Opening a thread and discussion about an interesting health technology company on the Oslo Stock Exchange. Are there any Medistim investors on the forum?

Medistim ASA is a Norwegian listed company that develops, manufactures, and distributes medical devices primarily for cardiovascular surgery needs.

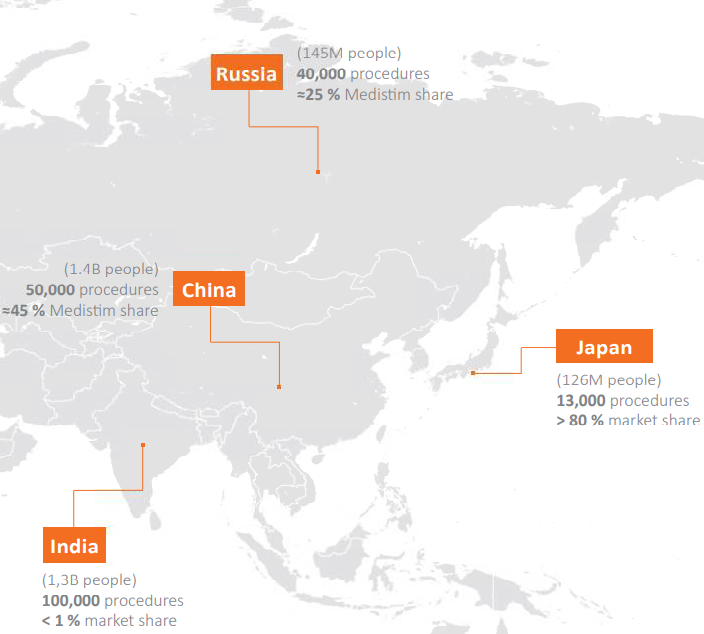

Medistim’s own products are considered the standard of care in most European countries and Japan, while market entry is only just beginning and growing in the United States, Asia, and the Middle East. Medistim is a market leader in intraoperative transit time flow measurement (TTFM) and ultrasound imaging. These systems allow medical professionals to reduce the risk of intraoperative complications during cardiac, vascular, and transplant surgeries. They provide clinically relevant information that enables surgeons to make better decisions in the operating room. The company’s devices are developed in close cooperation with surgeons.

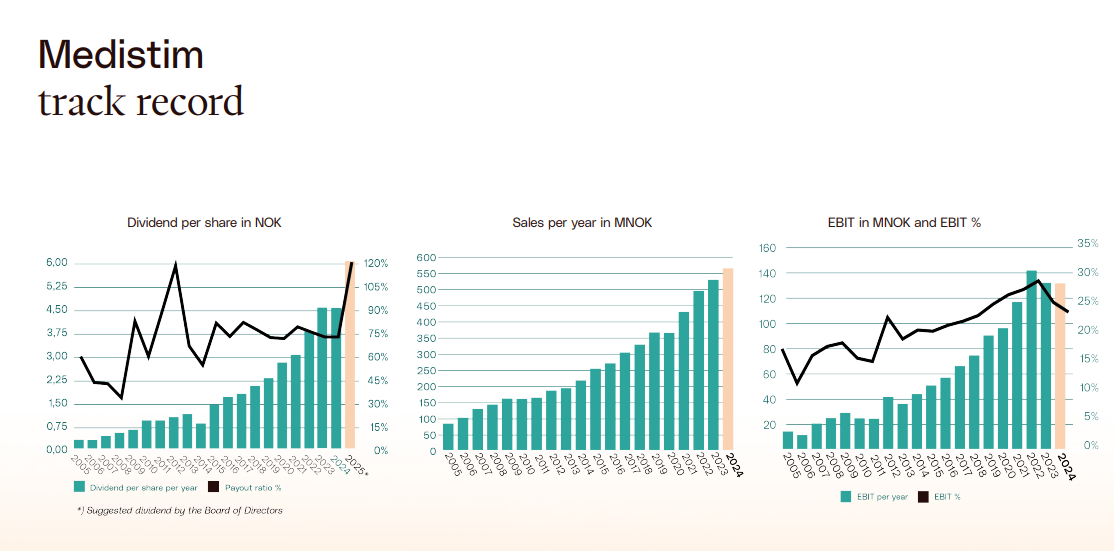

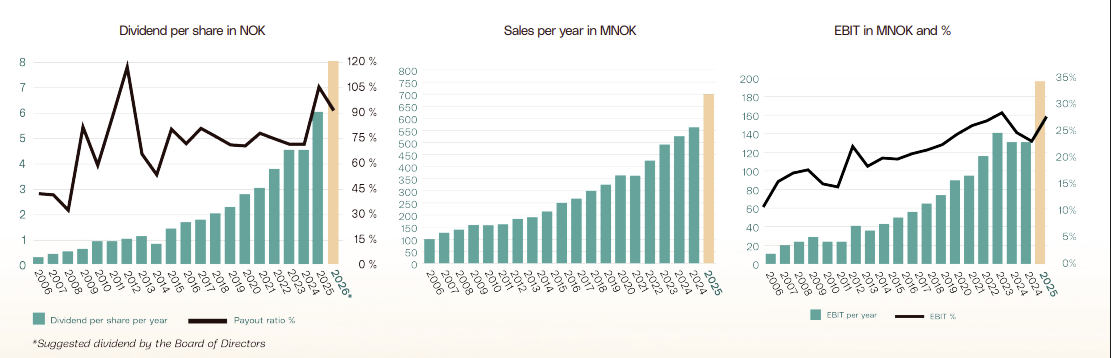

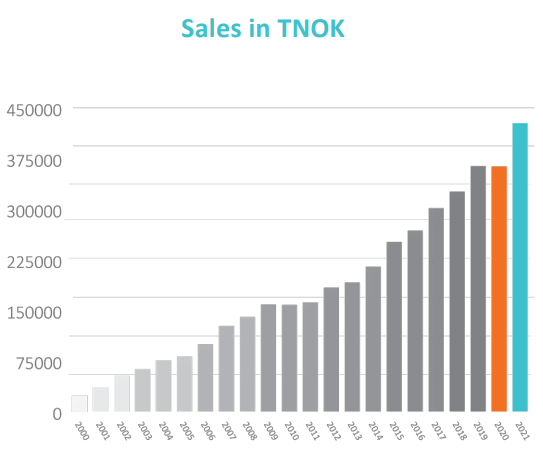

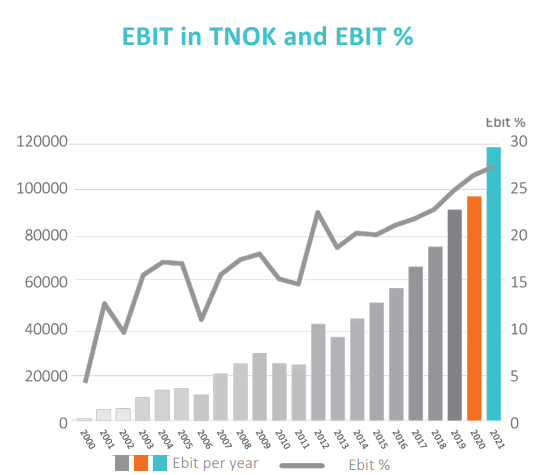

The small company is on a strong growth path. 2021 figures:

- Revenue 427 MNOK, Growth 17.7% (currency adjusted 24.6%)

- Operating profit 90.9 MNOK EBIT, Growth 21.8%

Sales of own products grew by 26%, of which sales of imaging portfolio products grew by 29% and vascular portfolio by 21%.

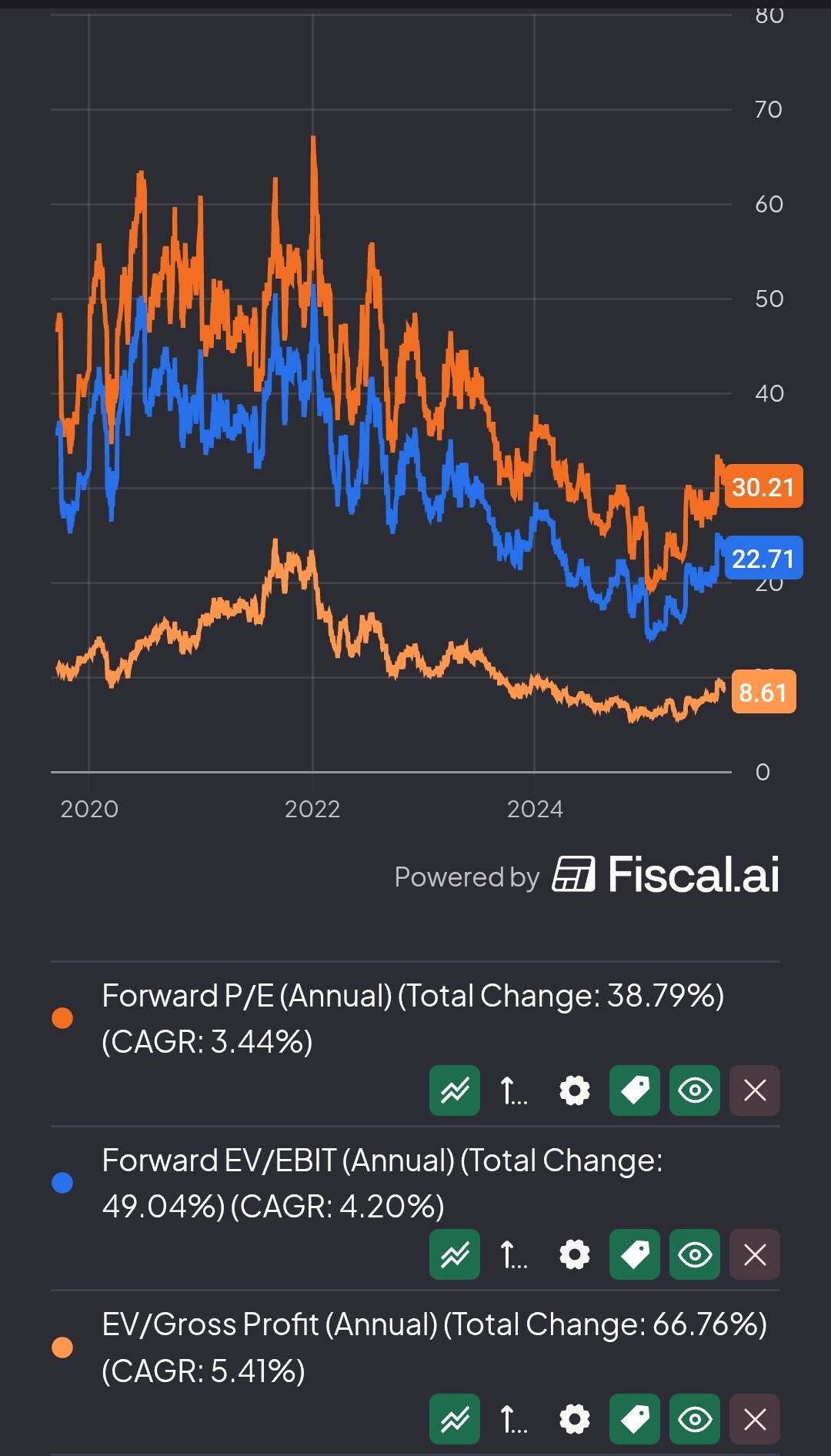

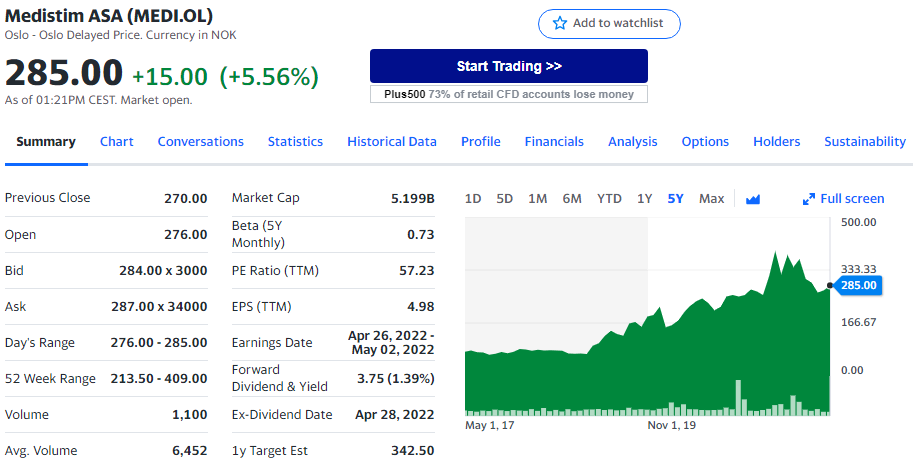

Share valuation on 4.4.2022 at a price of 285NOK PE: 57 with realized 2021 results

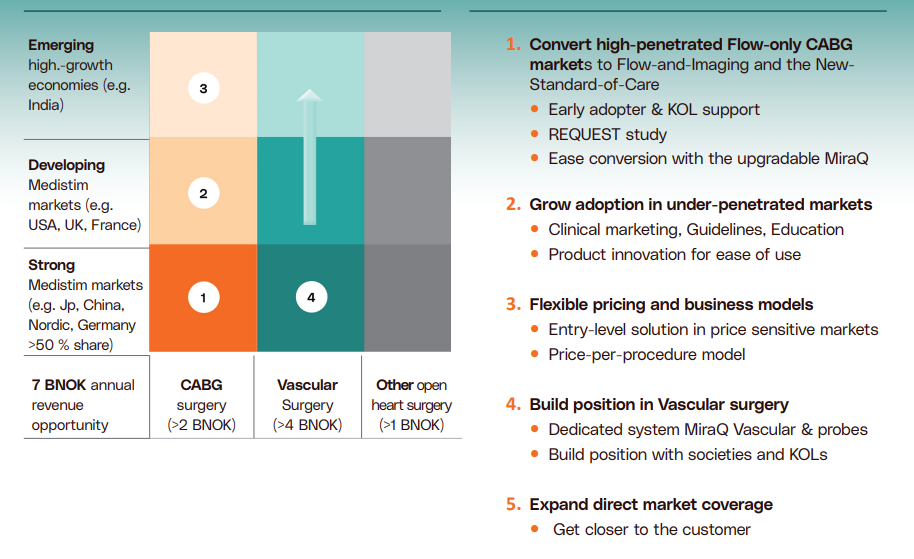

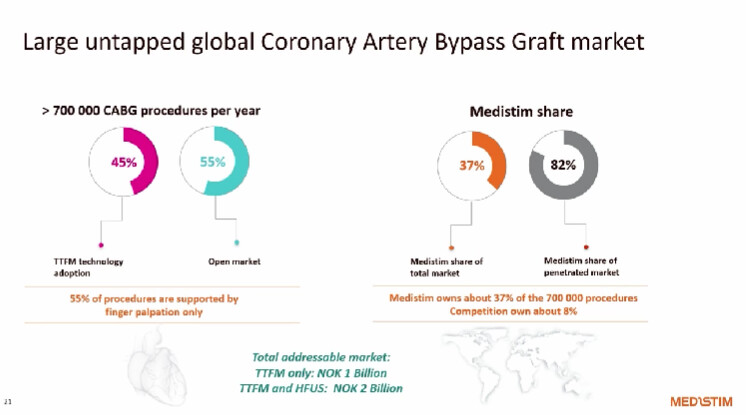

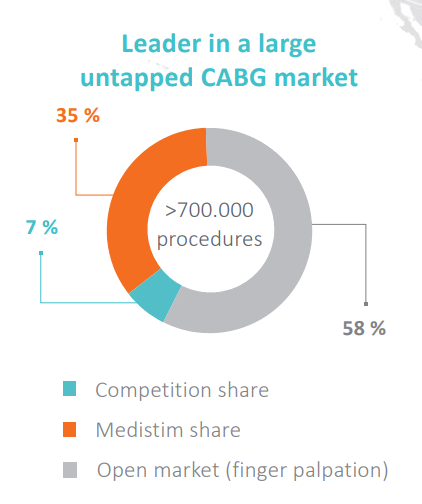

The company has room to grow globally. The company’s products are standard and market leaders in several European countries, but there is plenty of room for growth in, for example, the United States and emerging markets. For example, in India, the company holds an estimated only 1% market share. In the United States, the market share is approximately 28% and sales grew by 28% in USD terms in 2021.

Source: www.medistim.com

Excerpts from the 2021 annual report:

Revenue and operating profit:

The company’s goal is to maximize shareholder value creation. Dividends are paid when consistent with the growth strategy and financial objectives. In practice, the dividend has grown strongly:

Market shares:

Share price:

Ownership base: