I am reposting my deleted message in the form of a question.

Accounts receivable were 3.7 million. Will this amount already be reflected in the 2025 results, or will it fall into the 2026 results?

I am reposting my deleted message in the form of a question.

Accounts receivable were 3.7 million. Will this amount already be reflected in the 2025 results, or will it fall into the 2026 results?

In the 2025 results, 2026 cash flow. 50 characters then for the year 2027.

An interesting takeaway from the webinar regarding new partnerships. Several negotiations are underway, with some already at the contract negotiation stage, but apparently, these processes take a long time. That was certainly the case with Brainlab and likely with Sinaptica as well.

What was being blathered in the webcast when the share price tanked even further? Another masterclass in communication?

Notes from the webcast. The sales pipeline is strong, new initiatives are underway, and the long-term expectation is 20% CAGR growth. Recurring revenue is slightly down in 2025. Customers have preferred direct hardware purchases over leasing.

Direct purchases still generate some recurring revenue, because after the one-year warranty period, customers usually continue with a maintenance agreement similar to the warranty. There are different levels of maintenance agreements available. In the future, recurring revenue is expected to increase as licensed software users of the NBS 6 equipment also generate recurring income.

Brainlab’s option to purchase shares expires within a year (03/2027). It would increase their ownership from 3% to 13%. It will be interesting to see how they will act.

In summary, the company is moving forward. I would describe the company as being at the bottom of a new growth cycle, provided everything goes according to expectations. A broader view on this in the Jan 6th message. Perhaps analyst Antti Siltanen hasn’t been as far off regarding the 2025 expectations as the forum suggested last year regarding the forecasts.

Indeed, in light of the results, even Antti was overly positive. It’s difficult to accept the 20% CAGR offered by management, as including last year, it would actually mean decelerating growth, since 25% growth was achieved last year. Management’s figures were challenged a bit in the webcast, but they said that 20% is very ambitious. Personally, given the size of the company, I strongly disagree. As noted in the webcast, even doubling current revenue will take years. Of course, forecasts are just forecasts, but now management has provided a clear percentage they are targeting; the actual outcome could therefore be lower or higher.

I expect Antti will soon confirm that the current valuation is outrageous with these figures/growth expectations. Too much of the share price is now reliant on complete wildcards (Sinaptica etc.). The current share price cannot hold based on the figures and targets provided.

This is a growth company, the product is highly competitive, and the gross margin is over 70%. These are always priced looking toward the future. This business is not, and will not be, some basic commodity play. It’s also worth realizing that the entire company’s value at the current share price is a ridiculous €93M. You don’t come across this kind of special offer often… I’m going to pick up some more for my portfolio from the bargain bin ![]()

Profitable growth is in sight as far as the eye can see. As a bonus, an Alzheimer’s booster and other new initiatives in the works… it’s a pleasure to wait for these while riding along with a quality company.

The Year of Scaling

Can’t find the webinar recording on the website? And filling the character count.

Quite interesting estimates.

I watched a couple of the company’s/Inderes’ earnings calls myself. I really didn’t see anything dramatic. The NBS6 and the one-year warranty period are a very natural explanation for the recurring revenue as well. After the year, the maintenance agreement kicks back in. This will have more of an impact in the coming quarters, as sales have shifted to the 6. It will, of course, correct itself in a couple of years when the warranty period for the 6s bought already and those bought this year expires.

For me, one very significant investment driver is the management. I have trusted Karvinen all along, and his words have held up well. Costs are under control. When I think about Karvinen’s comments today, I didn’t find any weaknesses there. A pro. He also knows the competitors quite well.

Some have gotten hung up on that 20% growth in their comments. Let’s clarify that the actual expression was over 20%. That has a clear significance.

Last comment on growth. It has been stable for years… regardless of global turmoil… Covid… Ukraine… tariffs, etc. Significant issues, and solid growth despite them. It just makes me wonder, what if we could go for a couple of years without major “hassles” in the world once the Ukraine situation is resolved? What would the growth % be then?

Finally, I should state that I am certainly not comparing the situation in Ukraine to business matters.

Have a nice investing spring everyone… spring for investors arrives on Monday when the markets open.

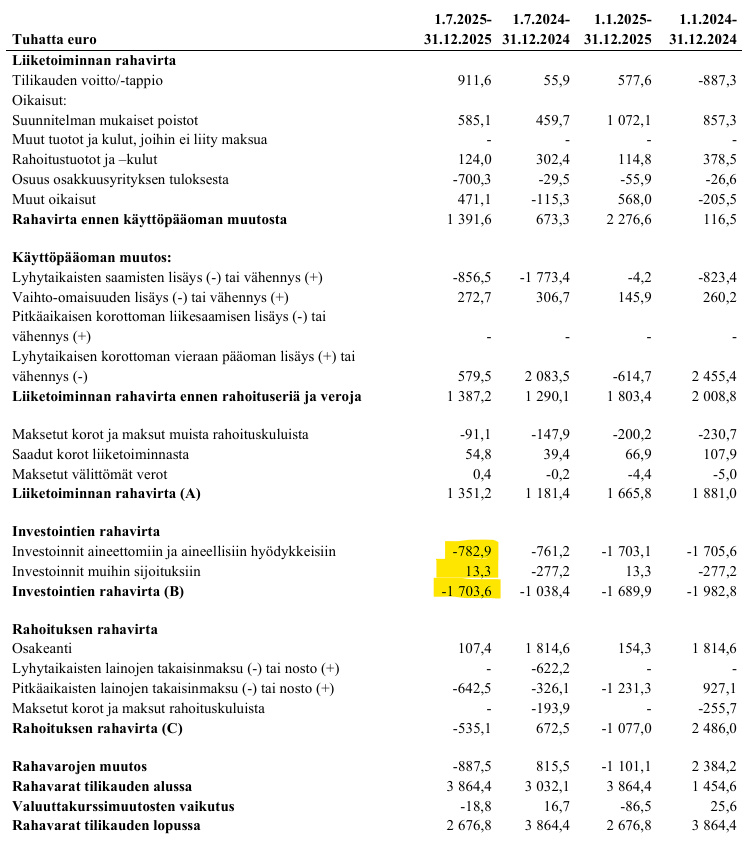

Looks like the cash flow from investing activities was calculated completely wrong. Surprisingly often you come across something like this with listed companies.

It’s just one of those things. I have to admit I’m a bit disappointed that Q4 didn’t perform in the same proportion as the start of the year; I was sure it would. ![]() hand up as a sign of a miscalculation.

hand up as a sign of a miscalculation.

Well, anyway. On the positive side, nothing dramatic happened and we are in the black. In the end, at this stage, it doesn’t matter much whether the EPS is 0.06 or 0.17. The CEO spoke for quite a while about negotiations regarding strategic partnerships and new treatments. These are the things that interest me the most, as long as the cash position holds up so we don’t have to seek more capital from shareholders. In my opinion, there’s no fear of this in the near future, because Brainlab also has options available and over 20% CAGR was promised.

Since it’s a growth company and the share count is moderate, the EPS will surely rise quickly when the time comes.

Good performance overall from Nexstim throughout the past year.![]()

Is there a mil more in the account now than what the report says, or what’s the situation?

Cash flow statements seem to be largely manual work in many places, so errors occur in these calculations.

In the balance sheet, the cash assets and the final total of the cash flow statement, 2676.8, are correct.

Target price €11.5 with an ADD recommendation.

Since I invest in the company rather than the share price, quarters don’t matter much unless something truly worrying appears in the numbers or the outlook. As far as I understand, nothing like that emerged yesterday. We even received a clear and logical explanation from the CEO as to why recurring revenue dipped momentarily.

Quoting and paraphrasing @Taitoo: “For me, one very significant investment driver is company management. I have trusted Karvinen all along, and his words have held up well. Costs are under control. When I think about Karvinen’s commentary today, I found no weaknesses there. A professional. He also knows the competitors quite well.”

This is also very important to me. Everything looked good and the targets/outlook also seemed understandably realistic. I wonder what kind of outcry and panic would break out among those “seeking quick riches” if the outlook were overstated and even a slight negative profit warning had to be issued?

Sinaptica on LinkedIn;

We are honored to have been selected as the winner of the MedTech World Pitch competition at the MedTech World Middle East conference in Dubai last week. See the comments from CEO Ken Mariash below following the win.

As precision medicine increasingly shapes the future of aging and longevity, we are proud to be leading at the intersection of neurotechnology and personalized neuromodulation, advancing data-driven, individualized approaches designed to support healthier brain aging and address the complex biology of Alzheimer’s disease and other neurodegenerative conditions.

This recognition reflects our team’s dedication and our commitment to transforming cutting-edge science into meaningful innovation for patients and families.

We are grateful to have been chosen from a strong field of visionary companies striving to redefine the possibilities of healthcare.

#DefaultModeNetwork (DMN) #PrecisionMedicine #Longevity #MedTech #MedicalDeviceInnovation #InnovationInHealthcare #ENDALZ