Aiforia Technologies announced its intention to list on First North and raise EUR 30 million.

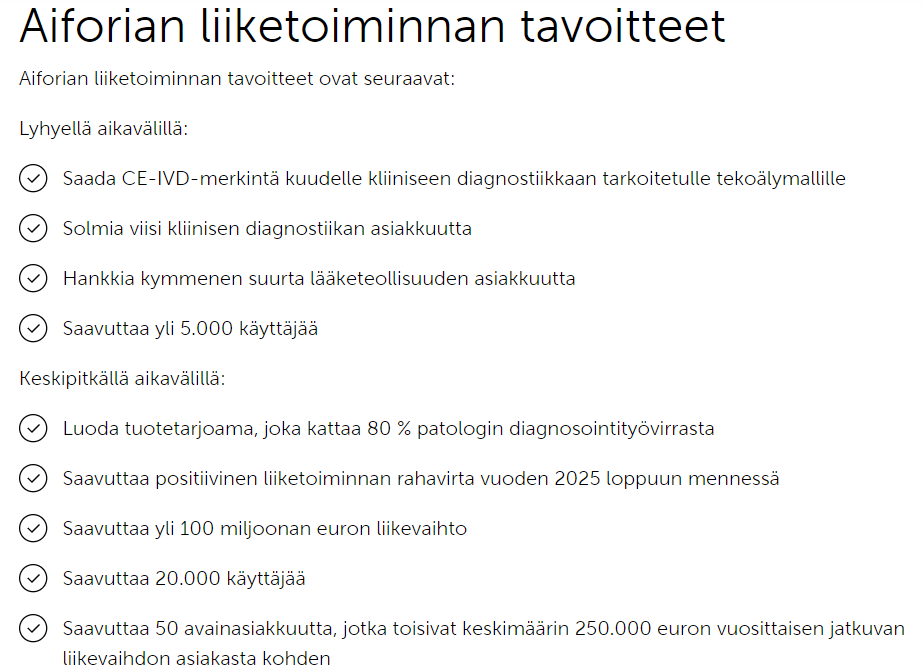

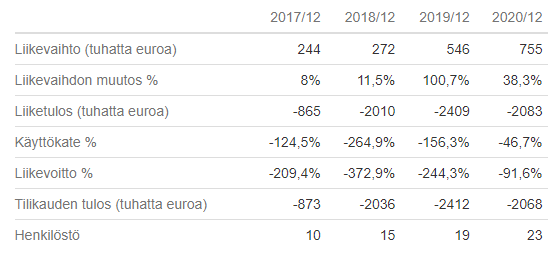

They are ambitiously targeting EUR 100 million in revenue, but so far, they seem to be operating at less than a million. They modestly omitted historical figures from the press release.

Well, this sounds interesting, but of course, the business case is another matter. So, it’s time to start dissecting it on the forum!

Aiforia aims to be a leading global player in AI-assisted tissue sample analytics. It seeks to provide AI solutions that improve the accuracy, efficiency, and repeatability of tissue sample analysis, enabling faster, better, and more personalized care for patients. The patient benefits can come through more accurate and efficient diagnostics, as well as through enhanced drug development and medical research.

The gross proceeds from the share issue are estimated to be at least approximately EUR 30 million and are intended to support Aiforia’s growth strategy through investments in sales and marketing, research and development, and other operational purposes.

https://www.finder.fi/Tukkuliike/Aiforia+Technologies+Oyj/Helsinki/yhteystiedot/2781000