In the analysis published today, the reduction in the target price was justified, among other things, as follows: “lower hardware sales volume than we forecast… sales weighting towards lower-priced therapy hardware compared to our forecast”. Brainlab was not mentioned at all, meaning Inderes’ interpretation is apparently that no devices have been sold through Brainlab because none have been announced. On the forums, however, the interpretation has been that these hardware sales figures will only be announced in connection with the results release. I wonder which interpretation is wrong?

10 Likes

Well, at the very least, Brainlab (and Nexstim) would have been incredibly unsuccessful in their sales efforts within Brainlab’s sector. The last 13 have been therapy, Finnish, or research deals. This would mean that since the start of Q4, zero diagnostic devices were sold in Brainlab’s sector.

Attending all those trade shows together, getting approvals, a 400-strong sales force selling, and then the end of the year turns out to be such a dud. I don’t believe it for a second.

15 Likes

Negotiations were opened during trade shows. The average sales cycle is over a year. No need to worry.

Brainlab started sales this year, and despite good relationships, the processes and bureaucracy on the buyer side are certainly quite rigid.

The results for this year are already good based on what has been reported, and I wouldn’t mind if we rely on the gross margin, leaving the deals to wait until next year. This kind of thinking only maximizes the money Nexstim receives.

1 Like

I really don’t believe that sales growth will slow down in 2026, considering nTMS has just had its clinical breakthrough. This is where the sales growth is only just beginning, and recurring revenue will increase as the number of devices grows.

Well, everyone draws their own conclusions.

8 Likes

Yeah, it wouldn’t even matter. But the claim that Brainlab sector sales were zero in Q4 is simply not true.

If there were 1 or 2 deals in the Brainlab sector, I could believe that things went poorly, but now that there are zero deals, it just isn’t true.

9 Likes

I was thinking about the trade shows. I wonder how much Nexstim benefits in its other sales from being featured alongside Brainlab?

Of course, that’s difficult to quantify, but the Brainlab “seal of quality” mentioned by the CEO and appearing alongside Brainlab at events builds credibility for the entire operation.

Previously, Nexstim’s problem has been a lack of brand awareness, rather than the device’s capabilities or even its price; the issue was that a small Finnish firm, even one struggling for survival, wasn’t seen as a sufficiently credible player. This increase in recognition and credibility might unexpectedly generate more demand for other business activities as well.

Personally, I think there is a tipping point in this scalability, and we are approaching it.

16 Likes

That Middle East deal is handled through a distributor, wasn’t it speculated here earlier that deals through a distributor are not reported?

1 Like

Sales made by Brainlab are not announced. That Middle East deal was for a therapy device, so it doesn’t involve Brainlab.

13 Likes

Research in a field where there would definitely be high demand for an effective treatment if a long-term effect could be achieved without medication.

I’ve been wondering a bit why Brainlab’s guaranteed sales margin for this year hasn’t been announced yet. It could be quite a significant positive profit warning when it’s released ![]()

3 Likes

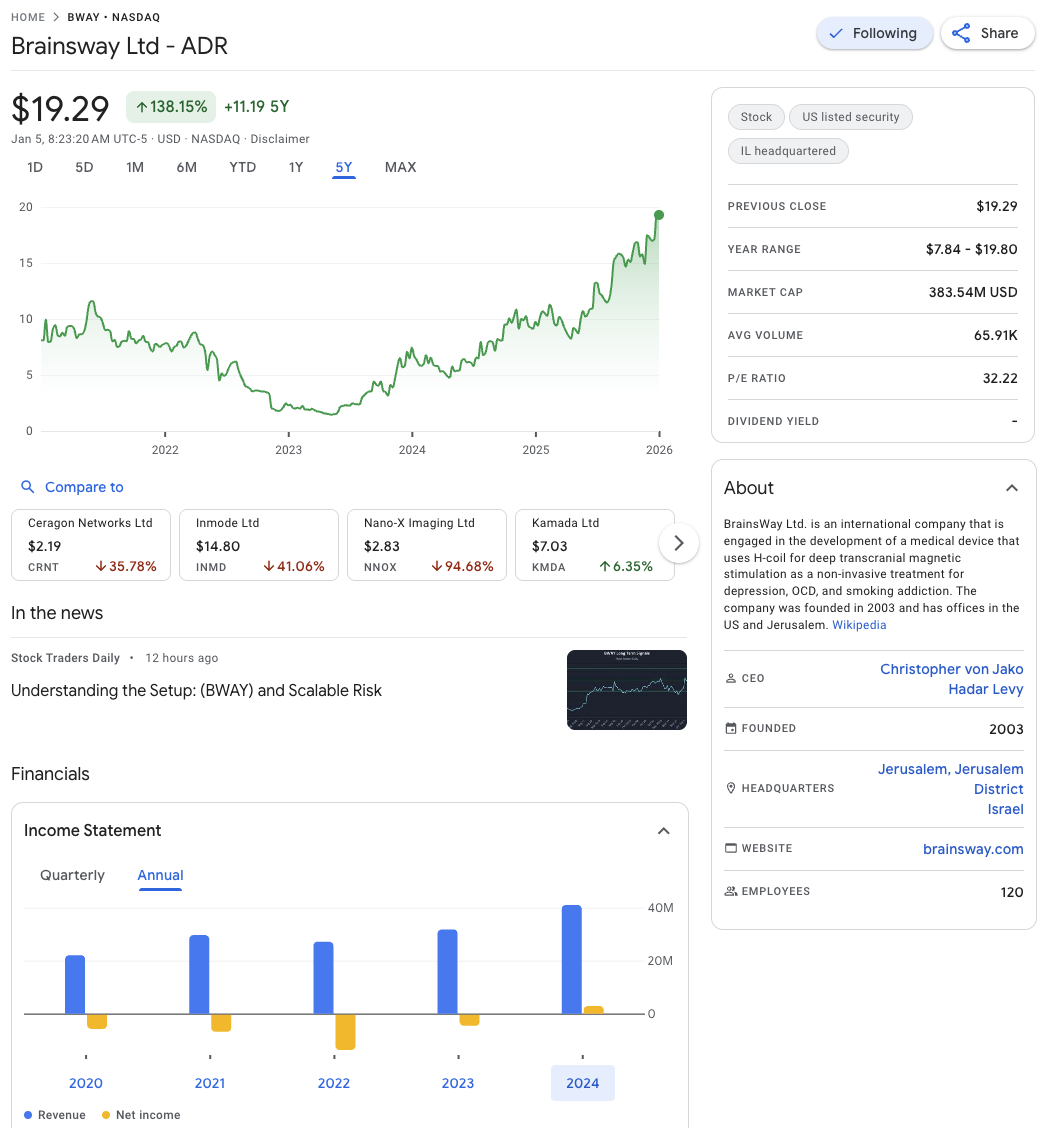

Of the main competitors, Brainsway’s market cap is already approaching the $400 million mark. The share price has risen quite significantly since the business turned profitable, and I expect a similar reaction for Nexstim as well.

23 Likes

Brainsway has a revenue of 41m, with a net profit of 2.9m in 2024. Nexstim seems to have a quite a bit better ratio in these.

My own crystal ball says that in addition to the deals announced so far, Brainlab has sold 10 devices in Q4, and in my opinion, 10 isn’t even an exaggerated figure, but an average one. 5 would be poor and 15 would be good.

Based on quick rough calculations, EPS could be 0.5-0.6, because not all devices will be delivered. For recurring revenue, I expect around 20% growth. So, I am in a much more positive mood than today’s Inderes analysis. Time will tell which estimate is correct. ![]()

18 Likes

@Antti_Siltanen a few questions about the report:

- you wrote: According to our understanding, Nexstim is also upgrading some of the previously sold NBS5 systems to new NBS6 systems, which we expect to cause moderate additional costs and weigh on H2’s gross margin.

I assume so myself, but I’m wondering what the basis is for this causing additional costs / weighing on the gross margin? Why would this be lower-margin work?

- The effect of the euro-dollar exchange rate on the lowering of forecasts also makes me wonder… doesn’t the company also have some expenses in dollars, so that this shouldn’t have a significant impact + a large part of the exchange rate change in question occurred before the summer, so is the reason behind your forecast changes that the weakening during the spring/summer simply hadn’t been accounted for in the report update after H1? In my view, the euro-dollar exchange rate has actually remained quite stable since the summer.

The report itself was otherwise a good read, and thank you for that.

1 Like

I don’t know if I’m remembering correctly, but to prevent everyone from just waiting for the NBS6 device, when purchasing an NBS5 device, they were promised a later upgrade to the newer one at a discount. This is what I recall Karvinen saying in an interview, but please correct me if I’m wrong. This naturally weighs slightly on the gross margin.

5 Likes

I’ve sketched out the coming years from my perspective and created a Google Sheet that you can copy for your own forecasts. You can open the spreadsheet and select File - Make a copy from the top left corner.

In that copy, you can then fill in the fields with the gray background with your own thoughts on the correct figures. The other fields are calculated using formulas, where I have tried to minimize the amount of speculation and include pessimistically realistic figures in the formulas. These can, of course, be challenged if you wish, and we can refine them if necessary.

In this published Sheet, I believe there is a fairly pessimistic outlook for the future, and for example, no more devices would be sold to Sinaptica in these calculations, but I don’t personally consider that a likely scenario. Similarly, the other sales volumes are, in my view, quite conservative, considering Brainlab’s massive sales and marketing resources, existing customers, the growing market, and strong research evidence regarding the necessity of the technology.

On the expense side, most costs come from variable expenses, which include sales commissions, device and supply manufacturing, and services. These have been taken into account via the gross margin in both new equipment sales and recurring revenue.

Let’s also set up a guessing game based on the table, using the share price section near the end.

Guess the share price at the close of the day the financial statements release is published for each year, and I’ll buy lunch in Helsinki for the person who guesses closest each year.

With those constant values from the table and a P/E 40 valuation, the share price would be:

2025 financial statements: €28

2026 financial statements: €60

2027 financial statements: €85

2028 financial statements: €112

2029 financial statements: €139

2030 financial statements: €168

24 Likes

Note that the margin and predictability should grow continuously through recurring consumables and maintenance services. I don’t know if you have taken this into account or not.

1 Like

Yes, I’ve worked through the recurring revenue in those lines 20-30. However, a “brake” of sorts has been added, where only 50% of recurring revenue is calculated for newly sold devices in the first year. The recurring revenue for 2025 is also surely on the low side, as it is largely based on the 2024 situation. It doesn’t take into account the large number of devices delivered at the end of the year.

So it is included, but likely pessimistic in many respects. I also personally believe that in the NBS 6 version, recurring revenue will play a larger role, e.g., through license fees.

4 Likes

When removing the annual sales of combined devices from the calculation, the company’s direction looks more realistic in my opinion. The potential growth in device sales in the coming years will likely be supported by, among others, Brainlab.

Otherwise, assuming Nexstim’s sales, distribution, and marketing organization remains at the same level as in previous years, I believe the sales volume will stay at the same level as this year, with the annual trend range being -5 to +12 devices compared to the previous year.

Building and expanding a partner network is a long process, especially in a relatively new market. Additionally, different geographical regions are at different stages.

Nexstim’s hospital, clinic, and research customers can be broadly classified into four stages:

1. Innovators

The market’s first users. Research-driven actors who develop new things and are interested in new treatment models.

2. Early adopters

Advanced actors who utilize early information.

3. Early majority

As the market matures, the solution becomes established as part of standardized treatment processes.

- Late majority

Smaller or individual actors once the treatment has become an established and recommended form of therapy.

What does this look like in practice?

-

In diagnostics, for example, the market is moving towards the end of the early adopter phase. Brainlab supports diagnostics device sales both here and in (3) the expansion of the early majority.

-

Depression treatment

Moving from innovators to early adopters, as evidenced by the growth of the clinic network.

3. Others

For example, Sinaptica. Approaching the beginning of the innovation phase.

4. The same can be applied geographically. For example, the Middle East is at a very early stage of the innovation phase.

Device upgrades will also provide support in the coming years when upgrading 3–6-year-old units from version 5 to 6, after which software for 6th-generation devices can be updated without the need to replace the hardware.

2 Likes

I don’t really see how that would increase realism? In 2025, sales of 13 NBS 5 combination devices and 3 NBS 6 combination devices were announced. I believe that in addition to those, more NBS 6 combination device sales might have been made in Brainlab’s territory that haven’t been announced.

Brainlab’s sales engine is going to get going properly this year, as this autumn Brainlab’s sales have already been able to influence customers’ 2026 budgets. I believe that device acquisitions have already been budgeted in several places for this year, but we’ll have to wait for information on closings.

4 Likes

I meant that by excluding the sales volume of combination devices, for example, the total volume of hardware sales for 2026 would be 41 units. In 2027, 44 units, and in 2028, 55 units.

In this case, -5 to +12 devices from the realized figure would mean 36–53 devices in 2026. In 2027, 39–56 devices.

Where the actual trade volumes settle will be clarified in the future. And I am happy to update my own views as well.

Thanks @Blindfolded_Monkey for the ideas and help with styling the table. Readability has been improved, and CAGR calculations have been added to the relevant sections. That CAGR really illustrates well how, with fairly moderate sales growth, the bottom line grows at a nice pace.

That recurring revenue is a great productive and stabilizing component in Nexstim.

The styled table can be found at the same link: Nexstim - Arvaus tulevien vuosien kehityksestä - Google Sheets

11 Likes