q.beyond (ticker: QBY.DE) is a German IT services company that primarily serves medium-sized enterprises. The company’s business involves helping customers with cloud service solutions, system maintenance, cybersecurity solutions, and building new AI and data solutions:

1. Business Areas:

- Managed Services

The company maintains customers’ IT infrastructure: cloud servers, networks, workstations, and cybersecurity.

- Cloud and Data Centers

The company has one proprietary data center in Hamburg and one leased in Ulm. The company can offer customers local data center services.

- SAP and Microsoft Services

The company assists customers in the implementation and maintenance of SAP systems, Microsoft 365, Azure solutions, and other business software. This is traditional IT consulting.

- AI and Data

q.beyond is trying to grow its business through AI. The idea is to offer AI solutions to companies, especially when customers do not want to move all their data to large American cloud companies.

2. Financial Figures:

In 2025, the company generated revenue of 182.6 MEUR and EBITDA was 12.3 MEUR (6.7% margin). EBIT, accordingly, was slightly positive for the first time in three years at 1.9 MEUR:

The company has a very strong balance sheet, with no debt and cash reserves of 42 MEUR:

3. Valuation

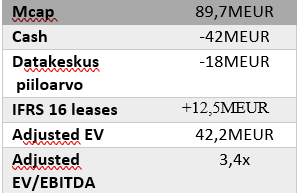

The company’s market capitalization at the time of writing is €3.6 * 24,915,896 = 89.7 MEUR. The company holds cash equivalent to 47% of its market cap, meaning the enterprise value (EV) is 47.7 MEUR. The company’s EV/EBITDA multiple is 3.9x. The company is effectively discounted by over 40% relative to other German IT service peers, even though the balance sheet is debt-free and the company has turned profitable. Peers such as Bechtle (9x), Cancom (8x), and Tieto (8x EV/EBITDA) can be used as comparables.

What makes the valuation interesting is that the book value of the Hamburg data center is 14.5 MEUR. I personally estimate the fair value to be closer to the 30-40 MEUR range. If the fair value is adjusted on the balance sheet, the P/B ratio drops to the ~0.8x range, meaning the company can be bought below its book value.

In practice, when the fair value of the Hamburg data center is included in the calculations, the adjusted EV/EBITDA multiple becomes 3.4x:

Cornerstones of the valuation:

-

Debt-free balance sheet, 42 MEUR in cash.

-

Hidden value of 15-25 MEUR in the Hamburg data center. As a point of comparison, the company’s previous data center sales from 2021 yielded 44 MEUR for two data centers.

-

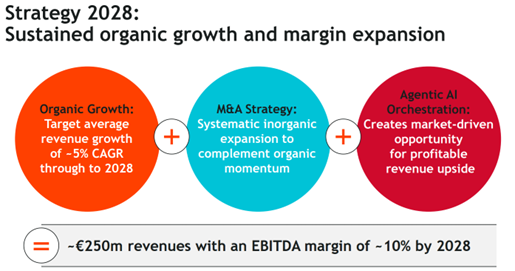

The company just released a new 2028 strategy aiming to grow revenue from 182 MEUR → 250 MEUR with a 10% EBITDA margin:

4. Target Price Scenarios:

I have modeled the company’s target price for the H1/2028 period through the scenario matrix below:

In the Bull scenario, I assume that the company achieves its 2028 strategic targets and succeeds in accumulating free cash flow of 5-10 M€/year. This would require the YoY growth of the Consulting business area to continue (>10%) and the company to announce a share buyback program during H2/26. At the same time, the assumption is that the hidden value of the Hamburg data center would be reflected in the valuation.

The company’s free float is only about 75%, so a 5-10 MEUR buyback program would already create significant buying pressure on the share price.

It remains to be seen how the company’s story develops, but I find the valuation and risk/reward attractive at the moment.

Disclaimer: I am a shareholder in the company.