The company seems interesting in all aspects, even if I don’t understand much about the technology. Does anyone have information about the company’s target market and its size?

KL:

The goal is to move forward with three customers for broad commercial product implementation in 2023. If this materializes, the company’s revenue will multiply.

According to the company, broad commercial implementation means that the revenue for that particular customer or product exceeds ten million euros.

There’s a bit of room for interpretation here, and one should approach these back-of-the-napkin calculations with caution, but if:

- revenue were to rise to €30-40 million in 2023

- the company could achieve ~€16-20 million EBIT, depending, of course, on growth prospects and investments

- with a valuation of €205 million, EV would be ~€150 million, and roughly 2023 EV/EBIT 7.5x - 9x

Of course, in this scenario, everything probably goes perfectly. There’s no information on how this company guides (overly conservative like Qt or otherwise).

33 Likes

It’s probably not directly comparable, but Revenio’s 2023 EV/EBIT is 35x with a 35% margin. Qt’s 2023 EV/EBIT is 42x.

If this company were to rise 50% at opening to a valuation of about €300m, then by back-of-the-envelope calculations, you could still get it at a 12.5-15x multiple.

I think that:

A) The company will be bought out before the IPO.

B) Retail investors will be able to get in at opening, maybe at that +50% level?

Someone please correct me if I’ve calculated something wrong ![]()

34 Likes

Was 205 pre-money or post-money?

2 Likes

Great, Timontti, that you found this company too! This only further strengthens my belief that we small investors won’t get more than a few scattered shares of this gem from the IPO ![]()

I would think that the company would have already been sold if its current owners had such intentions. Surely, this listing is the result of long consideration, so a really good takeover bid would probably be needed for them to accept it in this situation. Modulight must have had interested buyer candidates even before these IPO plans. In my opinion, it would be strange to cancel the IPO at this stage (though not entirely unheard of).

11 Likes

The condition for the institutions seemed to be €205m before the share issue, so there will be an impact…?

I can’t say for sure, but I assume the EV is then 205 million euros.

1 Like

How does one get involved in this as an institutional investor? ![]()

I couldn’t find any information about this in the listing announcement.

8 Likes

This is indeed a lot of salesman’s embellishment. If one reads the research on the company’s website on the topic, there is no such conclusion, nor was it even studied in that particular research setup. Proper studies have not really been done, but at least one previous clinical study has found that there is ultimately no difference in survival between those who received laser (so-called photodynamic therapy) on the tumor and the control group: mortality was ultimately the same. For glioblastoma, it is an experimental treatment and studies are ongoing. At least one clinical trial appears to be planned, with an estimated completion date of 2026.

It’s quite a stretch to claim that our laser cures up to 40% of glioblastomas, when the reality is that all patients eventually die within a couple of years of surgery. One should not believe everything CEOs say.

73 Likes

Here are a few things about the company that I came across today while looking for information. Some excerpts from them:

June 2, 2021:

https://lehti.tek.fi/tyoelama/tamperelaisten-tarkka-laser-ase-syopaa-vastaan

When financial news agency Bloomberg wrote about Modulight in October 2020, Orsila rubbed his eyes in disbelief: word of the Tampere-based startup had reached as far as New York.

– I can’t think of a single big technology company in Silicon Valley that isn’t one of our customers or hasn’t shown interest in us in one way or another.

Almost all of Modulight’s technical employees have been in the operating room to get a feel for how the usability of lasers needs to be improved.

– We want to offer our customers an easy-to-use device that doesn’t require two doctors of technology to operate. Many of the best cancer hospitals in the United States and Europe have our lasers.

According to Orsila, Modulight’s lasers can treat patients who would not survive traditional cancer treatments. When the optical fiber is guided directly into, for example, the patient’s brain and tumor, the surgeon does not have to cut out large pieces.

Focusing on health technology and especially cancer treatments was a conscious decision. In 2014, Orsila and his colleagues set up a laser factory, but soon realized that it would not be profitable if they only manufactured lasers for cancer treatment. Also, the employees’ skills would not stay sharp if they got to build lasers too infrequently.

– We wanted our own factory. Many buy lasers elsewhere and develop their products from them, but that’s like putting a tractor gearbox in a sports car. Thanks to our own factory, we can guarantee our customers continuity: our lasers will still be available decades from now.

According to Orsila, Modulight needed more products for its portfolio: something that is close enough to health technology, but for which the customer is willing to pay good compensation. Today, Modulight also develops lasers, optics, and their cloud services for genetics, ophthalmology, and the automotive and satellite industries.

Orsila also made a tactical choice to market Modulight’s products only to the United States and large companies.

– Through that, opportunities and deliveries have sprung up all over the world.

Modulight’s newest customers include printer manufacturer Hewlett Packard and Japanese Olympus.

Now Orsila is at a point where Modulight has been doing well enough for long enough, and he can take his foot off the investment brake.

– Last year, we acquired a five-million MOCVD (Metal-Organic Chemical Vapor Deposition) reactor from Germany, with which we can form laser structures. It is the stacking of different semiconductor layers on top of each other with almost atomic layer precision. In addition, a high-quality electron microscope from Japan will soon arrive. We are also investing 23 million euros in expanding our factory.

The pandemic has not slowed down the pace.

– Last spring, we gained many large customers.

The article also states that employees own 90% of the company and 10% is owned by other private individuals.

Article April 26, 2021:

Modulight manufactures lasers for special applications. Founded in 2000, the company spent the first 14 years extensively experimenting with different application areas for lasers, including space and defense technologies. There were customers from several different countries, but the company did not achieve profitable growth. About seven years ago, the company decided to focus on a narrower sector of the market, namely cancer treatment, genetics, and special applications requiring the same laser technology, and to focus its efforts only on the US market and large corporations.

Today, Modulight has several of the world’s largest companies as customers. Marketing and sales activities are still directed to the USA, although currently Asian exports are growing fastest - investments in the USA have also radiated business elsewhere. The work aimed at becoming a strategic partner for large corporations has begun to bear fruit: “Last year, we started more new long-term customer projects with Fortune 500 companies than ever before,” Seppo says.

Modulight’s sustainable growth has also been built on a strong technology focus. The company only undertakes projects for customers that result in products manufactured in Tampere. In addition, the policy is that IPR (Intellectual Property Rights) remains with Modulight and the devices are connected to the company’s own cloud and manufactured in Finland.

November 16, 2020:

Marketing and sales activities are still fully directed to the USA, and this radiates business all over the world. Currently, Asian exports are growing fastest. Surprisingly, our customers’ business in the USA has not really slowed down due to the corona pandemic. I expected that there would be no new initiatives, in particular, but I was wrong. This year, we have started more new long-term projects with Fortune 500 companies than ever before. Typically, these lead to business relationships lasting years and create stability for future growth. The share of exports will continue to remain close to one hundred percent. We are certainly happy when, for example, TAYS (Tampere University Hospital) decided to buy our laser for its Eye Center, says CEO Seppo Orsila.

Modulight focuses on technologies where it sees opportunities for strategic differentiation, not only technically but also in terms of business models.

– For example, since 2015, we have been developing only devices that connect to our own cloud, cloud.modulight.com.

43 Likes

Does anyone understand that market better? To me, it sounds like a rather small niche that can quickly become saturated, and then you can throw your hockey sticks into the closet.

E. Furthermore, why does a small, highly profitable company want to go public right now?

4 Likes

Yes, I agree. I’ve been involved with glioblastomas quite a bit myself, and it’s very misleading for the CEO to make such claims when there is no (at least published) evidence for such numbers. Furthermore, due to the infiltrative nature of glioblastomas, it’s hard to believe that much better treatment responses could be achieved than with the current resection+radiation+temozolomide combo. Of course, the pathogenesis of this disease will be refined into much smaller categories based on certain mutation profiles in the near future, at which point treatments will also become more specific depending on the mutations the tumor possesses. But now I’m getting a bit off-topic.

But otherwise, this case seems very interesting. The figures for the last 2-3 years are indeed very promising. If a company can always achieve 50-60% EBIT%, it’s worth paying attention ![]() It also seems that the product is technologically very competitive in certain segments (albeit niche). Let’s wait for more information and material related to the listing and then chat more.

It also seems that the product is technologically very competitive in certain segments (albeit niche). Let’s wait for more information and material related to the listing and then chat more.

EDIT: Addition regarding glioblastomas.

49 Likes

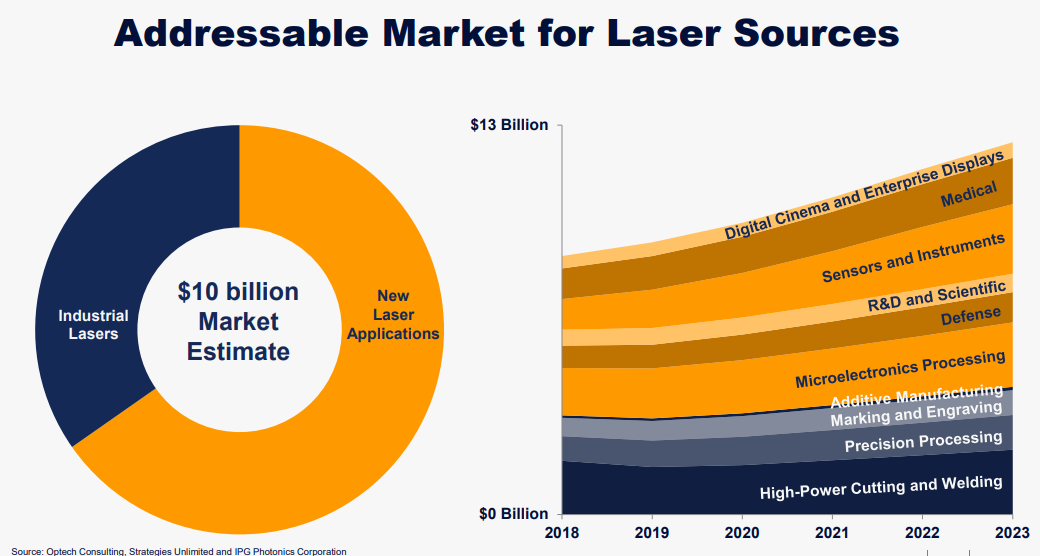

At least from the good materials of IPG Photonics Corporation (NASDAQ: IPGP), one of the largest or the largest player in this field, I found the following slide on market size.

Ten billion for the size of the entire global laser market is relatively small. And when the company has said that it has focused mainly on that medical segment and furthermore only on the United States and only on large companies and currently only on photodynamic therapy, then the TAM is indeed very small (less than a hundred million?).

But I do have difficulty grasping what the market in which this company actually operates ultimately is. The website and those articles emphasize that focus, healthcare, cancer, the United States, etc., but on the other hand, it says that the share of medical lasers has dropped in recent years from 70% → 50%, Europe’s share has varied between 10-30%, and Asia is on the rise. What are those other products and to whom are they sold, geographically? For the medical segment, strong zero growth is predicted for the coming years in this and in the earlier market report linked by @Contrafun. The growth of the entire laser market is predicted to come from sensors and optical communication. Of course, the company can grow geographically according to the strategy page, and expansion into glaucoma and refractive error surgical treatments, endoscopes, and dental care multiplies the TAM, but it also multiplies the number of competitors. If current profitability is based on focus, what happens when we start to branch out again?

34 Likes

Undeniably, it would be good to get a clarification from the CEO on what the comment about a 20-40 percent improvement potential is based on. That single comment leaves a bit of a bad taste, especially because the case otherwise seems very good to me. It makes me wonder what else might have been made to look too good? There shouldn’t be any need to exaggerate such a matter, if/when this investment case otherwise holds up. That’s why I find it somewhat odd, and I hope the matter will be brought up, for example, in Nordnet’s company presentation.

18 Likes

In my opinion, this illustrates a typical story: First, as a fresh company, they started doing and trying a bit of everything. Then they realized it was better to focus so they could learn to do what they do properly. Now that those few niches are being done really well and they are strong players in them, it’s a completely different matter to gradually expand into new categories and take control of them. Compared to a small company trying to do everything but excelling nowhere.

Instead of seeing it as sprawling, I see more potential for controlled expansion now that the foundation is solid and the business is profitable.

25 Likes

After a quick and superficial investigation, the company as a whole looks promising. This forum seems to have so many experts and so much knowledge (swarm intelligence) from all fields that any dishonesty would easily be caught. I see that this stock market listing can still be ruined by two things. One is greed (overpricing the stock market listing). And the other is dishonesty (lying).

3 Likes

I’ve had a couple of dealings with the company through my work and have also met with the CEO. My general impression of the firm was positive, and I personally consider it a plus that the business focuses on improving the quality of cancer treatments. Was there more detailed information somewhere about how long they’ve specialized in this “niche”? I got the feeling of a moat. However, the above is based on intuition. I’m following and intend to participate if I can get some scraps.

29 Likes

TJ in an interview with Aamulehti:

"It must be remembered that many studies are still in their early stages. In most cases, there is still a long way to go before they become accepted best practice recommendations.

So far, early-stage studies have been conducted. These are not yet approved forms of treatment.

“I am happy with the results, but it is unnecessary to draw any definitive conclusions yet. However, it seems that treatment outcomes can be improved.”

14 Likes

- Higher price => less popular offering => more shares

- Lower price => more popular offering => fewer shares

Choose one. It’s probably all the same in terms of returns.

3 Likes

You can ask technical questions in this thread Suuri IPO / kaupankäynnin ketju: tekniset kysymykset - Osakkeet - Inderes forum

4 Likes