I listened to that webcast yesterday. I’ll share my thoughts over the weekend. According to the CEO, the cash burn estimate for this year (approx. -€10M) does not include milestone payments. Management likely doesn’t want to forecast them for this year as their timing is probably uncertain, but if they do materialize, the results should primarily shift upwards. The submission of the marketing authorization application for nanoenzalutamide is still expected to happen this year. If it gets delayed, the company’s financing situation will indeed become more difficult. However, at the current cash burn rate, the cash runway should last for another two years. I would assume that the milestone payments for nanoenzalutamide are also tied to obtaining that marketing authorization.

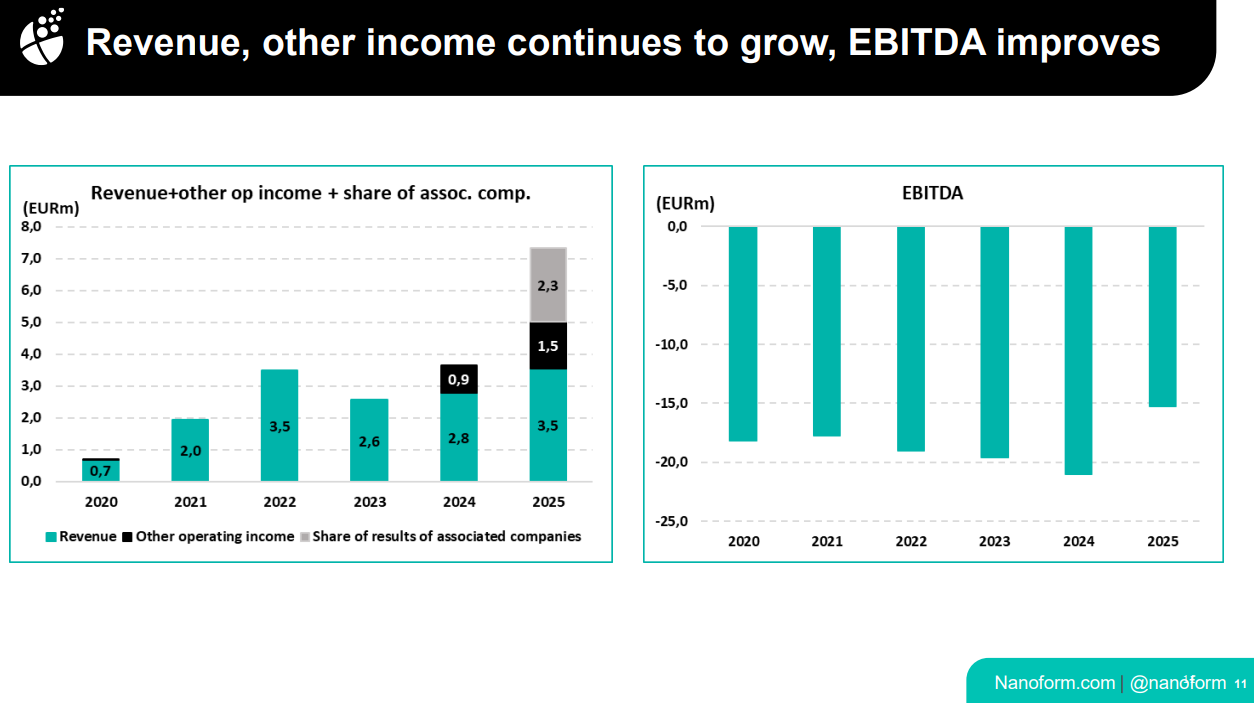

The income from associated companies (gray bar) likely comes from BRAFmed’s signing fees. According to management, these are in the low single-digit million range, which would fit that figure. The black bars likely relate mostly to nanoenzalutamide, of which Nanoform owns 25%.