I’m really no quantum expert; I only took the mandatory physics courses in high school… But as I understand it, that Microsoft chip is a so-called superconducting qubit, where the qubit is created by cooling superconducting material to a very low temperature. Another common method is “trapped ion”, which Ion Q, for example, uses, and this is where lasers are fired.

However, quickly reading Microsoft’s announcement, it talks about how the state of their qubits is measured, and it mentions the use of microwaves. I don’t know Modulight’s devices at all, and even if I did, I probably wouldn’t understand anything about them, but some microwave lasers apparently exist. Whether Modulight has them, I don’t know.

Modulight states on its website about the use of lasers in ion trapping. Based on that, the customer could well be IonQ or Quantinuum, both of which are US companies.

I suspect it’s Quantinuum, because Modulight tagged Quantinuum on Twitter in 2023.

"A week before the release of the 7-qubit computer, physicist David Wineland and his colleagues from (NIST) reported creating a 4-qubit quantum computer by entangling four ionized beryllium atoms in an electromagnetic ‘trap’. After the ions were trapped in a linear arrangement, a laser beam cooled the particles close to absolute zero and synchronized their spin states. Finally, the particles were entangled with a laser, creating a superposition of ‘spin up’ and ‘spin down’ states simultaneously for all four ions. Again, this demonstrated the basic principles of quantum computers, but scaling this technique to practical dimensions is also problematic.”

Antti and Tommi discussed Modulight, is it time for the company to see the light?

After difficult years, cautious glimpses of improvement can be seen in Modulight’s development, as the company has gained more reference customers and grown its order book. Risks remain high, but the stock finally appears cautiously attractive. Analyst Antti Siltanen discusses Modulight’s stock market journey and future outlook.

Topics:

00:00 Start

00:19 Difficult start to the stock market journey

04:06 Small signals of improvement at the end of the year

05:53 Order from a leading quantum computing company

07:30 Strong growth in forecasts

08:59 Stock valuation cautiously attractive

Siltanen has written his preliminary comments, as Modulight will publish its Q1 results on Friday.

The company reported in its previous Q4 report on a growing order book and an increase in the number of hospitals using its products. Based on this message, we expect growing revenue for the quarter. However, our growth expectations are still at a moderate level due to the early development phase of the projects. Earnings are slightly weakening in our forecast due to increasing depreciation. We do not otherwise expect operating costs to have increased. The weakened operating environment and the dollar in the United States negatively affect the company, but at this stage, the key is the company’s ability to grow revenue and make progress in achieving a turnaround in results.

Quite a lot needs to happen, of course, for EBIT to be positive in Q4. Based on the call, perhaps about a quarter of the revenue was left unrealized in Q1 due to delays… Orsila, in my opinion, emphasized continuous growth from one quarter to the next. If, for example, Q4 revenue is 3.5 million, would that be enough to turn a profit…? But there is some indication of improvement here.

Siltanen has completed a fresh company report today after the Q1 report.

Modulight’s Q1 continued on the positive path outlined by the financial statements. Revenue exceeded our expectations, and the loss was smaller than forecast due to a decrease in costs. Visibility into the company’s business has improved, although it is still at a low level. We are moderately raising our forecasts as a result of the good development. We reiterate our recommendation (add) and raise the target price to 1.5 euros (previously 1.3) in line with the forecast upgrades.

OP’s Kaj Stenvall shared his thoughts on Modulight’s Q1.

Modulight published its Q1/2025 results. The company’s revenue grew well during the quarter compared to the previous quarter. However, the operating profit (EBITDA) was at a loss (-0.6 million euros), although the loss was smaller than our forecast (-1.1 million euros). Senior Analyst Kimmo Stenvall elaborates in the video on the company’s first quarter of the year, the challenges it faces, and its long-term potential.

Antti has published a new comprehensive report on Modulight, and like other comprehensive reports, it is available for everyone to read.

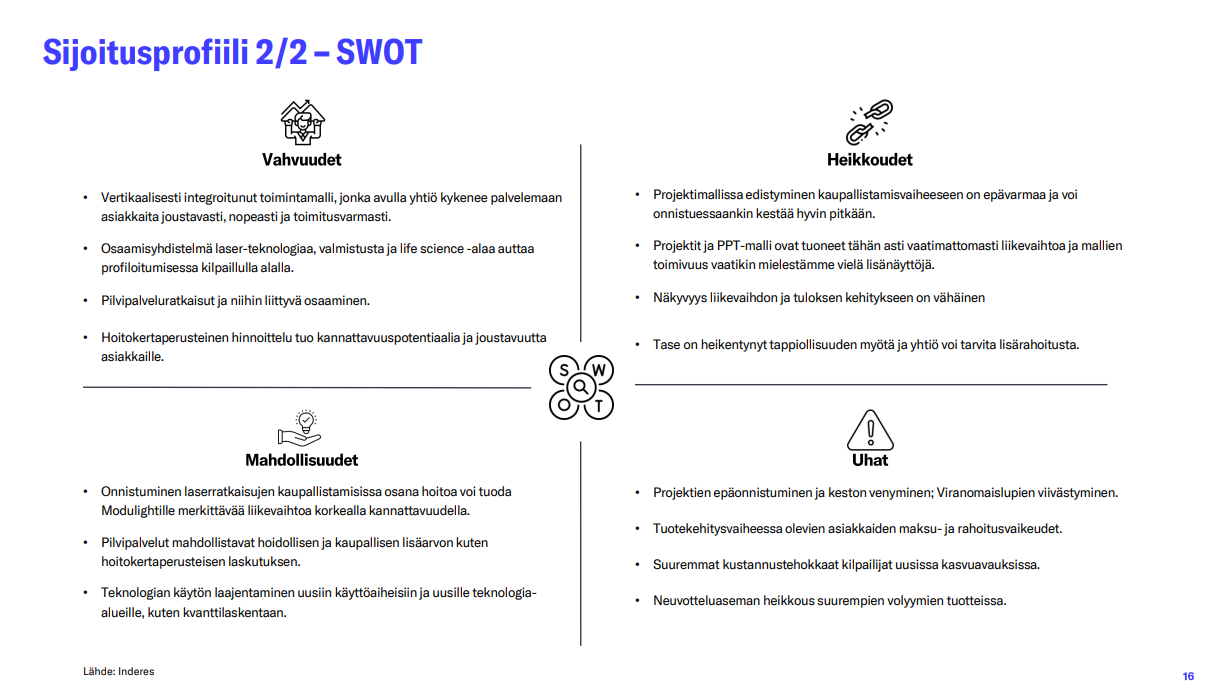

Modulight is a technology company focused on the design and manufacture of lasers and optics, with a strategic emphasis on medical and biomedical applications. The company aims to return to a path of profitable growth after difficult years following its listing. Recent reports have shown preliminary signs of improvement, although the turnaround involves considerable uncertainty. Our valuation, based on revenue multiples and cash flows, suggests a moderate undervaluation of the stock. We reiterate our “add” recommendation and a target price of 1.5 euros.

In summary, we believe that Modulight’s growth and profitability involve both great potential and significant uncertainties, which we aim to balance in our valuation. Uncertainties and poor predictability have been concretely reflected in the market’s highly volatile pricing and accepted multiples since the listing (the stock’s listing price was 6.49 euros and the subsequent range was 0.77-17.65 euros/share).

Iikka and Antti discussed Modulight regarding a comprehensive report.

Modulight’s business development has been slow, but the previous quarters give hope for better times. Opportunities outweigh risks, so we remain on the ‘add’ side. Analyst Antti Siltanen comments on the company.

Topics:

00:00 Introduction

00:15 Modulight

01:41 Transition to PPT model

03:39 Markets

09:31 Strategy

10:54 Company’s investment story so far

13:35 Revenue development

15:42 Earnings forecasts

17:19 Valuation

Thanks for the comprehensive analyses! The discussion about Modulight has quieted down, so it’s nice to hear Siltanen’s thoughts.

What would interest me is how much potential Modulight sees in the quantum sector. For example, what kind of competition is there among high-level laser suppliers? Market size?

Although the company did not reveal to whom the €0.8m piloting order would be delivered, many speculated it was Quantinuum, whose valuation is somewhere between 5-10 billion dollars. So, is there potential in this sector?