Netcompany has been at the very forefront of the European IT services sector for years. Organic growth has been good, and profitability, in particular, has been strong. The company has approximately 9,500 experts, and for comparison, Tietoevry has just under 15,000, Gofore 1,700, and Siili just under 1,000 experts at the end of Q3’25.

Overview

Business Area: Netcompany is a Danish IT services company specializing in critical IT projects related to digital transformation. It offers services for the development and implementation of digital platforms, core systems, and infrastructure.

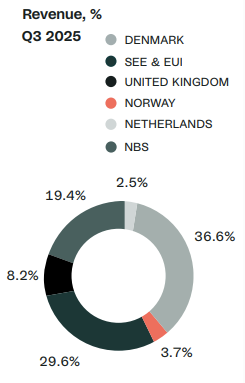

Clients: Netcompany serves both public and private sector clients. For example, in Denmark, it has achieved a strong position in the public sector (more details in the charts below).

Geographical Presence: In addition to a strong Danish foundation, the company has expanded into Europe. Important markets include the UK, Norway, and the Netherlands (more details in the charts below). With the acquisition of Intrasoft International in 2021, it has also expanded its operations to Greece and Belgium. With the latest SDC acquisition, it expanded to serve clients in the banking sector.

Growth Strategy: The company aims to grow both organically and through strategic acquisitions, which allow it to expand into new markets and strengthen its position in existing markets.

Today, Netcompany released its Q3 figures. Strong 22 with 20 rules (organic growth 8% and adj. EBITA 14). Clear cost synergies from SDC. In addition, a refinement/narrowing of the guidance. Revenue slightly exceeded consensus expectations, and adj. organic EBITDA exceeded consensus expectations by 6%. The markets seem to have liked the Q3 report and financial targets, as the share price is up 2.5% at the time of writing.

Summary

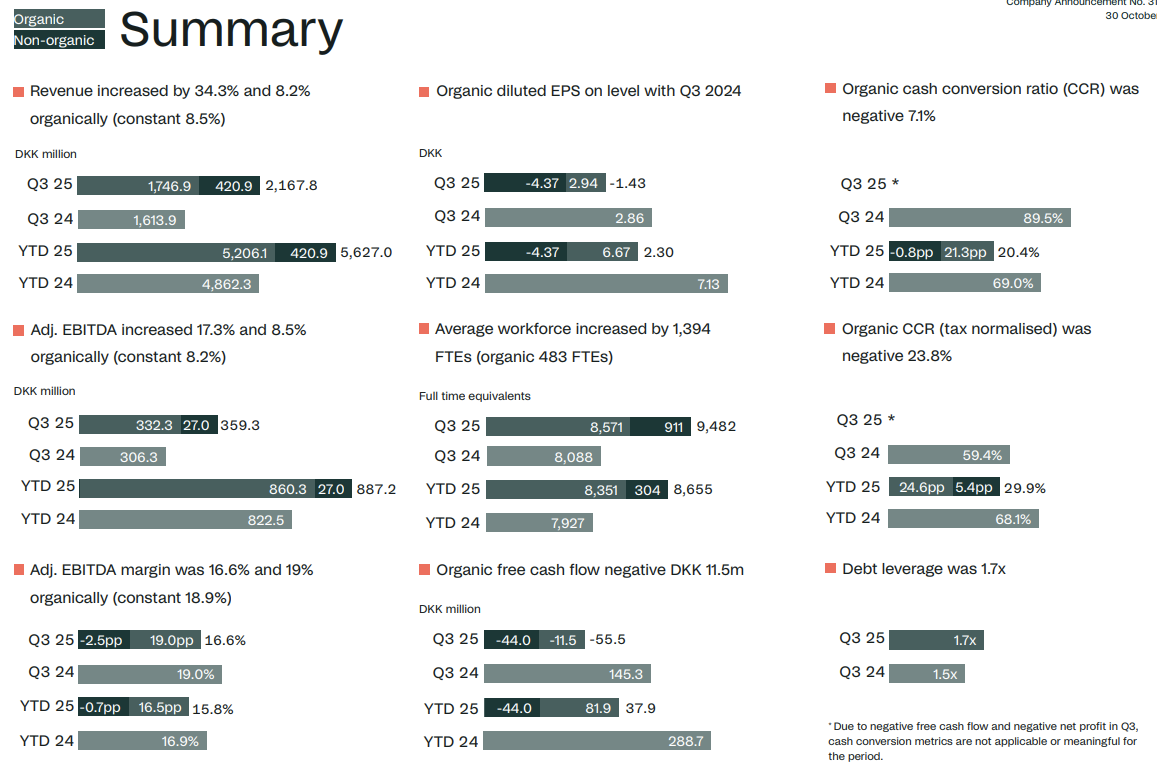

Netcompany’s organic revenue grew by 8.2% (adjusted for currency fluctuations 8.5%) to DKK 1,746.9 million in the third quarter of 2025.

Reported revenue grew by 34.3% (adjusted for currency changes 34.6%) to DKK 2,167.8 million in the quarter.

Organic adjusted EBITDA grew by 8.5% (adjusted for currency fluctuations 8.2%) to EUR 332.3 million in the third quarter of 2025, resulting in an organic adjusted EBITDA margin of 19% (adjusted for currency fluctuations 18.9%) – in line with the corresponding quarter last year.

Reported adjusted EBITDA grew by 17.3% to DKK 359.3 million in the third quarter of 2025. Netcompany Banking Services negatively impacted the adjusted EBITDA margin by 2.5 percentage points.

Over the next three years, Netcompany expects to gradually realize cost synergies, which are expected to amount to DKK 300–350 million per year by 2028, compared to SDC’s 2024 cost base.

The average full-time equivalent staff count was 9,482, of which Netcompany Banking Services accounted for 911 FTEs.

Leverage was 1.7x in Q3 2025.

Netcompany raises and narrows the lower end of its full-year financial guidance and expects organic revenue growth of 6–8% (previously 5–10%) and an organic adjusted EBITDA margin of 16–18%.

Inorganic revenue achieved through Netcompany Banking Services is expected to be DKK 840–870 million for the full year. Regarding the inorganic adjusted EBITDA margin, we expect Netcompany Banking Services to generate a result of DKK 35–40 million in 2025 (six months), as cost synergies affecting 2025 are limited.

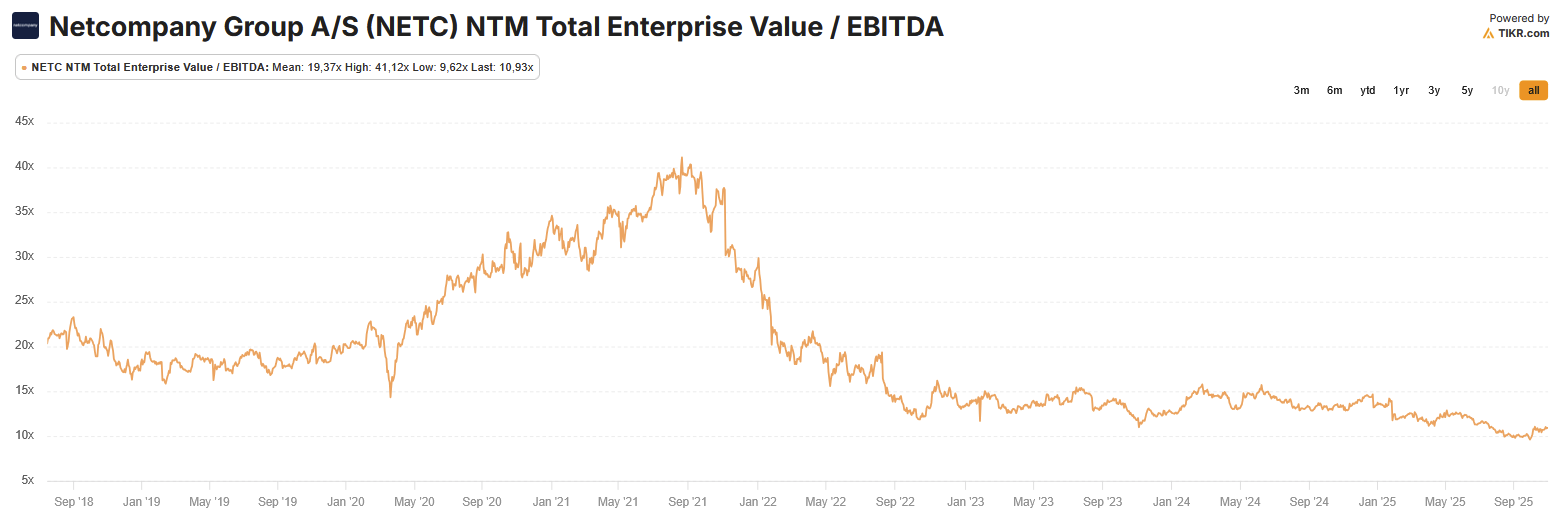

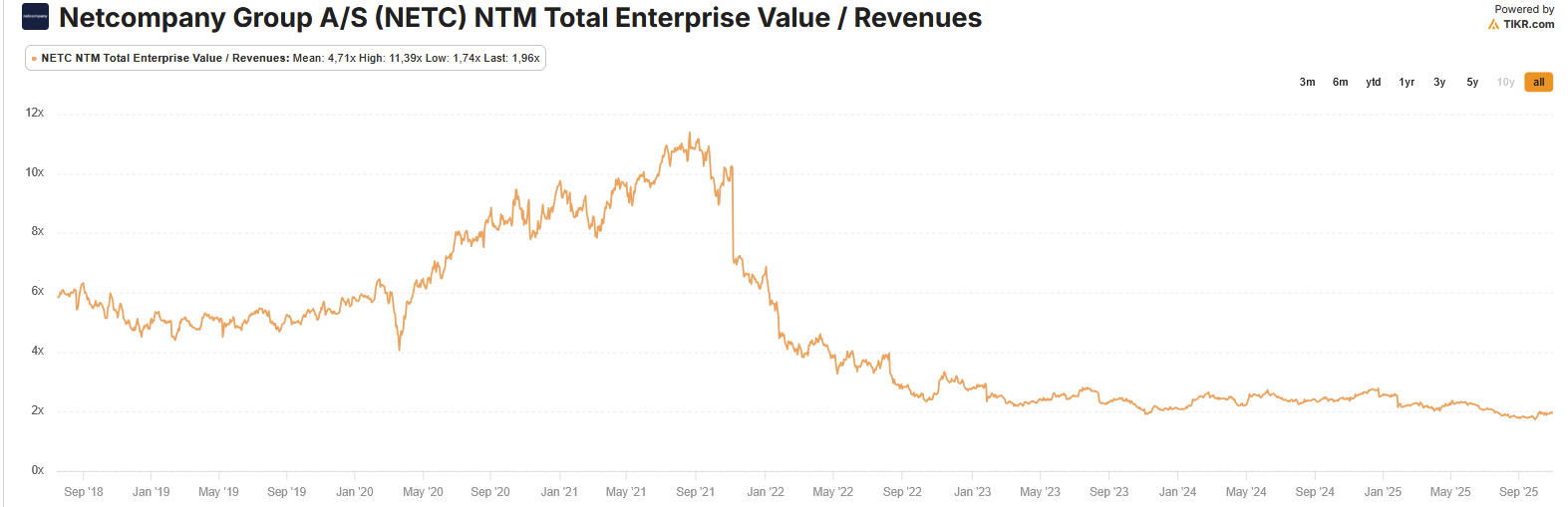

Here is also the development of the company’s valuation level (Tikr.com). Historically, the company was one of the highest-valued companies in the sector and still is, which was justified by excellent operational performance.

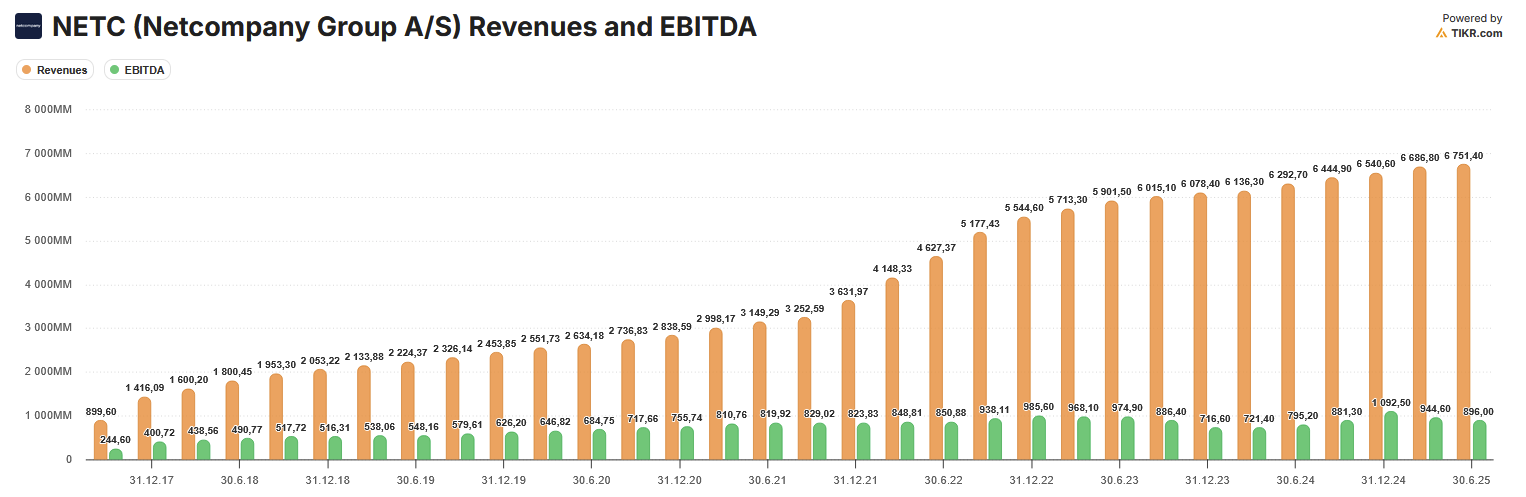

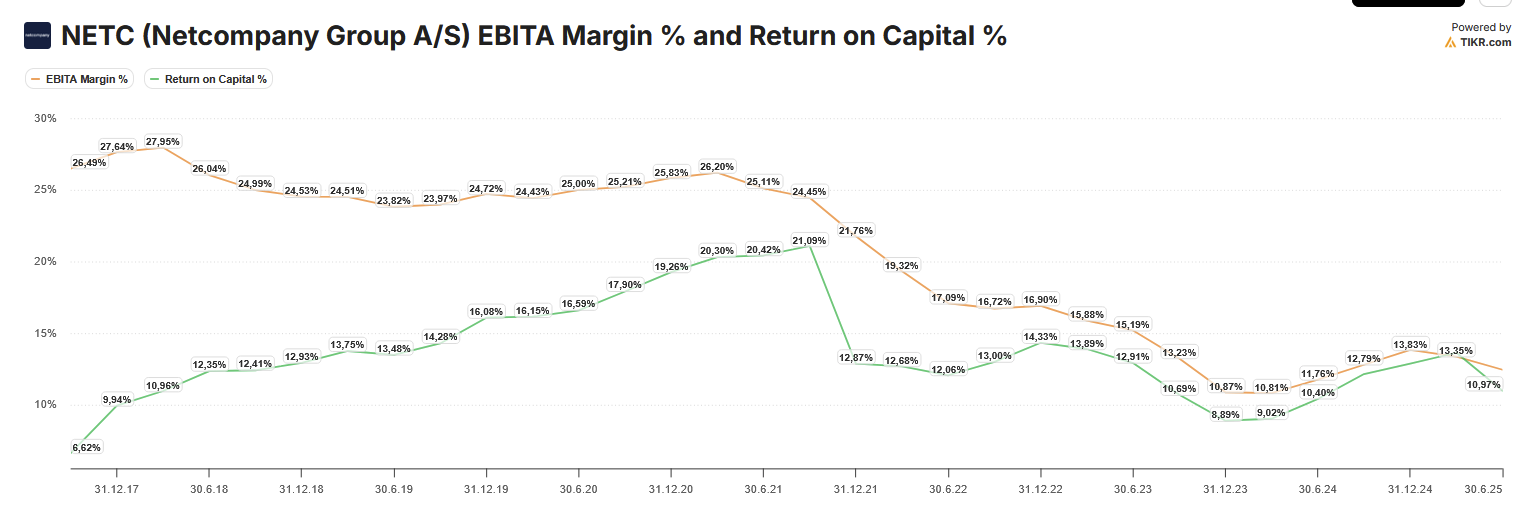

Here is also the development of the company’s key figures. As can be seen, the strong revenue growth that continued from 2021 has practically no longer translated into profit. The reason for this is that the company’s profitability level was exceptionally high and not sustainable.

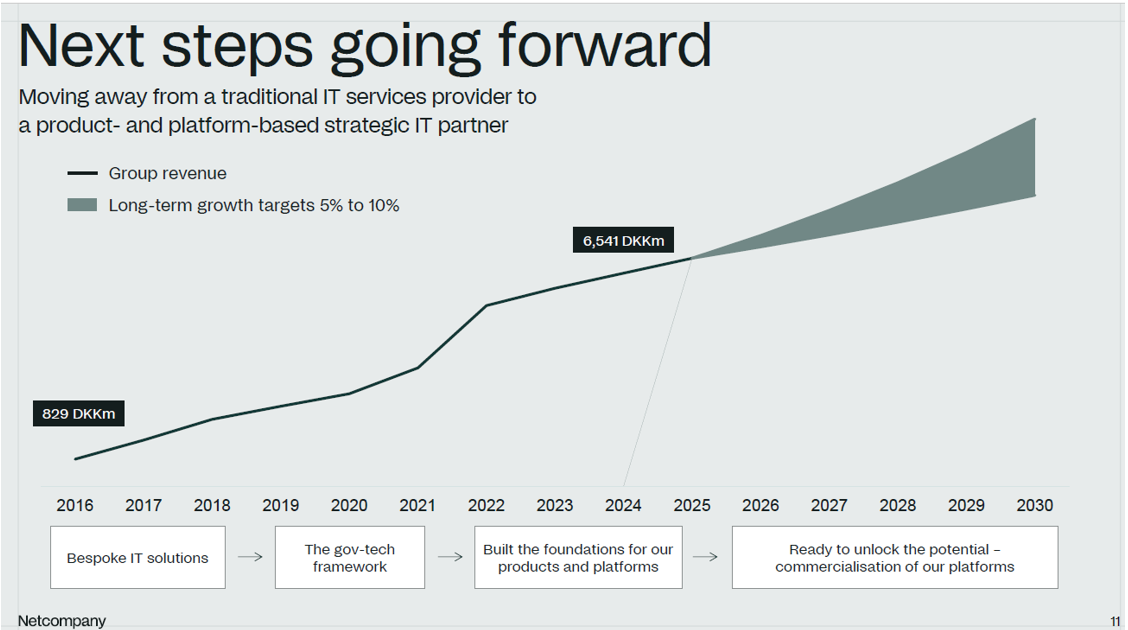

The Capital Markets Day was a bit disappointing, as concrete details after the financial targets were scarce. The previous Capital Markets Day was very fruitful. The main message now, however, is that the company is strongly transitioning from a service house to a platform and solution/product house.

The strategy now is to accelerate growth and profitability by transitioning from a pure IT service model to a hybrid model, accelerating expansion into scalable products and platforms with our related expertise.

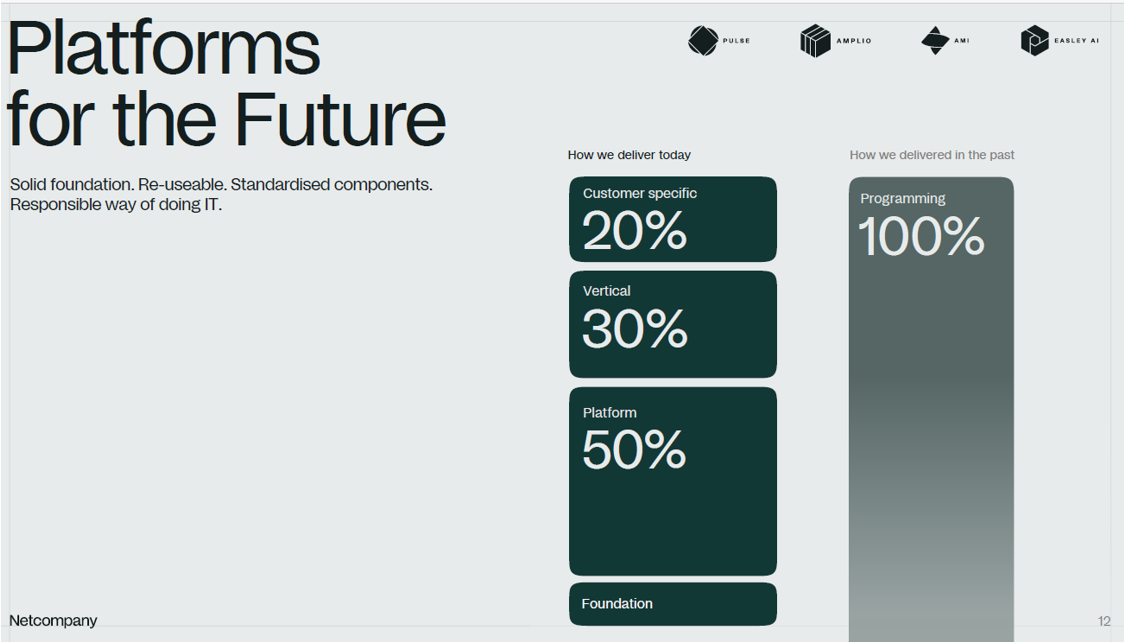

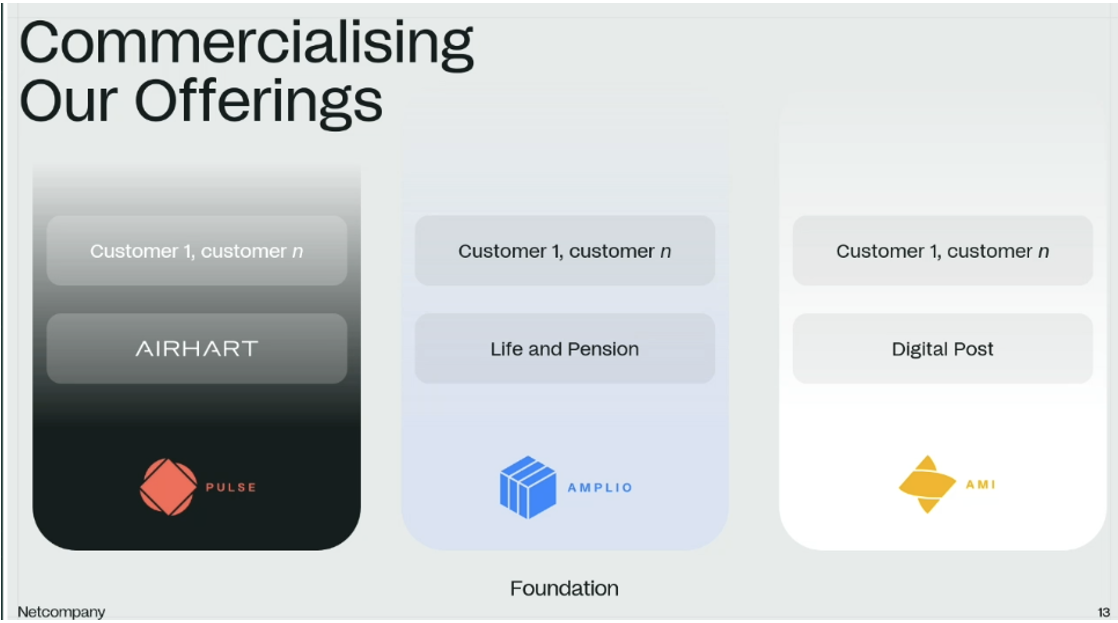

The revenue source has clearly shifted from the IT service model and is based on platforms, customer vertical solutions built on top of them, and further customer-specific customizations.

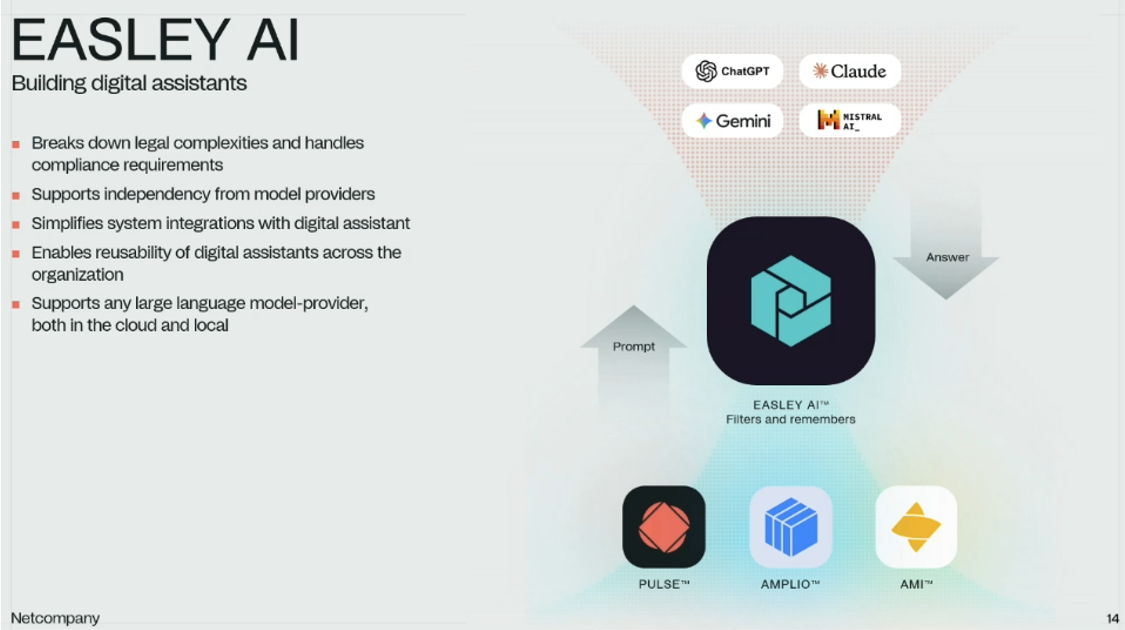

Netcompany’s platforms are Pulse, Amplio, and AMI, and these are combined with EASLEY AI. The company went through its various products, but unfortunately, concrete details remained scarce.

Regarding acquisitions, after the Intrasoft acquisition, the focus has changed, and the company will only acquire scalable IT solutions going forward. Payback target 5 years, max 7 years. Must be EPS-accretive within 2 years.

Profitability improvement will come in the medium term from SDC cost synergies and rising market margins.

I started researching this thread again after reading Joni’s review of the Nordic IT sector.

The difficult market situation throughout 2025 is reflected in the fact that in the Nordic countries, only a couple of listed IT service sector companies achieved excellent performance measured by the 20-rule. The best performance in the sector was achieved by the consistent performer Netcompany (21%), which is an excellent performance in our long-term outlook.

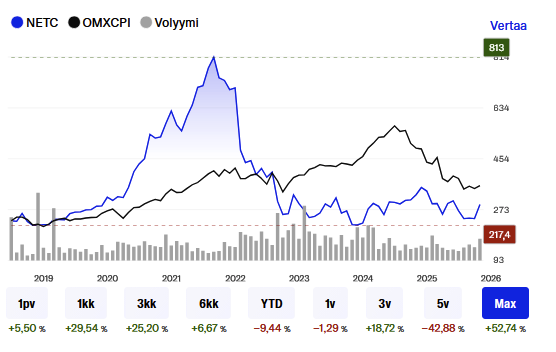

Since the beginning of the thread, the share price has risen nicely:

On March 26, the following announcement was released:

Company announcement – inside information

No. 20/2026

26 March 2026

Netcompany raises full-year margin guidance for 2026

Netcompany’s continued focus on delivery excellence and implementation, supported by the ongoing embedding of AI capabilities into our methodology has led to increased expectation for adjusted EBITDA margin for the full-year 2026.

“As a leading European provider of complex IT solutions in regulated environments across public and private sectors, we constantly strive to become better at what we do.

The continuous investment over recent years in AI-embedded platforms and products and responsible AI executable methodology has positioned Netcompany as a European leader in delivering and/or renovating highly complex high-quality systems on time and within budget with reduced risk.

We are closely monitoring progress in these areas and finalising the first quarter of 2026 with a promising outlook. Based on current initiatives we see significant potential for accelerated and ongoing improvements as further initiatives are introduced throughout the Group.”

André Rogaczewski,

Netcompany CEO and Co-founder

For the full-year 2026, Netcompany now expects an adjusted EBITDA margin excluding Netcompany Banking Services (NBS) between 17% and 20% (previously between 16% and 19%). This implies an adjusted EBITDA margin including NBS between approximately 16% and 19% (previously between 15% and 18%).

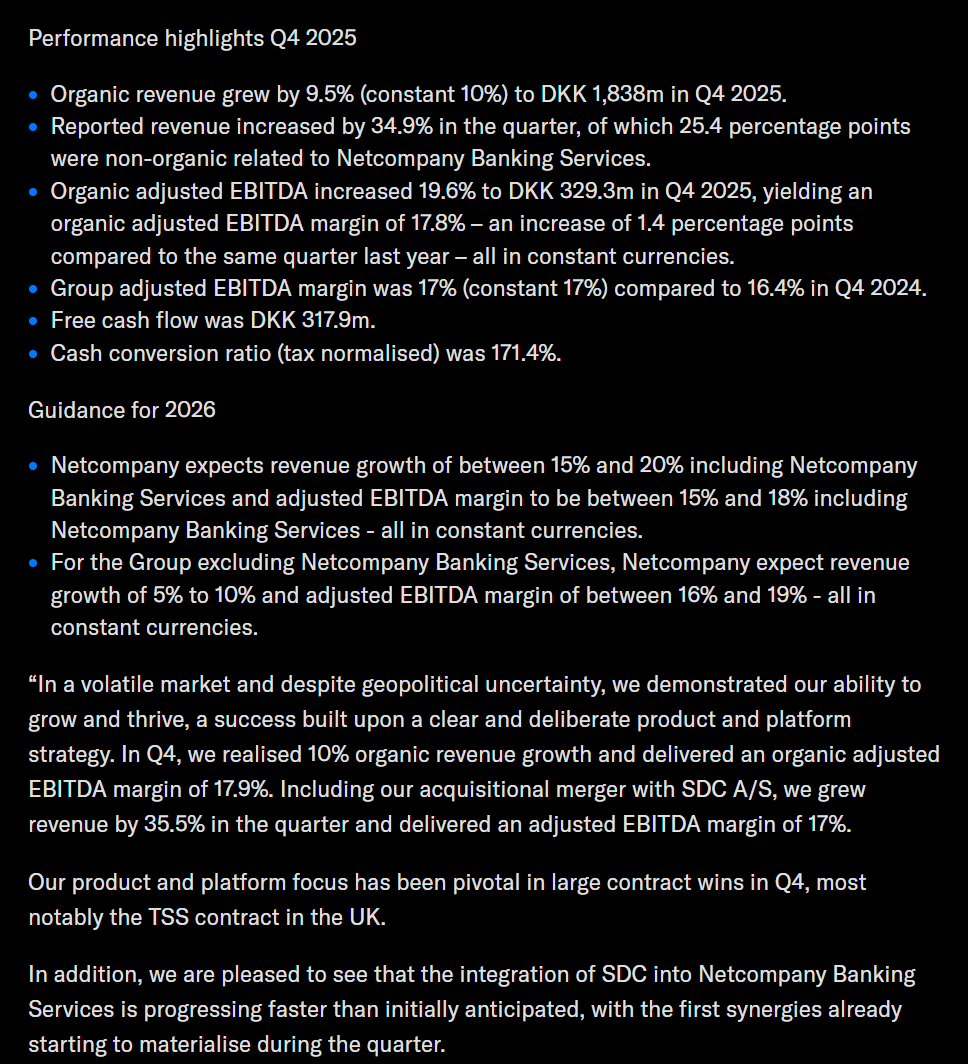

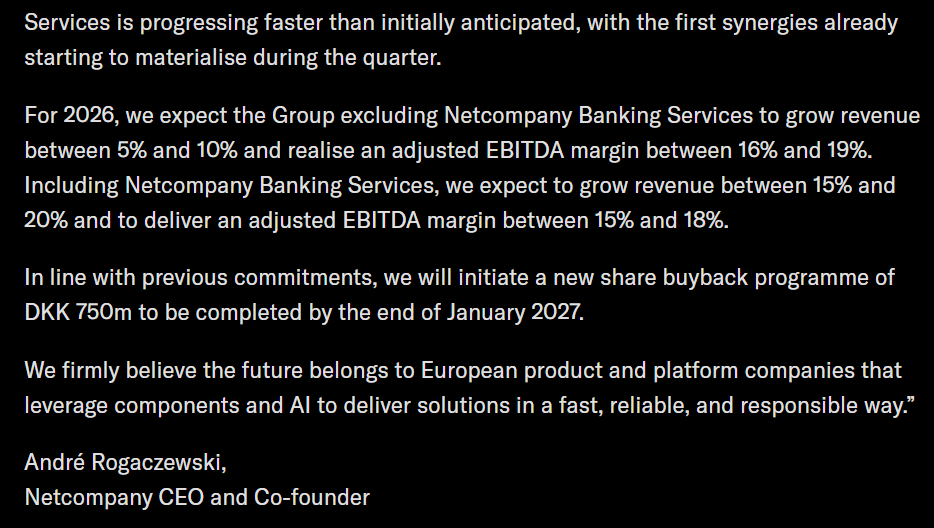

Then here’s a little Q4 report (after which the positive announcement above came out)

I’m trying to activate discussion with these “highlights” and so on.

From the analyses and articles I’ve read, Netcompany seems quite impressive and uniquely distinguished, for example, it has strong expertise especially in public sector digital transformation, and apparently its own products and platforms support this well.

The company gives the impression of being agile, even though it’s not a small firm, and at the same time it has the resources of a large stable company, which seems to be in a good position to benefit from new trends in the industry, if I can trust the texts I’ve read.

It’s almost half a year since Frans’s message below, and the share price has fluctuated (a lot), but it mentions valuations. It’s a highly valued company for a reason, but I don’t know if it’s already too expensive after the most recent surges.