun Tesla laskee hintoja ja BYD hallitsee volyymisegmenttiä. Nion keskittyminen premium-luokkaan ja akunvaihtoasemiin (yli 2 470 asennettua toukokuuhun 2024 mennessä) on ainutlaatuista, mutta se ei ole riittänyt pitämään heitä median keskipisteessä, kun halvempi vaihtoehdot valtaavat markkinoita. Onvon ja Fireflyn lanseeraukset osoittavat, että he yrittävät laajentua, mutta myynnin vaikutus ei ole vielä tarpeeksi vahva herättämään otsikoita.

Lopuksi Nion osakekurssi, joka nousi huippuunsa noin 55 dollariin vuonna 2021, on laskenut noin 4,50 dollariin maaliskuussa 2025 (Forbesin ja Yahoo Financen mukaan). Tämä heijastaa jäähtynyttä sijoittajien kiinnostusta ja vähemmän draamaa raportoitavaksi verrattuna aiempaan vuoristorataan. Media jahtaa usein seuraavaa suurta tarinaa, ja Nio on siirtynyt haastajasta yritykseksi, joka kamppailee todistaakseen pitkäaikaisen selviytymisensä.

Nio ei ole täysin unohdettu – he edistyvät, kuten CATL:n kanssa solmitun akunvaihtoteknologian kumppanuuden (ilmoitettu 18. maaliskuuta 2025) ja ET9-toimitusten aloittamisen myötä maaliskuussa – mutta ilman kannattavuutta tai räjähdysmäistä kasvua he ovat menettäneet asemansa median lemmikkinä.

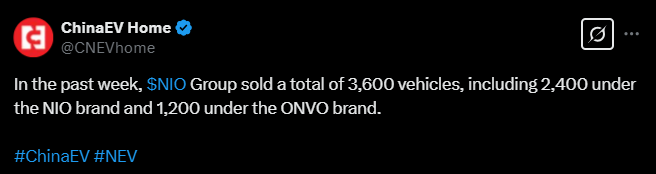

Tässä on tviitti NIO:n viime viikolla myydyistä autoista.

https://x.com/CNEVhome/status/1904432059634127280

__

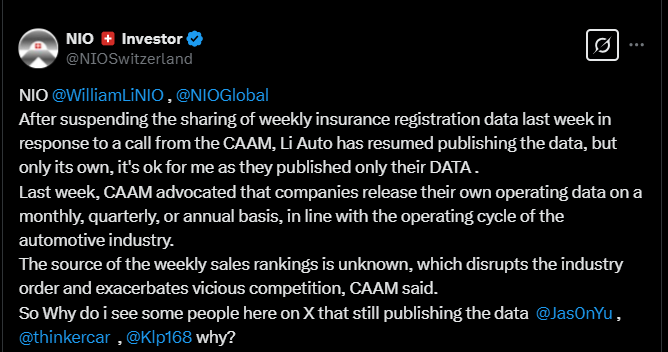

Laitan myös tämän mielenkiintoisen tviitin tähän.

https://x.com/NIOSwitzerland/status/1904423330301587923

1 tykkäys

Miksei BYD näy taulukoissa, muuten hyvä. Tai onko mukana vain puhtaat EV valmistajat.

Kai tämä on kuin kiroilisi kirkossa mutta todellisuus on joskus aika kova. Selviääkö Nio taloudellisista vaikeuksista tai meneekö …

1 tykkäys

Karua on EV-peli nyt Niolla. Haistelee 2 usd hintaa.

Nio oli melkein tuplasti suurempi market cap kuin Xpevillä ja nyt Nio markkinaarvo ei ole edes puoletkaan Xpengin arvosta.

Onkohan konkka tulossa?

Mitä Stocklover uskoo, onko jotain hihassa vielä ?

Kovasti on tariffit lyöneet sekä Xpengiin sekä Nioon, kummatkaan ei tietääkseni ole sen suurempaa satsannut jenkkimarkkinoihin, jotain oli Niolla vuosia sitten mutta kai sekin valui hiekkaan ?

Eli kai se sitten johtuu tästä “kauppasodasta” USA vs Kiina.

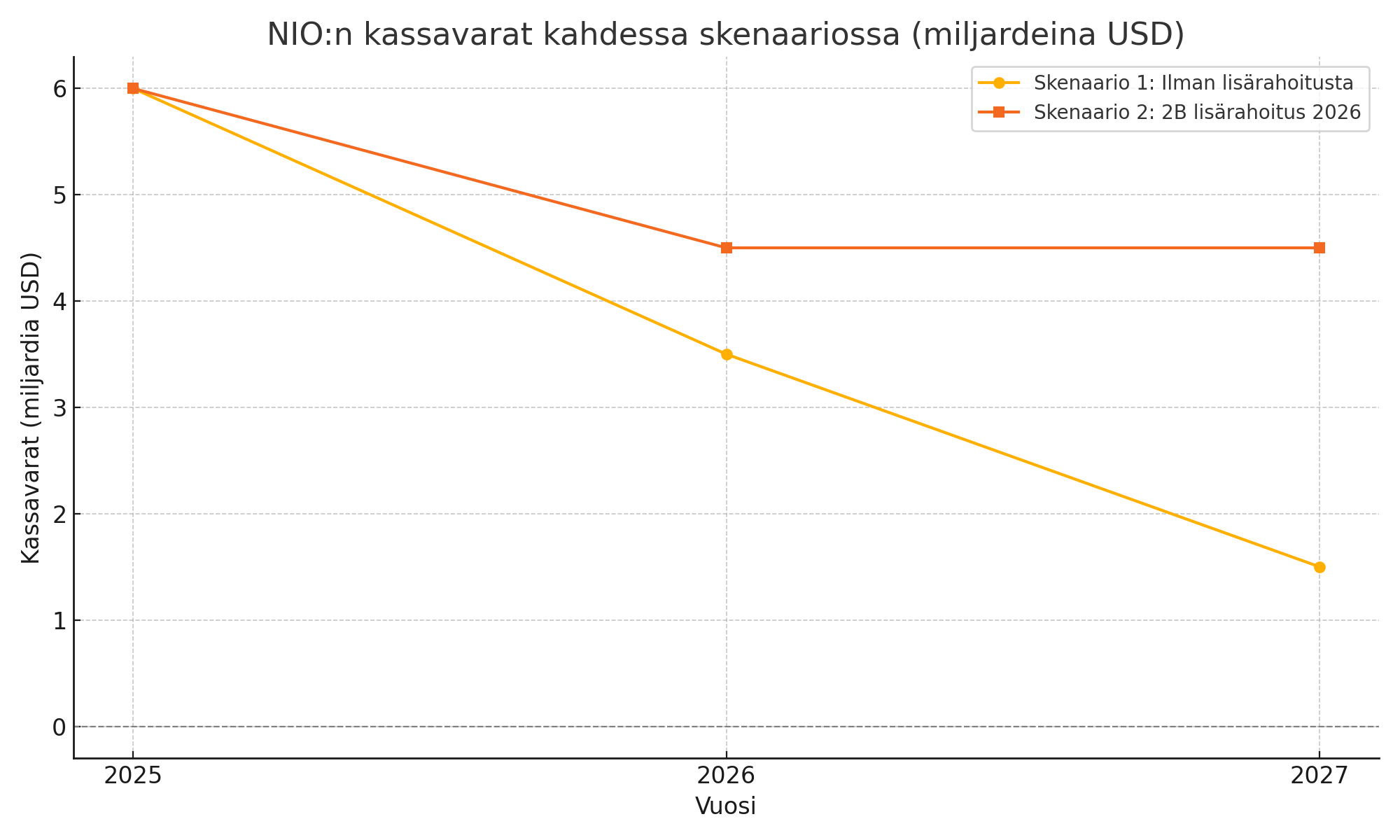

Pientä pohdintaa Nion kassavarojen riittävyydestä.

Toimia tarvitaan, jotta Niosta tulisi vihdoin kannattava.

Yritys hakee edelleen tosi rajua kasvua, joka polttaa kassaa.

NIO Inc.: Kassavarojen tulevaisuus kahdessa skenaariossa

NIO Inc. on kiinalainen sähköautovalmistaja, joka kamppailee kasvun ja kannattavuuden tasapainon kanssa. Yhtiön kassatilanne ja kyky rahoittaa toimintaansa ovat keskeisiä tekijöitä sen tulevaisuuden kannalta. Alla kaksi realistista skenaariota NIO:n kassavirran kehittymisestä vuoteen 2027 asti.

Skenaario 1: Nykyinen kulutustaso, ei lisärahoitusta

Skenaario 1: Nykyinen kulutustaso, ei lisärahoitusta

- Lähtökassa: 6,0 miljardia USD

- Kvartaali-tappio: 721 miljoonaa USD (n. 240 M USD/kk)

- Tappio pienenee ~20 % vuodessa

- Kassavirtaneutraalius saavutetaan: alkuvuodesta 2027

| Vuosi | Tappio / kvartaali | Tappio / vuosi | Jäljellä oleva kassa |

|---|---|---|---|

| 2025 | 721 → 577 M | ~2,5 B | 3,5 B |

| 2026 | 577 → 462 M | ~2,0 B | 1,5 B |

| 2027 | Neutraali | 0 | 1,5 B (säästyy) |

![]() Johtopäätös: Kassa riittää juuri ja juuri, mutta vaatii merkittävää tappioiden leikkaamista.

Johtopäätös: Kassa riittää juuri ja juuri, mutta vaatii merkittävää tappioiden leikkaamista.

Skenaario 2: Lisärahoitus 2 miljardilla vuonna 2026

Skenaario 2: Lisärahoitus 2 miljardilla vuonna 2026

- Sama alkuoletus kuin skenaario 1

- Tappiot pienenevät hitaammin (~15 %/vuosi)

- Lisärahoitus: 2,0 miljardia USD vuoden 2026 puolivälissä

- Kassavirtaneutraalius saavutetaan: vuoden 2027 lopussa

| Vuosi | Tappio / kvartaali | Tappio / vuosi | Kassa (loppuvuosi) |

|---|---|---|---|

| 2025 | 721 → 613 M | ~2,45 B | 3,55 B |

| 2026 | 613 → 521 M | ~2,10 B | 4,50 B (sis. rahoitus) |

| 2027 | Neutraali | 0 | 4,50 B |

![]() Johtopäätös: Lisärahoitus tuo turvaa, mahdollistaa investoinnit ja pienentää riskejä.

Johtopäätös: Lisärahoitus tuo turvaa, mahdollistaa investoinnit ja pienentää riskejä.

Visualisointi: Kassakehitys skenaarioittain

Visualisointi: Kassakehitys skenaarioittain

![Kassavarat kahdessa skenaariossa]

Sijoittajan näkökulma

Sijoittajan näkökulma

| Skenaario | Plussat | Miinukset |

|---|---|---|

| Ilman lisärahoitusta | Ei diluutiota, vaatii sisäisiä tehostamistoimia | Vähäinen liikkumavara, korkea riski |

| Lisärahoituksella | Vakaampi kassa, mahdollistaa kasvun jatkumisen | Mahdollinen osakeannin laimennusvaikutus |

3 tykkäystä

Jos worst case scenario tapahtuu Niolle, mitä arvaat että tapahtuu seuraavaksi koskien entistä Nioa?

Tiistaina 3.6. NIO:n Q1 tulokset ennen avausta.

Autotoimitukset Y/Y +40.07% ja Q/Q -42.09%.

Toimitukset 42,094 osui ohjeistushaarukan 41,000-43,000 keskelle.

Q1 toimitukset ollut NIO:lle aina hiljaisempia. Kuitenkin koko historian kuudenneksi korkeimmat toimitukset tähän kohtaan antaa ihan hyvän lähtökohdan koko vuodelle.

Itse odotan tulokselta enemmän NIO:n kulurakennetta ja sitä onko nettotappiot kaventuneet yhtään.

5 tykkäystä

NIOn toimitettujen sähköautojen määrä nousi reippaasti ml. uusi ONVO-brändi ja Firefly-malli.

Yhtiö esitteli uusia teknologioita ja keräsi pääomaa toimintojen sekä innovaatioiden tukemiseksi, lisäksi monia automalleja päivitettiin ja toimitukset laajentuivat.

https://x.com/earnings_guy/status/1929861483573227874

4 tykkäystä

Voitto on aina voitto ![]()

![]()

“Volkswagen voitti siis innovaatioiden yleisen sarjan, mutta CAM julkaisee erikseen myös premium-merkkien rankingin. Vielä viime vuonna senkin voitto meni Saksaan, mutta tänä vuonna voittaja vaihtui, kun kiinalainen Nio nousi ykköseksi 33,5 pisteellään. Nio pisteet olivat niin kovat, että niiden takana oli useita onnistuneita innovaatioita. Tärkeimpinä kuitenkin Nion puolikiinteät akut ET5- ja EC7-malleihin sekä valmistajan 1000 voltin latausasemat, jotka tarjoavat 640kW:n latauskapasiteetin.”

7 tykkäystä

"Yhtiö on korostanut useita kertoja tänä vuonna, että sen tavoitteena on saavuttaa ensimmäinen neljännesvuosivoittonsa tämän vuoden viimeisellä neljänneksellä.

Kaikki Nion ponnistelut keskittyvät tällä hetkellä perustan luomiseen tälle tavoitteelle todistaakseen liiketoimintamallinsa elinkelpoisuuden, ja L90, uutena mallina, jolla on potentiaalia tuottaa merkittävää myyntiä, on avainasemassa tässä."

4 tykkäystä