The year 2025 is over, which means it’s time to repeat the cliché and reflect on the past year.

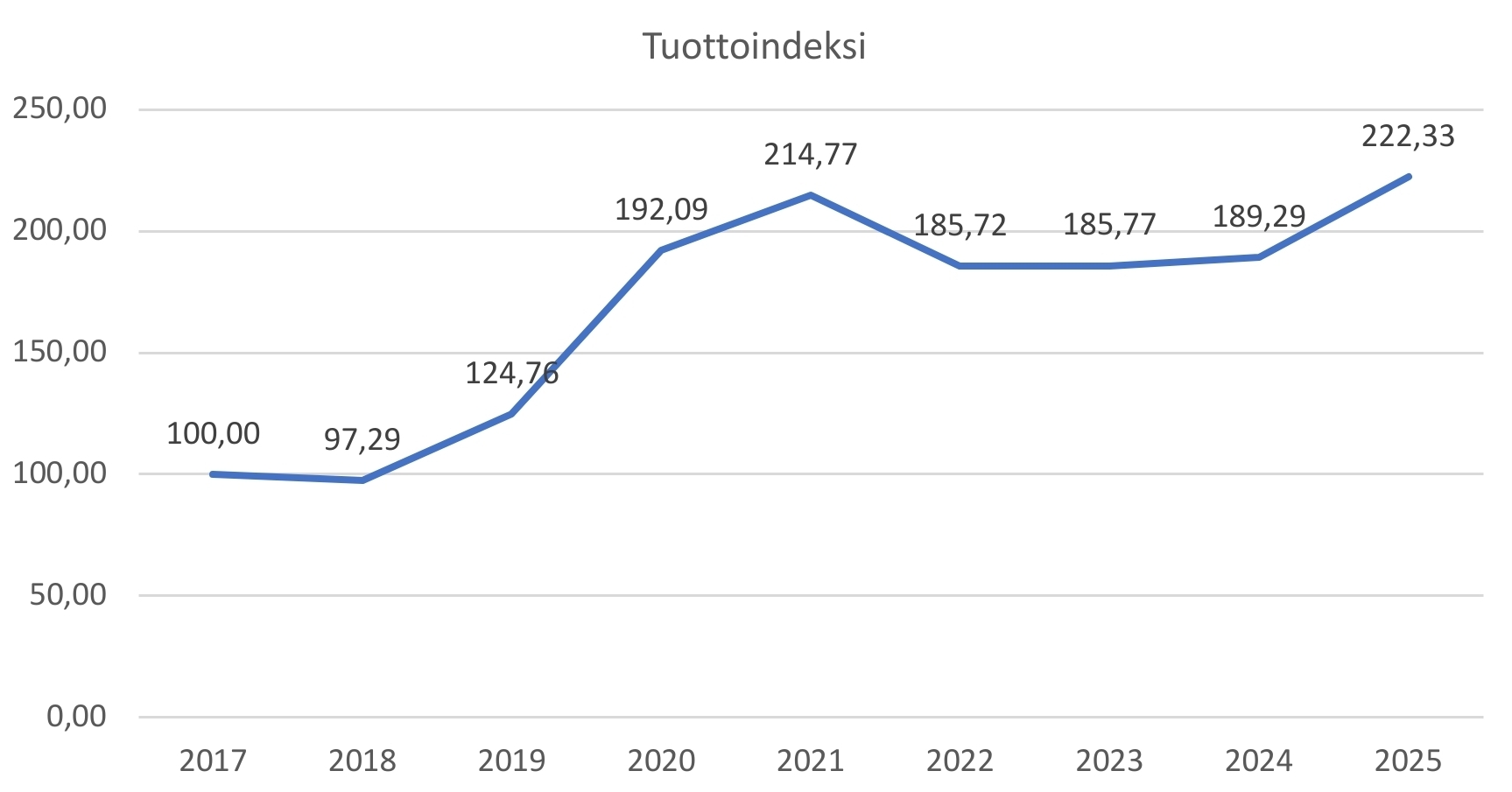

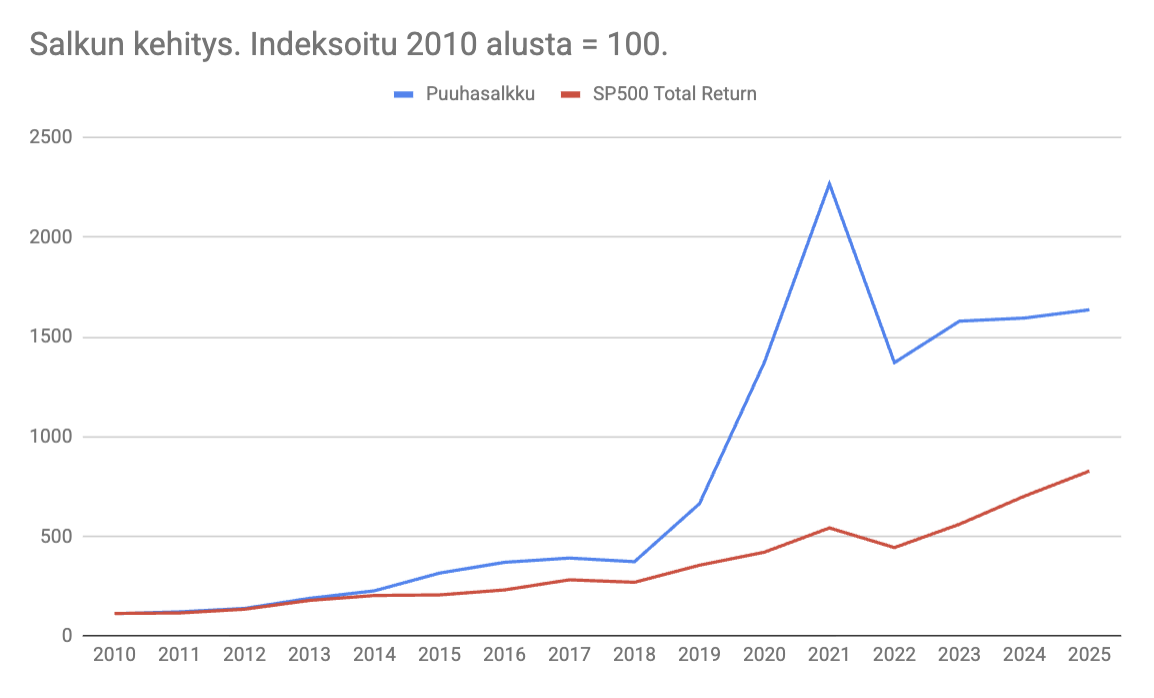

When I look at my investment year, my feelings are twofold. In terms of returns, I have significantly lagged behind Hesuli (the Helsinki Stock Exchange). My total return for 2025 was 8.63%, which clearly underperformed the market return. Naturally, I am not satisfied with this. Like many others, I would love to showcase stellar returns here, but my strategy will likely never make that a regular occurrence.

I primarily own quite “boring” companies that should create value year after year without much drama. In the long run, however, I hope to generate steady, boring returns that beat Hesuli over a long period. On the other hand, during individual years when the market rises sharply, I don’t expect to be invited to the party.

On a positive note, I feel I have grown as an investor again this year. I’ve focused more on studying how companies can create value for their shareholders, and in the long run, I believe that is a worthwhile subject to dive into. Aside from a few stumbles, I have stuck to my investment style of trying to find good companies at a reasonable price (and who doesn’t try to do that).

Towards the end of the year, I took some distance from the market and focused more on the companies themselves. We live in a world that becomes more intense by the second. News, data, and opinions are constantly at our fingertips, and when things start happening in the market, it’s easy—at least for me—to get the feeling that “I have to do something.” This sense of constant optimization hasn’t done my portfolio any favors in the past. That’s why I eventually pulled the handbrake and decided to go in a completely different direction. I came to the conclusion that I should only look at my portfolio once a week, preferably on the weekend when the exchange is closed. Of course, if I see during the week that a portfolio company or something on my watchlist has dropped -10%, I won’t forbid myself from buying. This is a hobby, not a law. However, I sometimes find myself taking investing too seriously, which is why I try to avoid staring at my own portfolio. Tracking gains and losses specifically makes me feel uneasy—so why would I inflict that feeling on myself? Watchlists that don’t include my actual portfolio have been a good alternative for me lately.

My investment style hasn’t changed during the year, but I want to emphasize predictability and boredom even more in my large positions. In smaller positions, I can take on more risk and thus increase the portfolio’s optionality, where a small position could potentially grow large if my analysis hits the mark. If I’m wrong, the damage is limited.

I thought I’d focus for a change on discussing the companies where price development didn’t go as I expected during the past year.

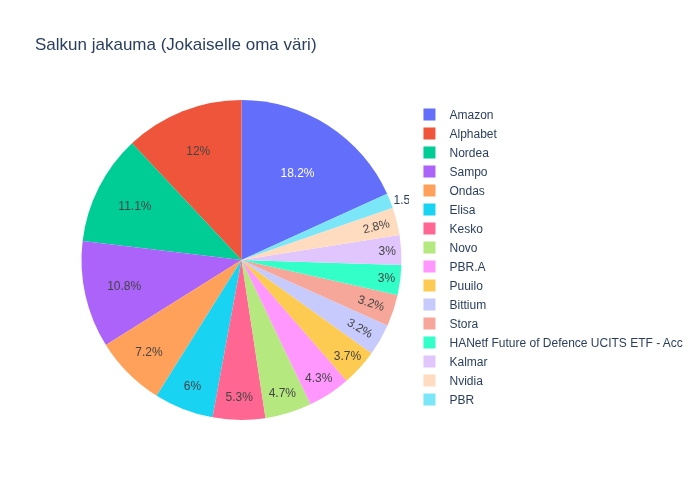

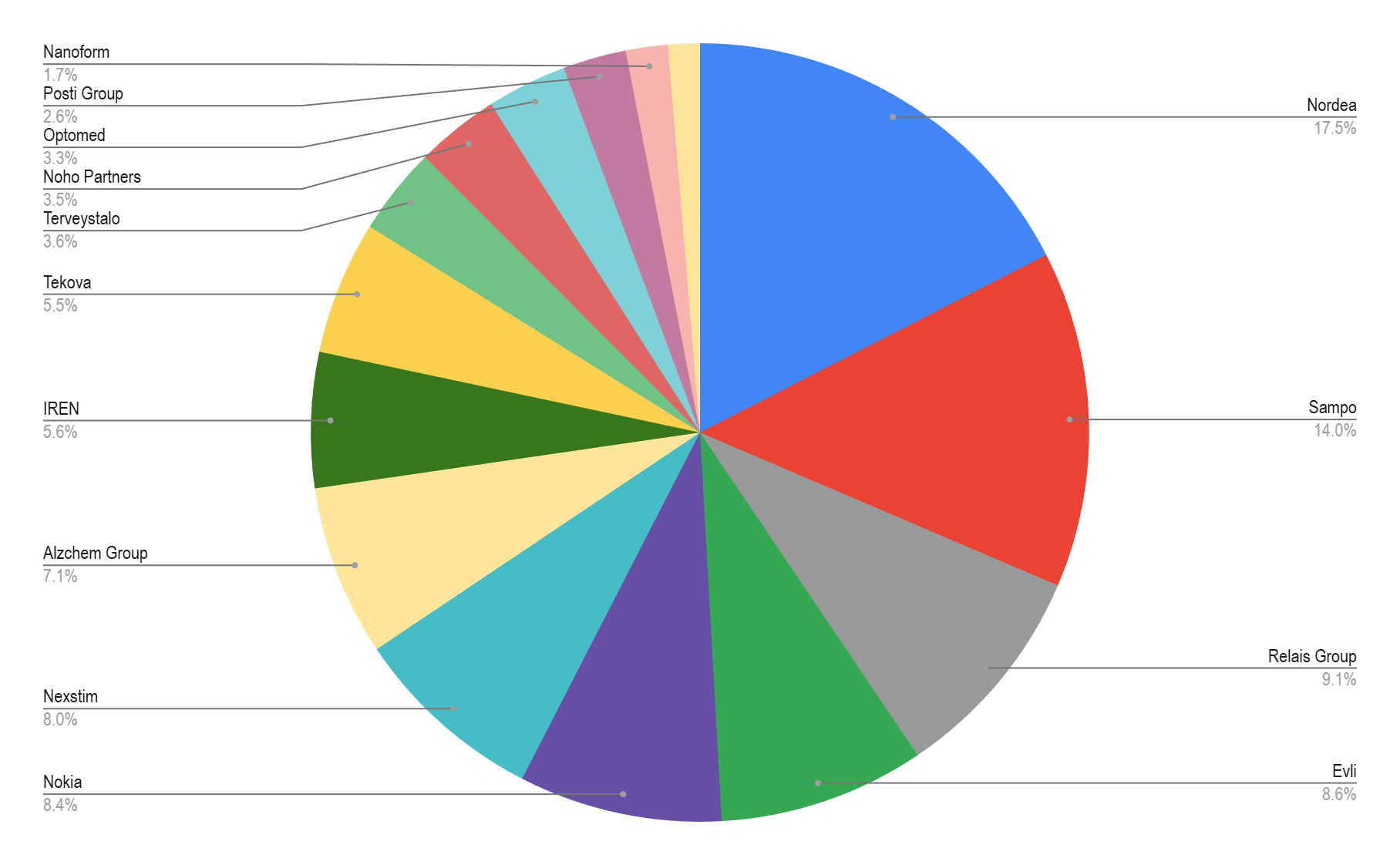

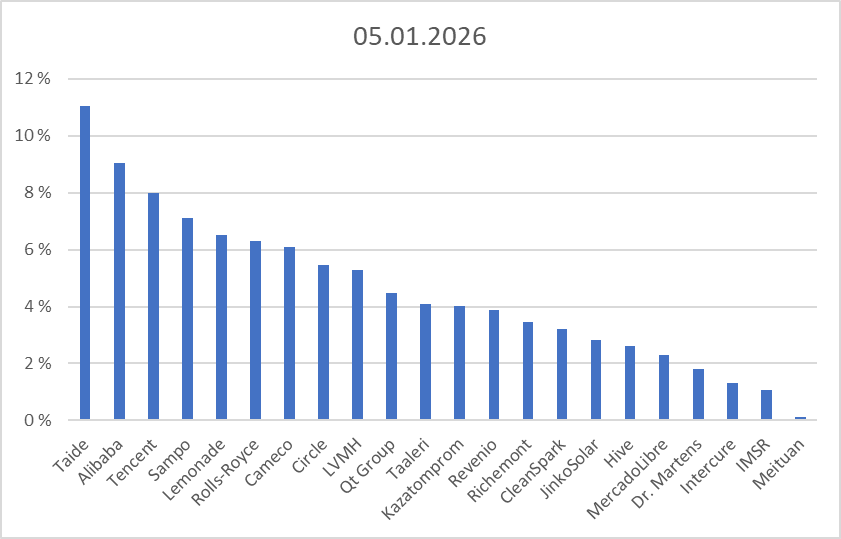

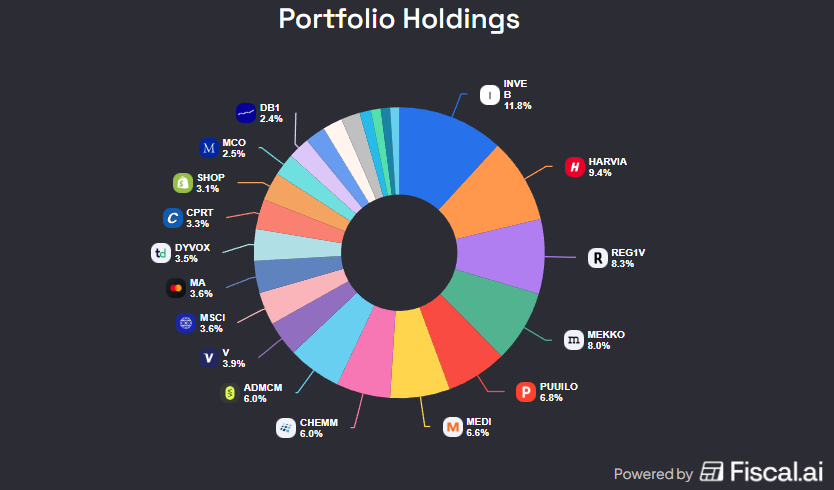

Revenio 8.5% position

Revenio was my biggest miss of the year. I expected earnings growth this year, but revenue still isn’t growing fast enough to cover increased costs. Additionally, the company has faced headwinds from the dollar, which has weakened the bottom line. Return on capital figures have naturally weakened in tandem since NOPAT isn’t growing, meaning a sort of creeping mediocrity threatens the company. Relative to that, my position is quite large. Am I worried? Partially. I believe part of the reason has been the market and that the company has drifted into a kind of limbo. The market for private acquisition targets has been expensive, which has resulted in the next growth leap not being made by buying the “missing piece” of the company. The competitive advantage has likely not weakened, but if the underlying market is soft, the company has settled for distributing cash in the form of dividends instead of pursuing growth. That is, of course, the only right solution for the owner when the expected return on an acquisition is insufficient, but I would hope my portfolio companies could grow NOPAT year after year, and apparently, the underlying market hasn’t allowed for this in recent years.

Copart 3.4% position

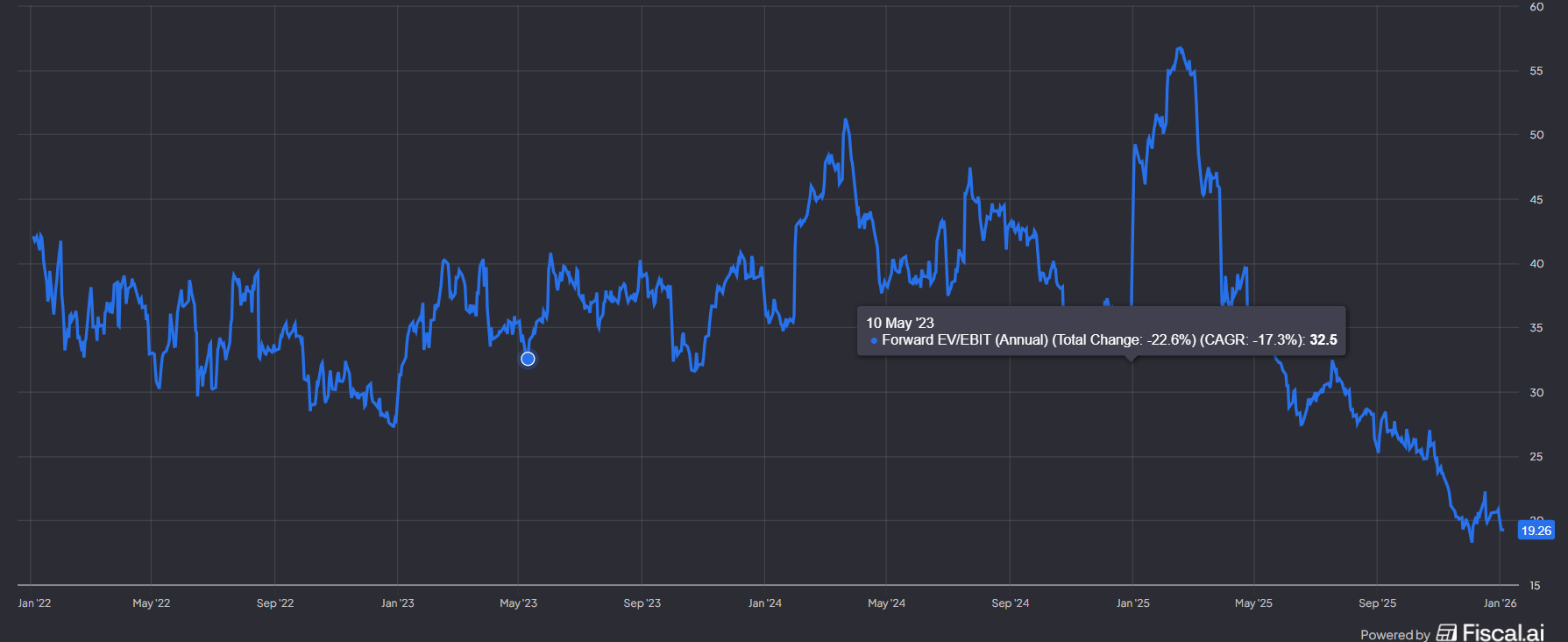

When you pay high multiples for quality and the market starts to doubt the investment thesis, the result is often ugly. Copart’s 12-month return is -32%. EV/EBIT multiples have nearly halved from the 2024 peaks. There are several reasons for this. The market has questioned the company’s market position as competitor IAA’s position has strengthened, at least momentarily. The company’s domestic market has proven difficult as the number of uninsured vehicles has grown. Investors are also keeping an eye on the company’s significant cash position.

Copart has previously successfully allocated capital to land and bought back its own shares opportunistically. To top it all off, Copart is on the “wrong side” of the AI trend. Am I worried? Not really; I still believe this is mostly a temporary situation where investors are questioning whether the company is as good as before due to external factors; additionally, multiples have normalized. Copart is known for not allocating capital just because the market wants them to, but rather waiting persistently until attractive options are available. I will continue to hold, but I don’t expect a quick change in multiples or for growth to take off wildly. Therefore, I’m not adding more until I see a clear change in the trend. I’m sitting in a hole, but I’m not going to keep digging.

Hemnet 1.1% position

Hemnet’s share price drop has been staggering. The 12-month price performance is -55%. The company is still a new position for me, so fortunately I haven’t been catching falling knives the whole way down. The company is Sweden’s largest portal for home buyers and sellers. Aggressive pricing has become a headwind for the company, and the less user-friendly but cheaper competitor Booli has taken market share. Hemnet’s multiples were sky-high and the company was a darling of investors until the market started doubting the sustainability of the pricing and thus future growth. Forward-looking EV/EBIT has collapsed as strong growth is expected to slow down.

It should also be noted that the real estate market in Sweden has been challenging, which has complicated the market. However, Hemnet has already made changes and experimented with different pricing styles that can lower the seller’s risk when choosing a more expensive advertising package. Hemnet’s trump card has been that it attracts the most eyes. This way, selling prices have also been better, meaning the price charged to the listing party has been tied to the value brought by the platform. I am, of course, a little worried, but I don’t know the company well enough yet to have a strong opinion on its future. Therefore, the position remains small and I am monitoring the situation.

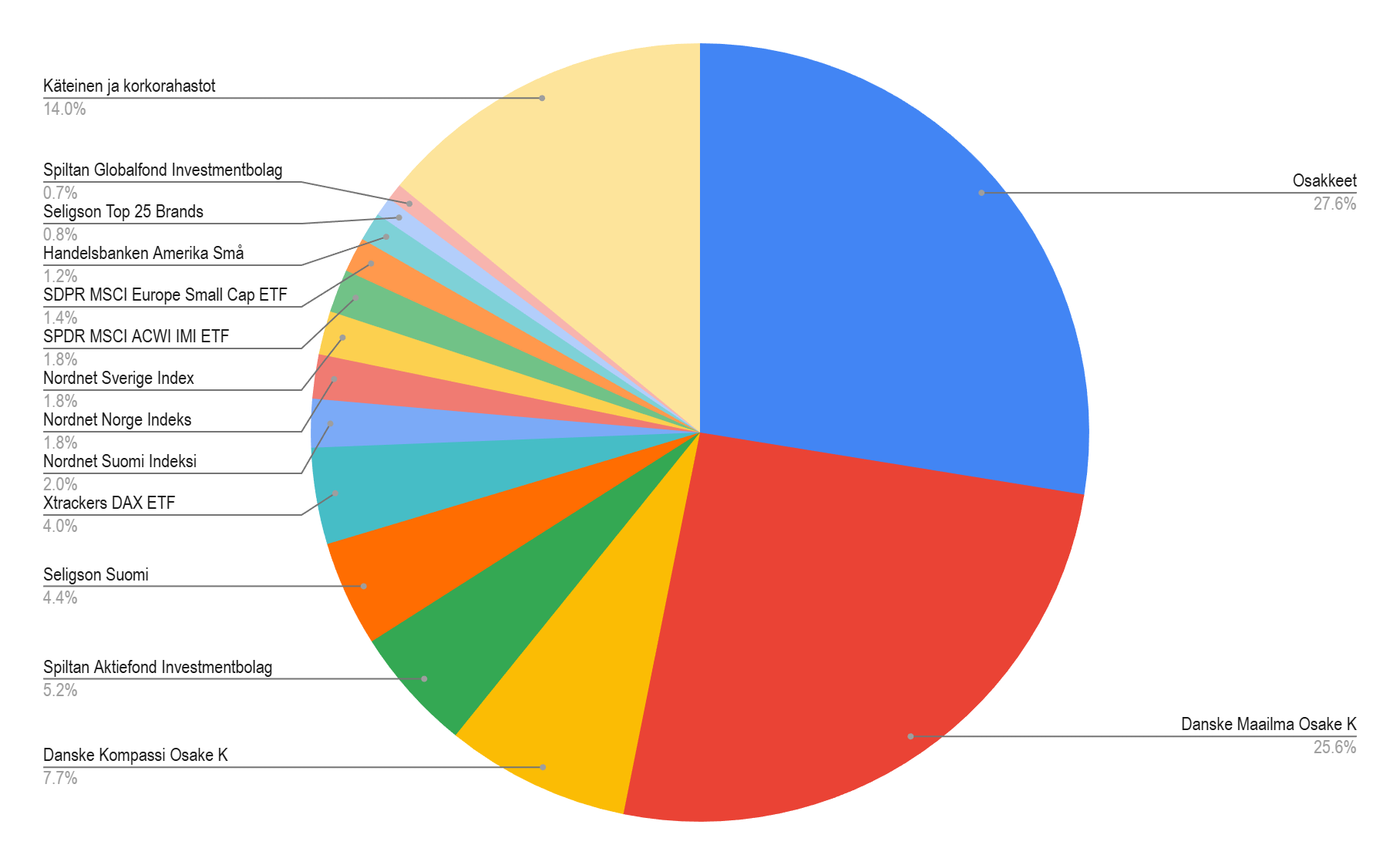

There have been no dramatic changes in the portfolio. During the last quarter, I have continued to add to several companies. The largest additions have gone to Deutsche Börse and Medistim. As new positions, I have bought the aforementioned Hemnet, Carasent, and Toast. Of these, Toast is still under evaluation; this might have been one of the year’s mistaken purchases. The more I’ve thought about the nature of the business, the more I’ve come to the conclusion that the company may not necessarily meet the criteria I hope for in a portfolio company. I sold Nordea, which was quite a significant position in the portfolio. It’s hard for me to justify the company’s valuation level anymore. Furthermore, banks have the downside that every now and then somewhere in the world, some bank gets into trouble, and then the whole industry suffers. Therefore, I felt now was a good time to exit while the music was still playing. European banks have had their best period in decades.

I don’t have a new recipe for success for 2026. If the same trends continue in the market as last year, I will likely lag behind the index again this year. I have about six companies on my watchlist that I would be ready to buy if the price is right. Monitoring and chasing these will surely be the main theme of the year.Finally, I would like to highlight my favorite book and podcast discovery from last year. The book is easily What I Learned About Investing from Darwin. It has been praised many times here on the forum, and I can only agree. It is an excellent and timeless book that can be read multiple times. An honorable mention naturally goes to McKinsey’s Valuation, which I am still in the middle of.

As for a podcast, I would highlight The Art of Quality, which I believe is still a fairly underrated pod. It is primarily investment-themed, but quality is explored from multiple dimensions with the help of guests from various fields. Truly interesting listening.

A very happy New Year to everyone!