Pharmaceutical development company Nanoform Finland is considering a dual listing on the First North Premier market in both Finland and Sweden. Founded in 2015, the company aims to reduce drug particles, thereby giving them more potency.

Revenue 2019: 0.05 million euros

Operating profit 2019: -7.3 million euros

Number of employees: 50

Nanoform’s key strengths

The Company believes that Nanoform’s key strengths are:

operates in a multi-billion-dollar global pharma market

possesses a patent protected technology with the potential to facilitate a paradigm shift in the global pharma industry, by addressing the key issue of low bioavailability

possesses a cost-efficient technology that enables sustainable and scalable supply for customers

has a business model that is expected to be highly cash-generative with strong potential for recurring revenues

has a seasoned management team with an excellent combination of competences, supported by a highly qualified Board of Directors

has strong momentum with significant opportunities ahead

Nanoform’s expected near-term business targets

start of first GMP project before year end 2020

win more new customers in 2020 than in 2019

first clinical trial and dosing in humans in 2021

Nanoform’s 2025 business targets include among others

process at least 50 new APIs per year

have 25 production lines of which 5-10 are GMP compliant

I’ll have to follow this thread, I’m already involved with three other pharmaceutical companies, so this one interests me too.

Let me know when you have information.

From Google Scholar, an article from 2016 on CESS technology was found using the search term “Controlled Expansion of Supercritical Solutions”. There’s also a lot of material when searching with the names Häeggström and Yliruusi. It’s harder to say how much of the results are relevant to Nanoform, though.

Nanoform is organizing a web presentation on Tuesday, May 26, 2020, at 5:00 p.m. One could imagine that this is aimed at building up suitable buzz as the stock market listing approaches.

"20,289,856 new shares in the Company to be subscribed for.

The fixed subscription price for the share issue is 3.45 euros per share, which preliminarily corresponds to approximately 36.42 Swedish kronor per share.[1]

The Company’s market value is approximately 230 million euros, assuming that the maximum number of new shares are offered and subscribed for in the IPO."

That value feels quite high; what worries me most is if human medical trials haven’t started yet? Does anyone have other information about this?

Nanoform’s expected near-term business targets

start of first GMP project before year end 2020

win more new customers in 2020 than in 2019

first clinical trial and dosing in humans in 2021

Edit: From a Talouselämä interview:

“The goal is to increase the number of our production lines from the current seven to 25 by 2025 and to get Fimea approval for clinical drug development for 5–10 of them. Then we can process about 50 new drug substances every year. When the lines are up and running and there are many projects underway, our goal is to become cash flow positive by 2025. That’s why we want to raise enough capital at once to achieve that,” says Nanoform’s CFO Albert Hæggström.

Yes, it seems we’ll have to wait a few years for cash flow positivity. It’s smart to acquire enough capital all at once so there aren’t issues every year, but it makes pricing the company challenging. It would be easier to seek money in later rounds at better valuation levels if things have progressed as expected.

Really interesting kiosk, but valuation is indeed challenging. And I wonder, why the stock market specifically, if it’s still years before things get going.

Revenue 50,000e and offering price 3.45e per share. Doesn’t sound appealing to me, especially considering Revenio’s market value of 198 M€ in 2016 (Nanoform also aims for a 230 M€ market value in the offering). The technology itself seems quite solid, but I don’t think 25 production lines will make the cash flow match the current valuation.

If Nanoform succeeds in what it promises, the company will still cost a lot compared to the outlook for 2025. Note, IF it succeeds. Their technology has only been proven with Piroxicam, which dissolves very well in liquid carbon dioxide (which is quite hydrophobic) and thus serves as an excellent case study from Nanoform’s perspective.

Almost all organic drug molecules don’t do this. Just as hydrophobic Piroxicam clumps in a polar solvent like water, polar or hydrophilic drug substances (like e.g. paracetamol Paracetamol in Older People: Towards Evidence-Based Dosing? | Drugs & Aging | Springer Nature Link) clump in a hydrophobic solvent like liquid CO2. This alone significantly limits the scalability of the technology for many different drug substances.

On the other hand, as offerings have always been fully subscribed in recent years and the stock price usually skyrockets from the opening, participating in Nanoform’s offering might be a smart move. Investing is not always a rational game that takes the whole picture into account. Especially during IPOs.

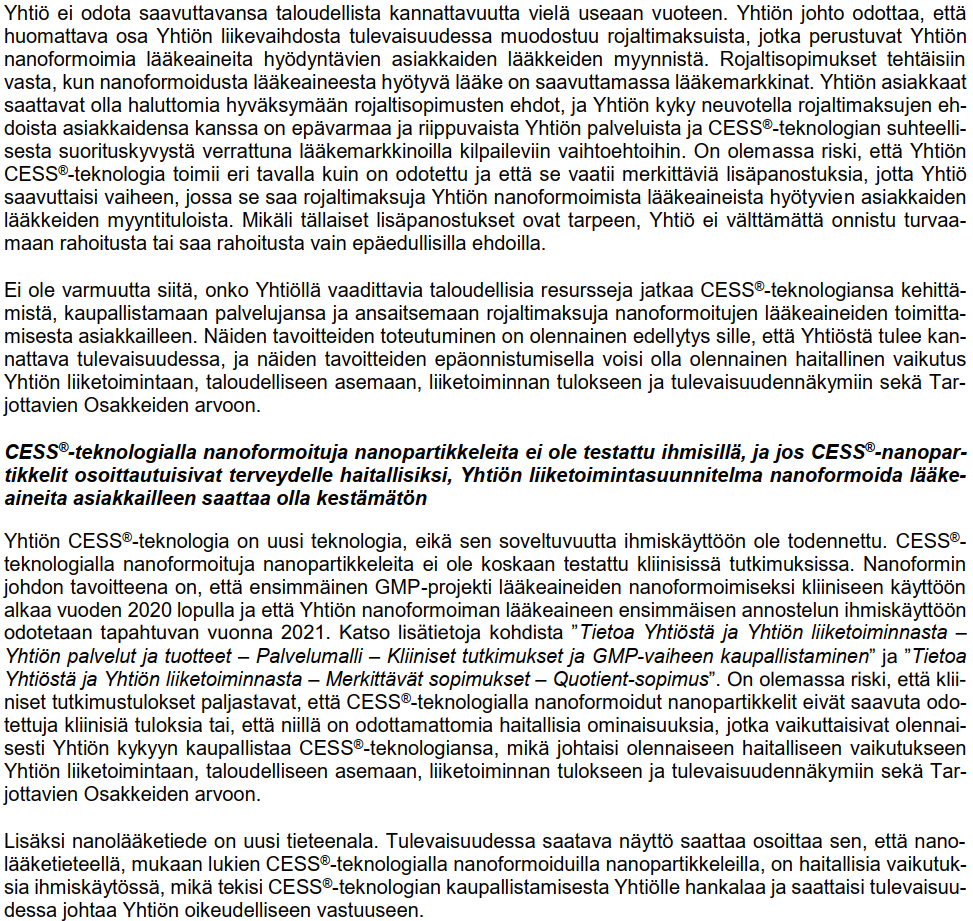

The above passage from the IPO prospectus tells why I won’t participate in the offering with this information. The company’s technology may not work, and even if it does, no money will be coming in for years. I’ll have to reconsider when the first couple of additional offerings have been made, the company’s product has been proven to work, and some money is in sight

You’re right, I accidentally looked at the 2016 market value. I’ll correct my previous post

If we look at the 2016 results, Revenio’s revenue was €23.4 million and operating profit was €7.1 million. So the same idea still applies when comparing it with Nanoform.

The Company and the Sellers anticipate paying a total of approximately EUR 13.8 million in fees and expenses incurred in connection with the IPO. Of the total amount, approximately EUR 8.8 million would be paid to the Organizers, and approximately EUR 3.7 million to the Company’s two Key Employees.

The goal of the IPO is to raise ~70 million euros in new equity for the company. However, ~20% of that will be immediately shaved off as “fees and expenses”.

A particularly dazzling return on equity is not to be expected immediately. The required rate of return will be quite high.

I haven’t looked into it in depth, but for example, a listing by some fellow finance company seemed to be around a million, and generally, that’s a more realistic range for these kinds of things than almost 14 million

Does this listing now cost 13.7 million or 12.5 million? Both figures can be found on page 32. The company is raising 70 million and estimates net proceeds of 57.5 million. On the same page, fees and expenses are estimated to be 13.7 million. Then, in the capital structure on page 33, the company’s liquid assets increase by 57.6 million. What happened to that 1.2 million?