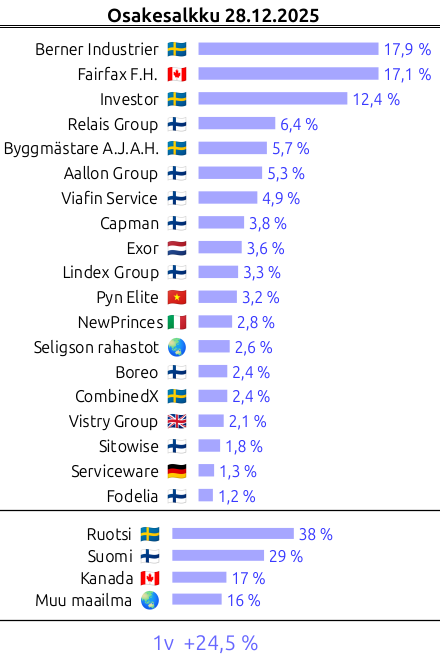

The stock market year was strong (especially in Europe), which was also reflected in my portfolio. The portfolio is more concentrated than before. 47% is in the three largest investments. It is noteworthy that Fairfax and Investor have built-in diversification as companies. Berner Industrier is a smaller company with a long history. Its situation and outlook look good at the moment. All of them are steady-growth compounders whose industries, at least, are not going to be disrupted by AI anytime soon. Let them grow in peace for now without the pruning shears.

NewPrinces was a new addition to the portfolio. It is an investment company that owns companies focused on food brands. NewPrinces’ most valuable holdings are the recently London-listed Princes Group and the Carrefour retail chain, acquired this year. With the aforementioned acquisition, NewPrinces wants to include the direct-to-consumer distribution of its food brands in its repertoire. NewPrinces’ valuation seemed quite attractive at the time of purchase, and it still does. However, Princes Group’s IPO was a disappointment in terms of valuation, which has weighed on the share price. NewPrinces still owns over 80% of Princes Group. If PG’s business goes well, the valuation will surely follow, largely flowing into the pockets of NP’s shareholders. Carrefour’s profitability as part of the group will only become clear later and may be the biggest question mark in the equation. After all, the previous owner could not make the chain profitable. The competition authority approved the deal very recently (December 1st). Other companies owned by NP are Diageo and Centrale del Latte d’Italia. As far as I know, the intention is to sell them to Princes Group at some point.

Among the old holdings, Berner Industrier has performed strongly, and Fairfax is at ATH (all-time high) levels. I believe Fairfax is an investment with an excellent risk/reward ratio that can be held indefinitely. I recently increased its weight. Fairfax was added to the S&P/TSX60 index on December 22nd, which could raise its low valuation. Exor’s performance has been a bit sluggish, but I still believe there is hidden value in the company that can gradually be unlocked piece by piece. An example of this is the recent offers for Juventus—in the range of up to €2 billion for Exor’s ownership stake. The Finnish serial acquirers, Aallon Group and Relais, have grown during this year as well, in line with their strategies. Their valuations haven’t changed much compared to a year ago. They are still relatively cheap. In Boreo, the CEO change was unfortunate, but the economic cycle and the company seem to be heading in the right direction.

US banks. Cyclical, sensitive to interest rates and the economy.

The average annual expense ratio for the ETFs is 0.46%, and generally, the goal is to hold the ETFs and sell the stocks for a profit. About 80% is in ETF funds and the rest in stocks, which is quite a decent allocation.

Let’s list my own stock investments here for review with brief comments/rationales, while also putting my scattered thoughts into writing. This year, risk-taking and a Helsinki-heavy (hesuli) allocation have paid off, but perhaps during next year, it would be wise to increase geographical and sector-specific diversification.

100% - ESA & BEA Total, YTD Return 55.13%

I use two portfolios; in my opinion, the ESA (Equity Savings Account) now has at least a sufficient number of positions, and the BEA (Book-entry Account) is then used for slightly better diversification.

76.44% - ESA Total, YTD Return 76.29%

Naturally, most of the investments are on the ESA side for tax reasons, even though I make clearly fewer than 1 trade/month and prefer to invest primarily in growth companies.

34.45% - Bittium, The stock’s valuation and weight in the portfolio are already quite steep, but I’ll stay on board for now due to the good market situation. The portfolio’s returns are largely thanks to this stock. However, a more detailed plan for selling/trimming should already be prepared.

9.89% - Kone, Bought into the portfolio as a pillar to accompany the growth companies.

8.76% - Harvia, A high-quality growth company with big potential; I’d even like to increase the position. Perhaps if there’s another dip that I consider unjustified.

7.74% - Olvi, A defensive company & a convincing growth strategy.

3.34% - Canatu, An interesting investment target, which to be honest, I don’t understand all that much about—in other words, a lottery ticket. The intention is to study it more closely and then make decisions on the future.

3.25% - Huhtamäki, Has stagnated in the red in my portfolio for a long time, but at this valuation, it can stay for now.

2.65% - Kempower, High potential and also high risk, but with such a small weight, I am willing to take that risk. Of course, the average price is €23, so the risk has already partially materialized here, although the purchase price doesn’t really matter as such on an ESA.

0.76% - Cash, The last of the long-held large cash balance has been put to work this year, but I wouldn’t mind if the share of cash slowly started to grow again.

23.56% - BEA Total, YTD Return 8.34%

I keep part of the investments on the BEA side for three reasons:

easier to diversify (outside of Finland and otherwise) e.g., through ETF funds.

Investments can be withdrawn for other uses with potentially a lower tax burden.

The use of an investment loan is possible. If Nordnet’s loan terms didn’t offer an advantage for diversification, there would likely be only one ETF in the portfolio besides Investor, whereas now the plan is to diversify cash into new ETFs.

7.47% - Investor, Diversification into the neighboring country and unlisted companies through an investment company with a convincing track record.

3.72% - (IS3N) iShares Core MSCI EM IMI UCITS ETF USD (Acc), More diversification.

0.52% - (SXR8) iShares Core S&P 500 ETF USD (Acc), A small position left over from previous hasty moves; let it serve as a tracking position for now.

6.37% - Cash, More cash is coming in from outside the portfolio when the apartment is sold. I also intend to continue monthly saving once my own financial situation clears up a bit; in addition to these, a credit limit is available. However, I have been cautious about increasing equity weight while fearing/hoping for a bigger crash – on the other hand, for the same reason, good returns have been missed in the past.

Investment Plan: A fixed amount is allocated to funds monthly, approximately 15% of net salary. Funds/ETFs are purchased to balance geographical diversification if there is extra cash in the account. A lump sum has been reserved for stocks and will not be increased. Additional purchases must be made using dividends and proceeds from sales. After a purchase, a one-month waiting period is required before the next buy. In the long term, my portfolio will consist mainly of index funds and high-quality dividend-paying stocks. Stocks are primarily sought from Finland to ensure as much of the dividends as possible are received tax-free into the equity savings account (osakesäästötili).

Outside of direct stock picks, things have been very serene. Monthly savings roll into indices with steady lethality, regardless of how many wrong moves I make in stock picking. This year clearly belonged to Europe: index funds investing in the old continent have returned an average of about 20% this year. As many know, investing in the Helsinki (Hesuli) index would have yielded a nice 35% return this year. But because my own stock portfolio invests primarily in Finnish stocks, a Finnish index fund is unfortunately not in my portfolio at the moment.

The share of emerging markets in my portfolio rose by a few percentage points, partly because I decided, after much consideration, to return as a client of PYN Elite. This was mainly influenced by 1) a temporary discount on the subscription fee to 4,999 euros, 2) the fund becoming attractively cheaper towards the end of the year, 3) FTSE upgrading Vietnam from a frontier market to an emerging market, and 4) the fund’s updated optimistic view of the Vietnamese market + Petri putting more of his own money in.

Perhaps the most interesting thing from the last half-year comes here:

Surely many have noticed that the last couple of years have been a celebration for precious metals. Gold started rising two years ago, and silver went completely out of hand this spring. ETFs investing in mines and silver have grown by about 150% this year. Gold has doubled in three years. For now, I intend to sit on my hands, but since I admit these are pure speculation, I have already started thinking about selling silver. The price of silver is full of very rapid rises and even faster falls, so as a novice, I would perhaps rather sell too early than too late. I will likely keep gold and mining stocks in the portfolio for a long time, unless something particularly tasty opens up in the indices.

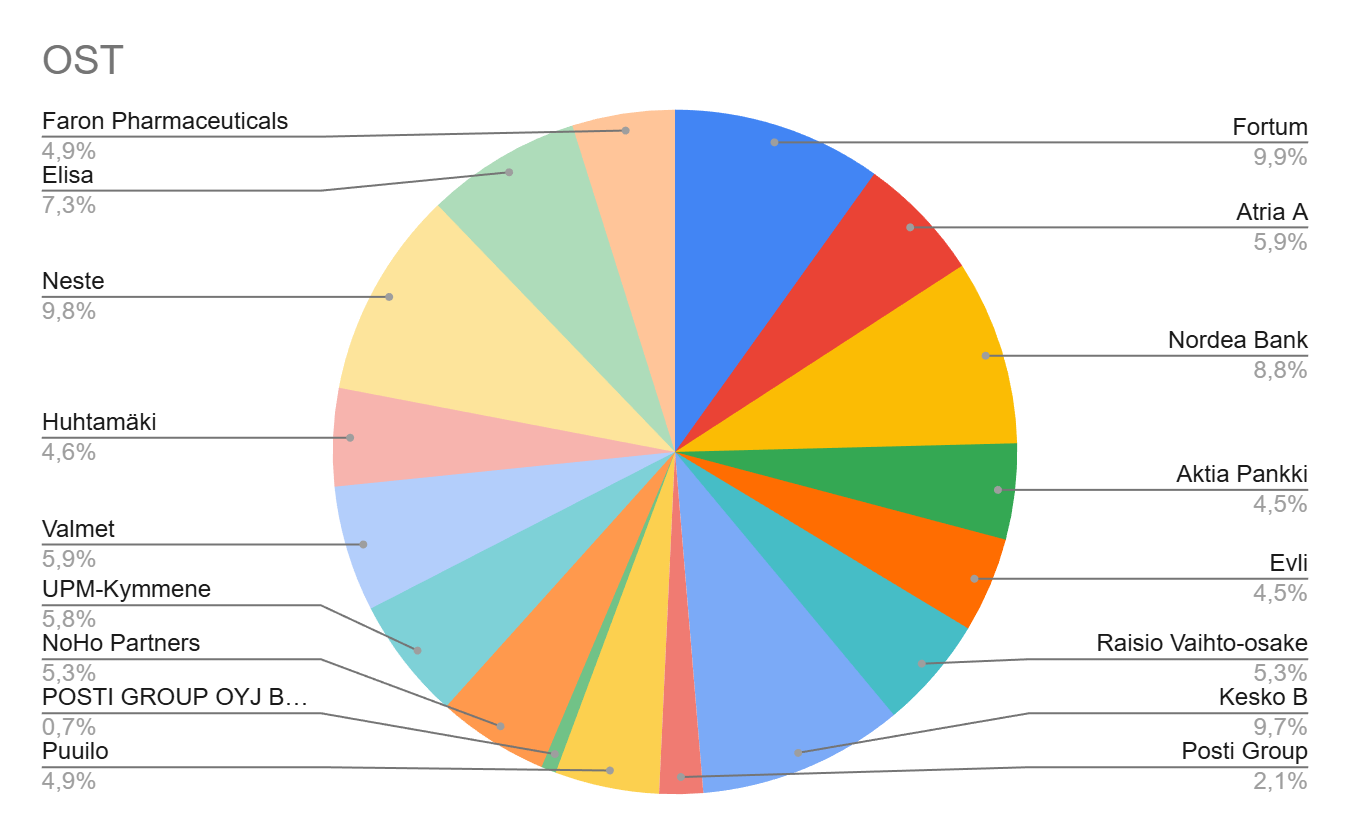

Stock Portfolio:

Bought: Terveystalo (9.32e), Huhtamäki (31.6e)

Trimmed: Orion (67.15e)

Sold: Tietoevry (18.03e)

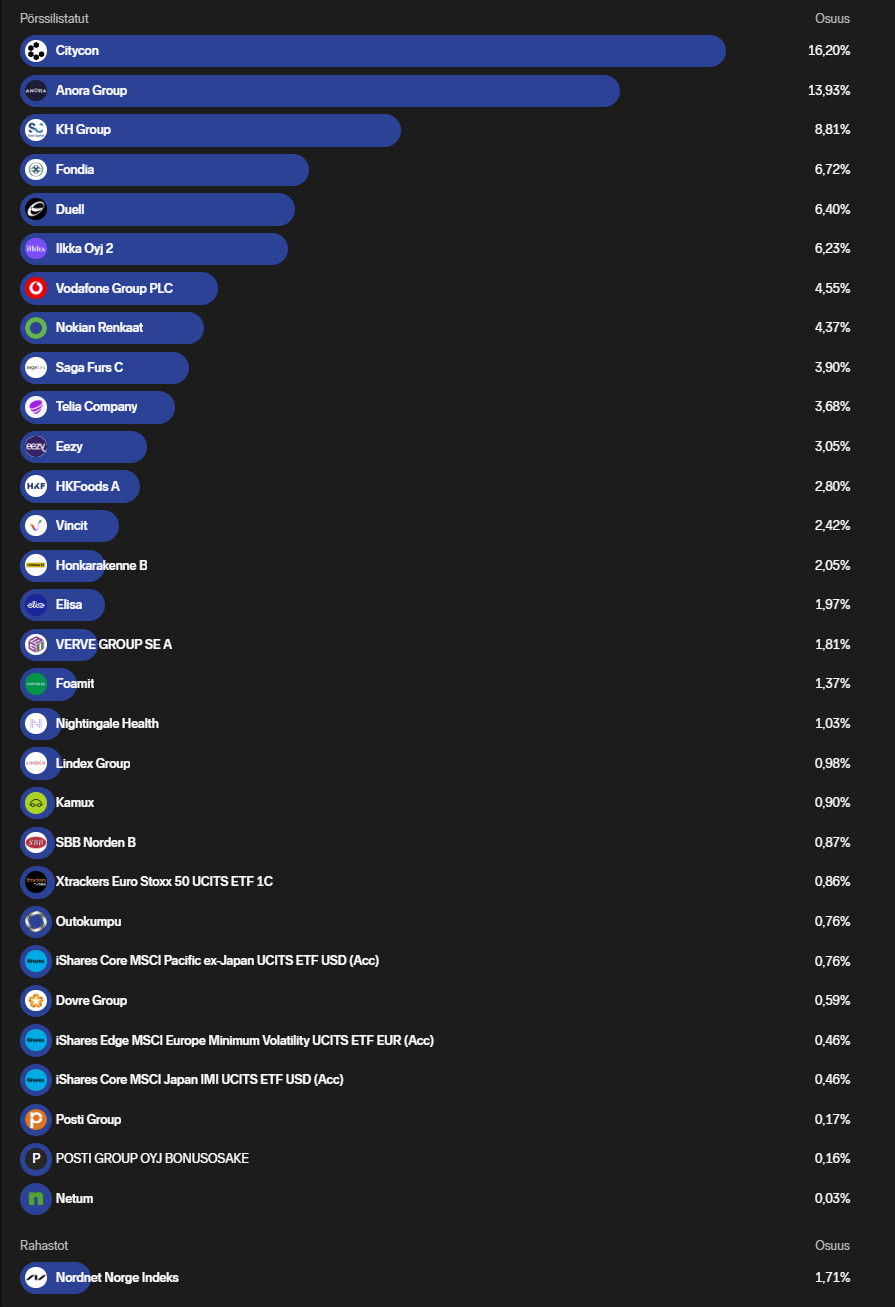

Listed Stocks

Share of Stock Portfolio

Nordea Bank

9.5%

Nokian Tyres

9.2%

Kalmar

5.9%

Neste

5.3%

Huhtamäki

4.6%

Valmet

4.5%

Terveystalo

4.2%

Orion B

4.1%

Viafin Service

4.1%

Orthex

4.1%

NoHo Partners

3.8%

Detection Technology

3.6%

Marimekko

3.2%

Tokmanni Group

3.2%

Cash

31%

In the last six months, very few direct stock purchases have been made. Probably precisely because the Helsinki exchange (Hesuli) has risen by 35% this year and my strategy is to find “quality dividend payers in the bargain bin.” At the moment, nothing really catches my eye within my comfort zone, so I am waiting calmly for better buying weather. Tokmanni, Orthex, and DT are, in my opinion, still at buy prices, but I think I would rather add more diversification to my portfolio than add to bright red rows. At the beginning of the year, there would have been a chance to buy Aallon Group, Wärtsilä, and Lassila & Tikanoja, but I hadn’t done my homework. Fortunately, I at least realized not to sell my loss-making Nokian Tyres and Neste at the bottom, as light is finally starting to show at the end of the tunnel

Of course, that 31% cash weight in the Equity Savings Account (OST) is burning a bit of a hole, but the amount of cash in the entire portfolio (reserved for both stocks and funds) is only 6% of total wealth, so I am still quite firmly in the market. Let’s wait quietly to see if we catch any fish

Happy New Year and successful stock picking to the entire forum community!

YTD +11,71 % (kaikkien kulujen, korkojen ja verojen jälkeen)

Q4/2025 alkaa olla valmis, ja edellisen kolmen neljänneksen tavoin kvartaali oli hiljainen aktiviteetin osalta. Fokus alkoi siirtyä enemmän uusien potentiaalisten salkkuyhtiöiden tutkimukseen ja shortlistin kehittämiseen, jotta jatkossa olisi helpompi ja nopeampi reagoida houkuttelevan yhtiön tullessa alennuskoriin.

Myynnit, Q4:

Strathconasta myin OST:lla olevan osan pois MEG-yritysostosekoilun keskellä. Voittoa tuli mukavasti lyhyellä sijoitusajalla, vaikka MEG päätyikin Cenovuksen haaviin eikä siksi asiat menneet täysin toivotusti. Lisäksi vuodenvaihteen tilejä tasatessa myin Investor-position pois. Rivi oli salkun pienin, korkeimmin arvostettu, enkä rehellisyyden nimissä löytänyt mitään muutakaan fiksumpaa myytävää, joten tällä kertaa näin.

Lyhyet kommentit salkkuyhtiöistä:

Fairfax: YTD +30 %. Kolme kaunista vuotta salkun ykkösenä, ja jälleen kerran voi todeta vuoden olleen loistava. @lazyway avasikin hieman yhtiön tapahtumia jo yllä, mutta lisäksi arvonluontia on kvartaalilla jatkettu Kennedy-Wilsonin ostotarjouksella ja Eurolife-henkivakutuusyhtiön myynnillä (tästä 300 MEUR voittoa Q1/26-raporttiin, yay). Ensi vuonna jatketaan hajautusta vakuutusyhtiöiden ulkopuolelle, ostetaan Allied Worldin vähemmistöosuudet pois, ja tehdään buybackeja - tuloskasvu jatkunee siis hyvinkin ennustettavana. Välillä täytyy ihmetellä, että vaikka ensiostoista on jo nelinkertaistuttu, niin tätä saa vieläkin alle 10x tuloksen.

Linamar: YTD +48 %. Arvosijoitus isolla A:lla on tikannut yhä kohti koillista kertointen normalisoituessa kohti kelvollisen teollisuusyhtiön lukuja. Casen tärkein osa, eli autobisneksen kannattavuuden kasvu tuli Q3:lla läpi huolella, mikä käytännössä katsoen korvasi teollisuuskoneiden markkinan romahtamisen yhtiön alta. Yhtiö teki myös kaksi yritysostoa lokakuussa, käyttäen vahvaa tasettaan ostaakseen EV/EBIT 5-6:n pintaan kaupan olleita autonosatehtaita Saksasta ja USA:sta. Myös buyback-konetta käynnisteltiin uudelleen, mikä lämmittää sydäntä osakkeen treidatessa 0,8x bookilla. Ensi vuodelle olisi toiveissa lisää järkevää pääoman allokointia ja buybackeja matkalla kohti historiallisia kannattavuus- ja arvostuskertoimia.

Nelnet: YTD +25 %. Yhtiön Q4 on ollut melko rauhallinen: yhtiö osti opintolainojen hoito-/palvelubisneksen Kanadasta lisäykseksi portfolioonsa, ja dumppasi totaalisen epäonnistuneen aurinkoenergian rakennusbisneksensä toivottavasti johonkin todella kauas konsernista. Lienee selvää, että yhtiön laatu parani näiden järjestelyiden myötä, mutta siihen olisi riittänyt viimeksi mainittu yksinäänkin.

Muuten ei mitään kummoista kerrottavaa Nelnetin loppuvuodesta. Tavoitteena olisi pitää yhtiö salkussa compoundaamassa koko vuosi 2026, eikä taas veivailla osakkeita edestakaisin kuten tapana on aiemmin ollut.

AerCap: YTD +50 %. AerCap tykitti hävyttömän kovan Q3-tuloksen, ja osake on sen jälkeen jatkanut liitoaan ylöspäin - viitisen prosenttia osakkeista silputtiin kolmessa kuukaudessa, ja en yhtään epäilisi, jos sama tahti olisi jatkunut myös Q4:llä. Ylärivi paisuu hitaasti ja varmasti, mutta kalustomyynnit yli kirja-arvon ja valtavat takaisinostot pitävät huolen siitä, että osakekohtainen arvo paisuu kuin pullataikina (vuodessa 20 %:n kirja-arvon kasvu / osake). Markkina ei vieläkään ylihinnoittele tätä kasvukonetta (P/B 1,3, kirja-arvo selvästi alle todellisen), mutta parhaat alennushinnat ovat jo kurottu umpeen.

IGIC: YTD +7 %. Vuosi ei ole ollut valuuttakurssivaikutusten ja Q1:n Kalifornian vahinkojen myötä häikäisevä, mutta samanaikaisesti firma treidaa P/B 1,5:n ja P/E 9:n pintaan tykittäen 20+ prosentin pääoman tuottoja. Sijoittajaystävällinen johtoryhmä on palauttanut sijoittajille vuoden aikana osinkoina yhden dollarin, ja takaisinostojen muodossa toisen. Nettokassaa on sen verran paljon, että ensi vuonna voittoa jaettaneen samanmoinen summa. Holdaus jatkuu, ja en yllättyisi, jos yhtiö kiinnostaa jotakuta ostokohteena.

NewPrinces: YTD +58 %. Q4:n uusi osto, ja tätäkin @lazyway yllä jo ansiokkaasti esitteli. Ostohetki oli luultavasti paskin mahdollinen - osake sukelsi saman tien 30 prosenttia, mutta hiukan omien sääntöjeni vastaisesti pidin laput salkussa. Muutos ei perustunut fundaan käytännössä yhtään, joten en nähnyt syytä panikoida.

Miksi ostaa italialaista ruoka-kauppias-brändiketjua? Siksi, että yhtiön luvuissa ei ole mitään järkeä. Reippaan 800 MEUR:n arvoinen, defensiivisen alan kasvuyhtiö treidaa 2x EBITDAlla ilman minkäännäköistä taseongelmaa. Firman molemmat bisnekset (Princes ja Carrefour) tuottavat reipasta vapaata kassavirtaa, ja vaikka nykyisellä raportoidulla tiedolla on äärettömän tuskallista saada selkeää kuvaa tarkasta potentiaalista, niin hyvässä tapauksessa tämä treidaa 25 %:n FCF yieldillä ilman nettovelkaa. Carrefour-ostos ja sen integrointi saavat kumpikin epäonnistua todella pahasti, jotta tuotot jäisivät millään tavalla heikoiksi - nyt puhutaan todella huokeasta firmasta alalla, jonka sentimentillä on varaa parantua.

Kasvutarina jatkunee Princesin puolella yritysostoin, ja Carrefourin puolella taas myymäläverkoston kehittämisellä ja kannattavuuteen panostamisella ennen suurempia kasvutavoitteita. Strategia jatkoon on siis selkeä - täysin päinvastaista kieltä kertoo yrityksen luvut, jotka ovat hujan hajan eri hankintojen ja IPOjen jäljiltä, samalla peittäen yhtiön potentiaalin melko tehokkaasti alleen. FY2025-tulos julkaistaan maaliskuun puolivälissä, ja tuolta raportilta toivon ennen kaikkea selkeyttä siitä, mikä on NewPrincesille emoyhtiönä kohdistuva tulos, kassavirta ja velkalasti.

Seuraava 12 kuukautta näyttänee tehokkaasti, että millainen sijoitus tuli tehtyä. Realistinen parin vuoden potentiaali on mitä tahansa osakkeen kolminkertaistumisen ja puolittumisen väliltä. Luottoa on, että odotusarvo jää silti reilusti positiivisen puolelle.

Secure: YTD +10 %. Secure lienee heikoiten performoinut salkkuyhtiöni koko vuonna. Kannattavuutta söi vuoden mitassa kasvupanostukset uusiin hankkeisiin sekä öljyn hinnan heikentyminen, mikä tekee Securen talteenotetun öljyn myyntikatteeseen ikävän loven hyvin nopeasti. Firma sai kuitenkin vahvistettua alkuvuoden yritysostolla kierrätysbisnestään, ja myös takaisinostoja tehtiin kaksin käsin läpi vuoden (yli 8 % osakekannasta tuhottu).

Secure on hieman vaikea tapaus. N. 7 prosentin FCF yield ei ole sellainen halpa hintalappu, jota yleensä haluaisin maksella yhtiöistä. Toisaalta tuotto tulee pehmeän kannattavuuden ja merkittävien kasvuinvestointien jälkeen, eli tuotto tulee lähes pomminvarmasti kasvamaan, etenkin kun tähän yhdistetään reilut buybackit. Kasvuodotuksia on hinnassa eri tavalla kuin suurimmassa osassa muiden salkkuyhtiöideni osakkeissa, ja se tästä tekeekin vaikeamman holdattavan. Verrokkeihin nähden tämä on silti selkeästi halpa - kertoimet ovat luokkaa 60 % kilpailijoiden vastaavista, mikä tuntuu rajulta alennukselta (öljyaltistus varmasti suurimpana syynä).

Secure pysynee salkussa, etenkin kun käteistä on kertynyt taas liikaa salkun pohjalle huippuideoita odottamaan. Hiukan uskallan silti toivoa, että tämä ostettaisiin pörssistä pois, jotta yllä mainitusta dilemmasta pääsisi eroon. Ja jos se tapahtuu, niin olen luultavasti pettynyt laatufirman menettämisestä.

Nikotiinifirmat: YTD +35 % (PM) ja +46 % (BTI). Ei mitään toimenpiteitä. Kyseessä ovat salkun kalleimmat positiot, mutta mikäs tässä on niitä holdaillessa. Ensi vuodelle P/E 17 on selkeästi koko salkun painotettua keskiarvoa suolaisempi (2026e P/E 10,8 konsensuksilla), mutta eipä tuo nyt aivan liikaa ole. Kevennellään tarpeen tullen, ja lisätään koriin uusia positioita, jos sopivia tulee vastaan todella edullisesti.

Kanadan öljyfirmat: YTD -5 % (SCR). Strathconan yritys hankkia MEG kaatui lopulta Cenovuksen pokattua pääpalkinnon totaalisen lapasyötön kautta itselleen. On vaikeaa voittaa tarjouskilpailu, jossa kilpaileva taho saa ensin tehdä due diligencet ja sen jälkeen ostokohteelta… noh, erityisluvan, hankkia 10 prosenttia firman osakekannasta markkinasta, kun aiemmin suositeltu tarjous ei mennytkään omistajille läpi. Totaalinen pellesirkus alusta loppuun, ja kuten parille foorumilaiselle olenkin sanonut, niin tämä show yksinään on syy arvottaa koko Kanadan öljy-yhtiösektoria alennuksella muunmaalaisiin verrokkeihinsa.

Strath onnistui kuitenkin pakottamaan Cenovukselta kaksi tarjouksen korotusta, sekä määrättyjen öljyassettien myynnin puoli-ilmaisena Strathconan portfolioon. Vaikka kyse olikin lopulta lohdutuspalkinnosta, niin yhtiölle kävi kuten alun perin oli suunniteltukin: voittaja joka tapauksessa. CEO Waterousin tekeminen vakuuttaa, ja siksi tämä sopii salkkuun kuin nenä päähän. Keskittynyt omistusrakenne (Waterousin rahasto) on yhä ongelma, mutta rahaston suuromistusta on jaettu rahaston sijoittajille Q4:n aikana, ja sama meno jatkunee ensi vuonna. Valoa on siis tunnelin päässä heikosta öljyn hinnasta huolimatta.

Strathin omistajia hellittiin epäonnistuneen tarjouksen myötä kovalla kurssinousulla ja 10 CAD:n lisäosingolla, joka irtosi viikko takaperin - ja samalla se romahdutti salkun tämän vuoden tuottoja reippaalla prosenttiyksiköllä, sillä käteiset tulevat tilille vasta ensi vuoden puolella. Lisää en ole ostamassa, mutta pidän osakkeita mieluusti salkussa ja katson, että mitä Waterous vielä keksii. Muilta osin odottelen parempia alennushintoja ja sitä, että sektorilla alkaa IPCOn ja Strathconan lisäksi muitakin kiinnostaa omistaja-arvon luominen ennen kaikkea muuta.

Vuoden 2022 kauhukabinetin jälkeen sijoitusstrategia meni uusiksi, ja nyt tuloksena uudistustyöstä on kolme peräkkäistä vuotta kaksinumeroisia kokonaistuottoja. Mutta tärkeämpää on tietysti ymmärrys siitä, millaisilla eväillä tuottoihin on päästy / millä eväillä juuri mä voin niihin päästä:

hyvin hoidetut ja johdetut, halvoilla kertoimilla treidaavat arvoyhtiöt,

jotka keskittyvät fiksuihin pääoman allokointipäätöksiin,

osakkeiden takaisinostoihin,

ja kasvattavat seurauksena tulosta, kassavirtoja ja omistaja-arvoa.

Tällä hetkellä lähes koko salkku edustaa juuri tuota sapluunaa, ehkä nikotiiniyhtiöitä lukuun ottamatta. Salkku on tylsä kuin mikä, mutta firmat tekevät mun silmissä järkeviä asioita, ja se riittää mulle. Myös 10 position hajautus + iso käteiskassa on rakenteena OK, ja tuskin tulen kauheasti sitä muuttamaan suuntaan tai toiseen tuosta.

Vuoden 2024 lopulla toivoin tälle vuodelle 5-10 prosentin tuottoa, ja noin kahteentoista päästiin - tämä siitä huolimatta, että valuuttakurssien muutoksista tuli turpaan useamman prosenttiyksikön verran. Suoritus lämmittää mieltä, vaikka varmasti enemmänkin tuottoja oli otettavissa.

Ensi vuotta ajatellen olen melko luottavainen: Fairfax ja Linamar, salkun kärkihevoset, ovat iskussa ja kykenevät varmasti merkittävän positiiviseen tulokseen. Kysymyksiä herättävät enemmän osasto AerCap/Secure/nikotiini, jossa arvostukset ovat kireämpiä ja odotukset kovempia jo valmiiksi. Tavoitteena on kuitenkin jatkaa kaksinumeroisten tuottoprosenttien putkea, ja vaikka pörssit ovatkin jo lähtökohtaisesti korkealla, niin pidän tavoitetta täysin realistisena omia salkkuyhtiöitä katsellessa.

Hyvää ja rahakasta uutta pörssivuotta 2026 koko foorumille!

Let’s start the end-of-year review with the easiest part: the portfolio contents. Investment level 222% after a small upward spurt during the last trading week of the year.

New year, new joke. Heh heh… I thought I’d move out of my comfort zone and keep a proper record of all the tinkering I do and what kind of mistakes I make during the year. I’ll try to share all the changes here about every 4 months and keep track of what’s been done I have a habit of getting jittery and FOMOing quite a bit, and that’s where I’ve made my biggest mistakes in recent years. Hopefully, this record-keeping will calm those tendencies. I apologize in advance.

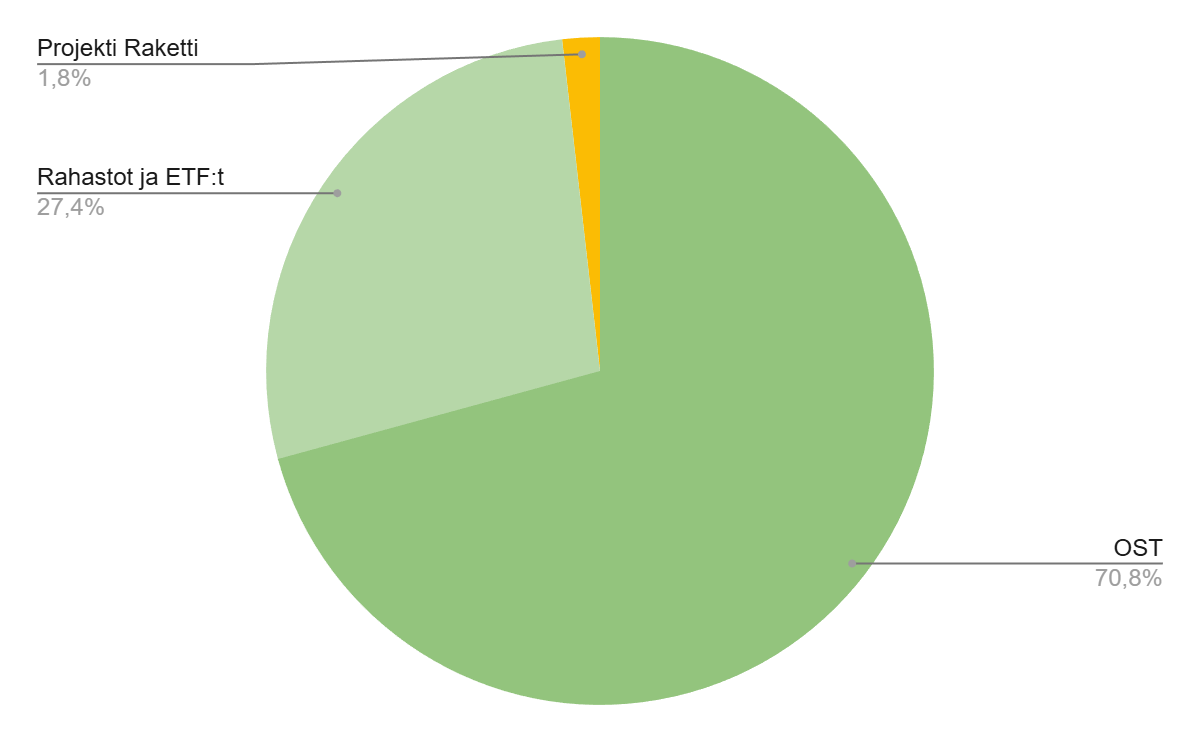

OST (Equity Savings Account) portfolio. Established March 25, 2020. The idea is to accumulate dividend stocks here and do some quick trades with stocks where I have some kind of view or hope regarding the price. The 100K deposit limit for the account was reached on October 31, 2025. I’ve been aggressively saving everything extra to reach this goal.

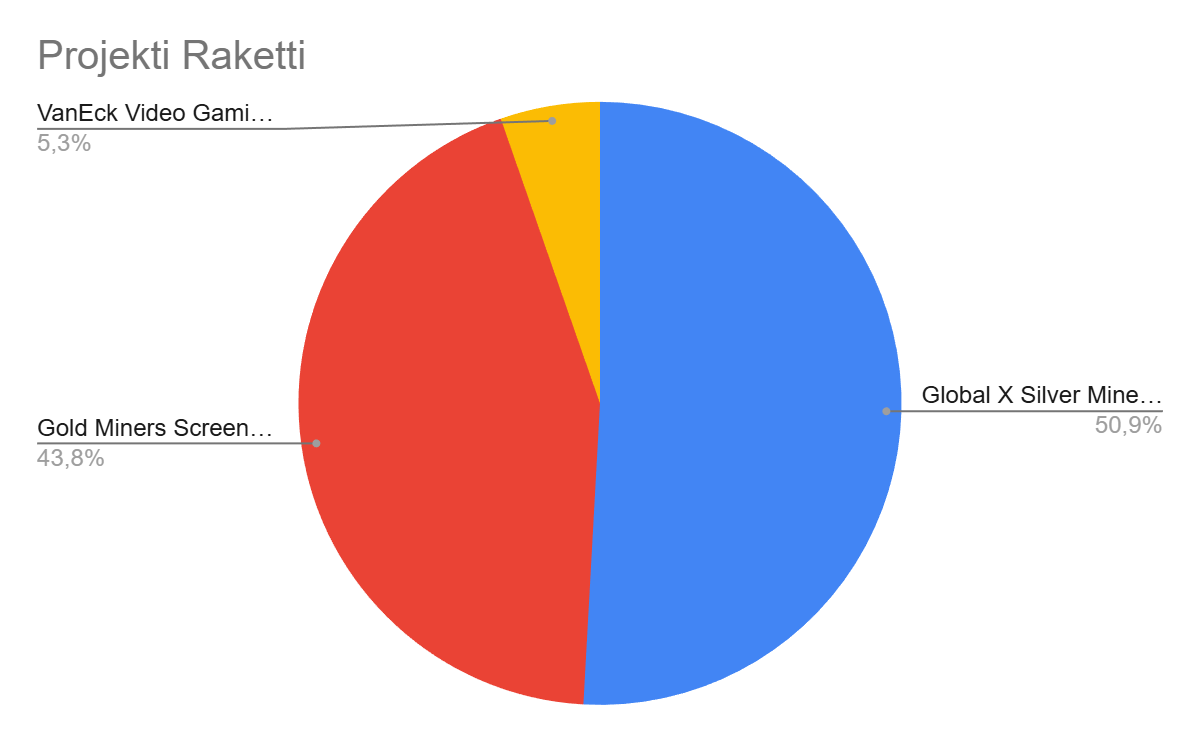

As a new portfolio, I set up the “Project Rocket” portfolio. Established October 1, 2025. Let’s hope this one really rockets. The idea is that I’ll also start buying foreign stocks here, because right now the weight is heavily on Finland. Metals were the first to find their way into the portfolio. I’m growing this portfolio aggressively now to get more diversification.

Then the big picture. The OST has grown really large. Thanks to the strict savings regime of recent years. I wouldn’t have believed I’d get it together this fast myself.

Cash/fixed income investments 19.6 %.

Funds and ETFs (Seligson, Pyn Elite, Splitan, EUNL, EUNK, IUSN, IS3N, Seligson & Co OMX Helsinki 25, XACT Norden) 26.8%

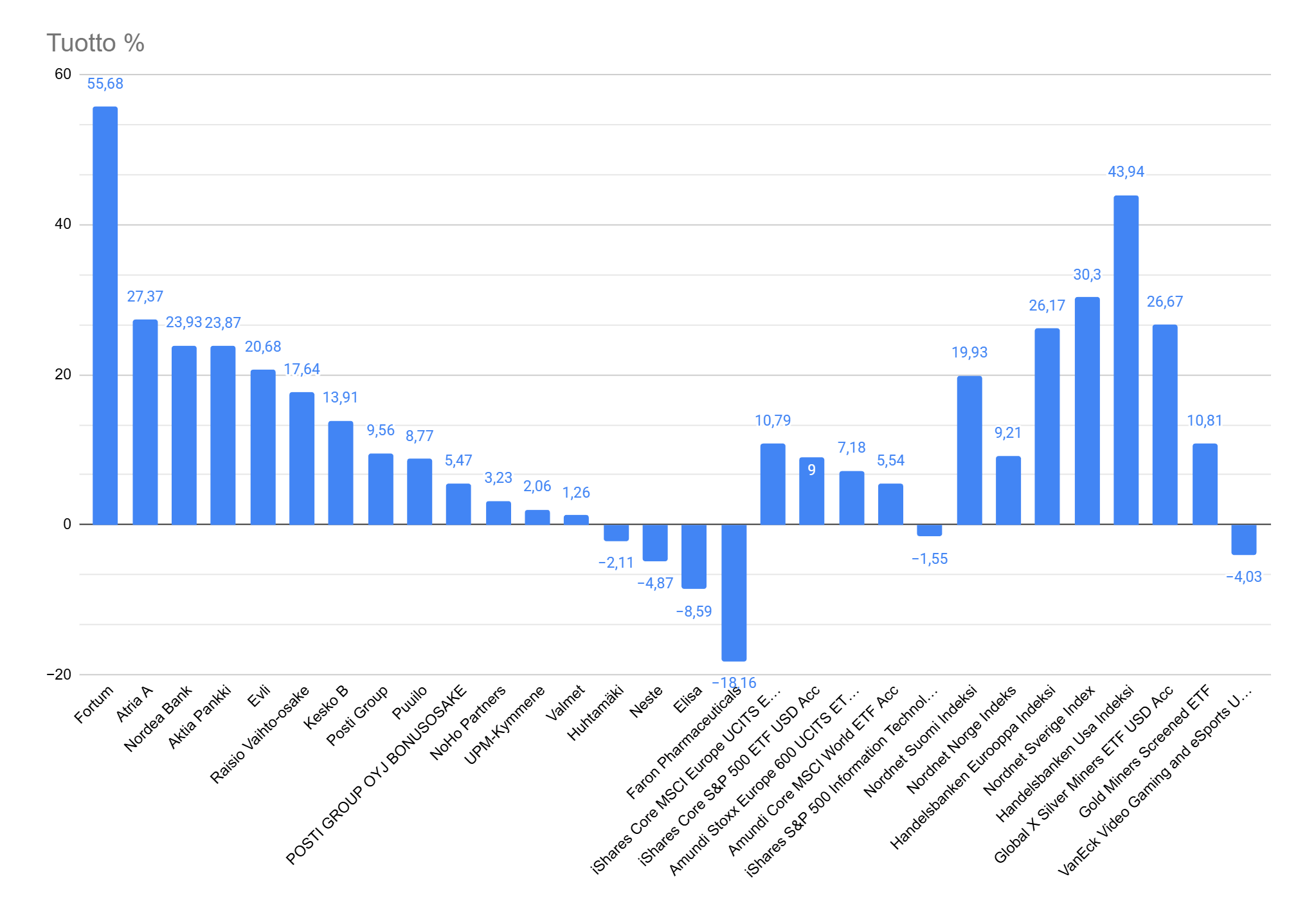

New additions to the portfolio: Elisa, Huhtamäki, Adobe, Noho

Additions: Vaisala, ADP, Evo

Sold: Talenom, Framery

Trims: Qt, Tieto

Short trades: -

Share issues: Framery

My investment strategy has changed slightly over the past couple of years. Two years ago, I began increasing the weight of ETFs and funds in my portfolio. During this time, their share has grown from 10 percent to nearly 27 percent. I intend to continue increasing this share further.

In the longer term, my goal is also to reduce the number of direct stock positions. I also intend to keep position sizes slightly smaller in the future.

For various reasons, the share of Finnish small and mid-cap “home field advantage” companies in the portfolio has decreased. A few companies are still waiting at the starting gate, but in this market situation, it’s not necessarily worth hitting the submit button just yet.

Increasing the share of funds and ETFs has led to a small problem in my equity savings account (osakesäästötili) in the form of accumulated excess cash. You don’t get any interest on cash there. Because of this, I will continue to invest small amounts in companies I might not otherwise invest in. This quarter, the companies falling into this category were: Elisa, Huhtamäki, Adobe, and Noho. It has been on my wish list for a long time that legislation would change so that other investments besides direct stock investments would be allowed in equity savings accounts. This change would be timely for my portfolio as well. I would very gladly replace these small positions with a suitable ETF.

I reduced my position in Qt during the quarter. The company’s recent quarters have been somewhat weak. I was expecting a more positive surprise in the form of delayed deals materializing. The surprise was anything but. I was left wondering if Qt’s competitive advantages have begun to erode, especially in the automotive sector. I will continue to monitor the situation through the company’s Q4 report and perhaps Q1. The company might even face a sudden exit from the portfolio if the direction doesn’t change. My intention is to emphasize quality companies in my portfolio going forward. With high-quality companies that possess (ideally) sustainable competitive advantages, one shouldn’t have to ponder these kinds of issues.

Talenom was finally sold off entirely. It has been painful to follow the company’s development, and I’ve received several cuts from falling knives. Expanding into the first foreign market proved to be a stumbling block for the company, and during 2025 Q3, the last remnants of the facade seemed to collapse. Although the Finnish operations have proven quite profitable, growth hasn’t really carried over here either, considering the market situation. The company’s management no longer inspires confidence, and the balance sheet is what it is. The dividend policy has been strange for a company seeking high growth. Capitalizations on the balance sheet aren’t to my taste either. In my opinion, I have often succeeded in getting rid of companies in my portfolio that I haven’t really missed later. The problem, however, has often been that I’ve woken up to the companies’ weaknesses far too late, which may have caused significant dents in the portfolio’s returns.

I’ve been doing passive investing for about five years now—mostly because it’s supposedly trendy and profitable in the long run. This has also become my own mantra and strategy: buy in a diversified way, don’t worry about daily or weekly fluctuations, and encourage loved ones to do the same.

Now, however, after about five years, the whole thing has started to feel a bit boring. Not because there’s no logic to it, but because my role is mainly just ensuring that on a certain day each month, there’s enough money in the bank account for the automated transfer and purchase process.

Since I started from zero, the portfolio has only grown to a value of a few tens of thousands, so there’s still a long way to go before I can live the life of a “gentleman of leisure.” The portfolio’s contents are roughly 2/3 low-cost funds, diversified geographically and by sector. 1/3 is individual stocks.

In terms of stocks, I’ve held Nordea for a few years from around the €9 mark and Smart Eye from the 40 SEK level. The idea with these, so far, has been that it’s nice to have at least one pillar (Nordea) and one innovative technology company whose business (and product) use case is straightforward enough to explain to my own parents.

I started thinking about how I could get that spark back from the “corona fever” days of investing. Can I make my approach active instead of passive? I recognize and am aware that I don’t have the patience to dive deep enough into investment terminology, market dynamics, or especially company financial figures. Because of this, I need to come up with a new strategy and a way to involve myself and my thoughts in investment decisions.

I consider myself a logic-driven person: I (often, though not always) need a cause and effect for many things and events. From this, I reasoned that I would start looking for and identifying event points in the future. Yeah, if only I had a crystal ball.

Many would probably call this normal “market sensing and interpretation,” but for me, the idea is more on the side of common sense. When certain things happen, they usually set off some kind of cycle (a “domino effect”). When you catch onto that cycle and have a dash of luck involved, it provides enough fuel for potential success in terms of returns.

In my view, the next significant event is, naturally, the end of the war in Europe. The war itself has pumped the valuations of defense sector players through the roof—meaning that train has already left the station in terms of returns. But more than just weapons and bombs will be needed.

Based on this “brilliance,” I decided to use the money I had stashed away to top up my portfolio (in addition to current holdings) with:

ETF: Global X European Infrastructure Development

Contains many European construction-related companies. A large portion of the companies are from countries that have actively supported Ukraine both publicly and financially during the war. I trust (bet) that these actions will also secure a ticket into the reconstruction value chain.

Stock: Finnair

Heh. Is there a more uncertain industry than air travel? Finnair has taken quite a beating due to the war. I trust that (when) peace is achieved, Finnair will correct significantly upward. However, I don’t believe this will stay in my portfolio for long. Probably the first one to go.

Stock: YIT

Someone has to take overall responsibility for private and public construction projects, right? I’m speculating that YIT will rise from this slump when the time comes. It might take a long time; I’m in no hurry. The same applies broadly to the entire construction sector; YIT is no exception in itself.

Stock: Arcelor Mittal

A steel company that has already front-run quite a bit and has also invested in a production facility located in Ukraine. Local steel will surely be of interest during the reconstruction phase. Let’s see and hope for the best.

In addition, I’m still looking for stocks related to the energy sector as well as service and restaurant operations, but research on these is still ongoing. And of course, tech companies are always interesting—as long as they aren’t some AI mumbo-jumbo.

Many of these hit the stock exchange, but then again, I feel they are easier to follow. Time will tell if I’ll venture further outside my home country. It’s easier to add salt than to remove it

I’m heading into 2026 with a fairly open mind and a messy portfolio. But above all, based on gut feeling and occasionally even bold vision.

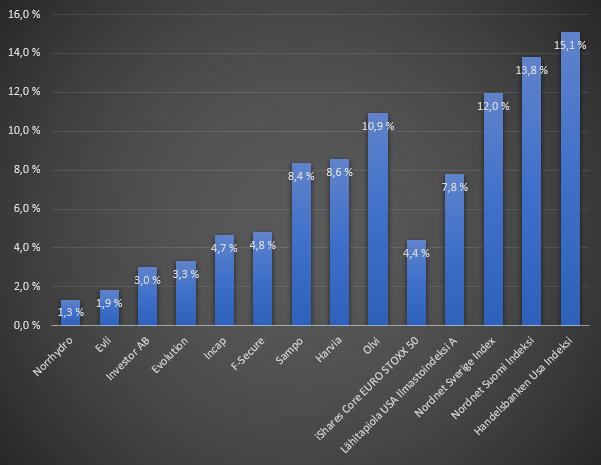

The goal for 2024 and 2025 was to increase stock picking outside of the Helsinki Stock Exchange. In the context of Trump’s tariff policies, I realized that evaluating foreign companies combined with massive price fluctuations does not suit me after all; Applied Materials and Brown-Forman had to go. I am diversifying outside of the Helsinki exchange by increasing the weight of US funds and gradually adding Investor AB and the EuroStoxx 50 index.

Overall, I am still satisfied with the portfolio structure. The weighting of funds/ETFs can increase to ~60-70%, with the remainder in 5-10 individual stocks.

My biggest investment mistake, Kamux, was finally removed from the portfolio. Evolution is now under review—are we stepping into the same minefield of setbacks and excuses as with Kamux, or will we see a positive turnaround?

Wishing you a good and successful investment year 2026!

During the latter part of the year, stock purchases continued, but some reductions and sales were also made. Fund and ETF purchases have also proceeded as usual on a monthly basis.

New to the portfolio:

Huhtamäki, Elisa

Additions:

Nordea, Kesko, QT, Harvia

Reductions:

Nokian Renkaat, Kalmar, Alphabet, Berkshire Hathaway, Neste,

Sales:

Fortum

I sold my Nike shares but bought them back later in the year during the price dip.

The portfolio return was approx. 24% in 2025, which is reasonable. Lower returns came from funds and ETFs with a high US weighting due to the exchange rate.

In 2026, the intention is to initially monitor the market a bit and accumulate cash, while continuing regular monthly ETF and fund purchases.

2025 was a “gap year” in the sense that I didn’t lose tens of thousands of euros to the world index. Finally, even the (nominal) net worth of 2021 has been exceeded. In between, quite a lot of losses were made with domestic small-cap companies. Many on the forum, or at least a few smart people, did warn with good reasoning about the small-cap bubble back then.

All kinds of mistakes can be made in stock investing. Significant ones for me include thesis creep and burying my head in the sand. However, I haven’t generally clung to falling knives by increasing my stakes. This “success” is probably, for many tickers, a result of a lack of original investment thesis and conviction. With domestic companies, there has perhaps still been a tendency to hope for a turnaround through patriotic lenses. With foreign ones, such nonsense doesn’t interfere with my thoughts.

I have consciously tried to slow down decision-making, which may be good in the long run, but as a result, there are still useless lines hanging in the portfolio. I have let go of my mistakes slowly—too slowly in terms of returns. A large part of those bought as replacements (or additions) have succeeded quite well, but chance largely defines that in the short term. Perhaps the further erosion of self-confidence in my own stock picking has partly slowed down decision-making.

According to plan, regarding listed holdings, the shift outside of Finland has been slowly continued. If unlisted ones are included, the domestic market weight is now about 50%. Regarding the performance of unlisted companies, I can be satisfied, even though the market conditions have offered headwinds. Their valuation is conservative, but they are small enough in size that the final exit could be 0 euros. For now, however, things seem to be going okay, and maybe in a few years, allocation decisions will need to be made. There is still time to mull over my attitude towards fixed-income investments too.

Despite the somber tone of the text, the interest in learning new things about both investing and self-knowledge is at an ATH.

Thanks to the whole community and especially thanks to the first-class moderation!

Wishing you all the best and most profitable investment year 2026!

First post in this thread about a hobby that started in the fall of 2022.

Returns haven’t been very good, especially due to constant changes of heart regarding investment targets in the beginning, but at least the hobby has brought some meaning to my life

And after all, it’s not really a hobby if it doesn’t take all your money.

New year, new identity. Ziiba was too boring and didn’t highlight my love for dividends enough.

The portfolio also underwent a major overhaul in 2025. It still contains the same 6 ETF monstrosities, but most of my 26 stocks are brand new or at least returning ones. ETFs weight 56.33% of my portfolio, and direct stocks account for the remaining 43.67%.

I started investing in the summer of 2023, and 2024 in particular was a miserable performance in terms of stock picking. If I remember correctly, the Equity Savings Account (OST) was still about 6% in the red in January 2025, and at that time, I was thinking how great it would be if I could manage to break even this year.

But then things started happening: In the spring of 2025, a certain liquid knife stopped falling. In the autumn, Fortum was realized to be an AI stock, and Outokumpu was… a defense stock, I guess? Well, they all rose anyway, and I trimmed my positions in each. But my new stock picks performed perhaps even better: strong returns were delivered by, among others, Enersense (80%), Tekova (64%), and Citycon (24% with only just over a month’s holding).

At the end of a fantastic investment year, the OST was actually over 31% in the black! There was much more luck than skill involved, but I am really happy.

With this portfolio, it’s good to head towards the adventures of the 2026 stock market year.

Pharming (21.1%) – Joenja case: patient discovery, reimbursement/accessibility, geo-expansion, and potential label/indication expansions could grow the scale to a whole new level; Ruconest provides support, but as I understand it, the company will invest in growth for some time.

Biohit (17.2%) – Hit indeed, it has been improving its numbers for several years now, and mass screenings would be the rocket catalyst that changes the scale, but the base case doesn’t rely on that alone.

Novo Nordisk B (12.3%) – Portfolio anchor: high-quality business and strong cash-generating ability balance out riskier holdings, and if demand + capacity expansion stay under control, the premium may return.

Diamyd (12.1%) – Binary catalyst play: if the DIAGNODE-3 data hits, the revaluation could be aggressive; if not, the story stalls.

Evolution (10.5%) – The price drop improved the r/r, although regulatory risk is always present, and at the same time, trackers show the games reaching new ATHs (e.g., at Christmas). If the regulatory fog doesn’t worsen and the numbers hold, the king could get king-level pricing again.

Smart Eye (9.6%) – Hockey stick case: in my opinion, we are right at the shaft/inflection point where OEM volumes start to properly show up in revenue and scaling kicks off. If the stick turns, the leverage is brutal.

Magnora (8.9%) – I think a massive number of milestone payments are coming, and the market doesn’t realize how much money could come in even in the short term through multiple hits. This is the “underpriced cash flow option” slot. This is the stock among these that I’d still like to buy significantly more of before it takes off to the skies.

Lindex (3.8%) – The sale of Stockmann/structural cleanup is a clear catalyst: uncertainty fades, the story becomes clearer, and multiples can move.

Multitude (2.9%) – I’m not fully deep into the case yet, but a quick DD gave the feeling that the valuation could easily be several times higher if the numbers hold and suspicion fades. Therefore, a small weight, more depth later.

OMS Energy Tech (1.5%) – Same: a light DD was enough for now, and the upside looks like a multi-bagger if the execution hits, so I’m in with a small option. Small weight because I haven’t “nailed” every angle of the case yet.

Oh yeah, and in addition to these, of course, a certain pot in junk bonds and various hyped unlisted stocks.

Let’s record for myself how the investments look at the start of 2026, as I started investing for the first time last January; cashed out my ASP (home savings) account and put everything into an ESA (Equity Savings Account), which currently only allows for buying Finnish stocks. However, I added physical gold and silver to the same table, as I bought them alongside these at roughly the same time.

I more or less started with the idea that the portfolio size should be about 7-10 stocks, in which I initially invest roughly the same amount. The only exception was Neste, which managed to drop significantly lower after January and is therefore (+ good return %) clearly the largest weight in the portfolio.

I already knew that I didn’t want to start active trading (veivaamaan), and the few trades of the year have confirmed this view … result: nothing but bad moves:

the portfolio previously included Nokian Tyres (Rinkulat), which I bought at the end of January, and the price dropped ~20% just two days later… After that, there was a long period of languishing (mörnimistä) as a red line in the portfolio - I sold these at break-even (kuivin jaloin) at the end of October, but apparently, I should have left them in the portfolio.

SOSI1: I bought this with roughly the same 8% weight in the portfolio at the end of January at .092e/share and let go of them after what looked like “constant bad news” again at roughly the purchase price at the end of July… and everyone knows what would have happened to these shares (lappusille) if I had just let them stay in the portfolio until now - well, I try not to look at the stock prices at this stage and take some comfort in the fact that I am still involved in silver’s development with a 6.6% weight in physical ownership.

–> these two were replaced by Terveystalo and Kemira, clearly worse options at least looking at it now. However, I believe in both in the long term.

share of investments %

return %

Neste Corporation

19.0

66.8

Nexstim Oyj

10.7

72.2

Fortum Corporation

9.9

38.0

Gold

9.0

44.1

Terveystalo Plc

8.5

2.5

Herantis Pharma Oyj

8.1

58.2

METSO OYJ

7.4

55.1

Mandatum Oyj

7.1

47.5

Nordea Bank Abp

7.0

41.6

Kemira Oyj

6.8

0.1

Silver

6.6

106.5

There isn’t much to explain about the portfolio as such, except perhaps too much weight on the healthcare sector. In the beginning, I wondered if I should go with Faron & Nightingale instead of Nexstim and Herantis, but I ended up “supporting” brain research & imaging. Terveystalo indeed joined the portfolio later, as I reflected on the state and future of public healthcare in late autumn.

Alongside a few slightly disappointing trades, I must say that I entered the (Finnish) market at a great time for me and overall the investments performed very well, especially considering I don’t really know anything about investing

The few dividend pennies that have managed to come in have been reinvested into Herantis on top of the old ones.

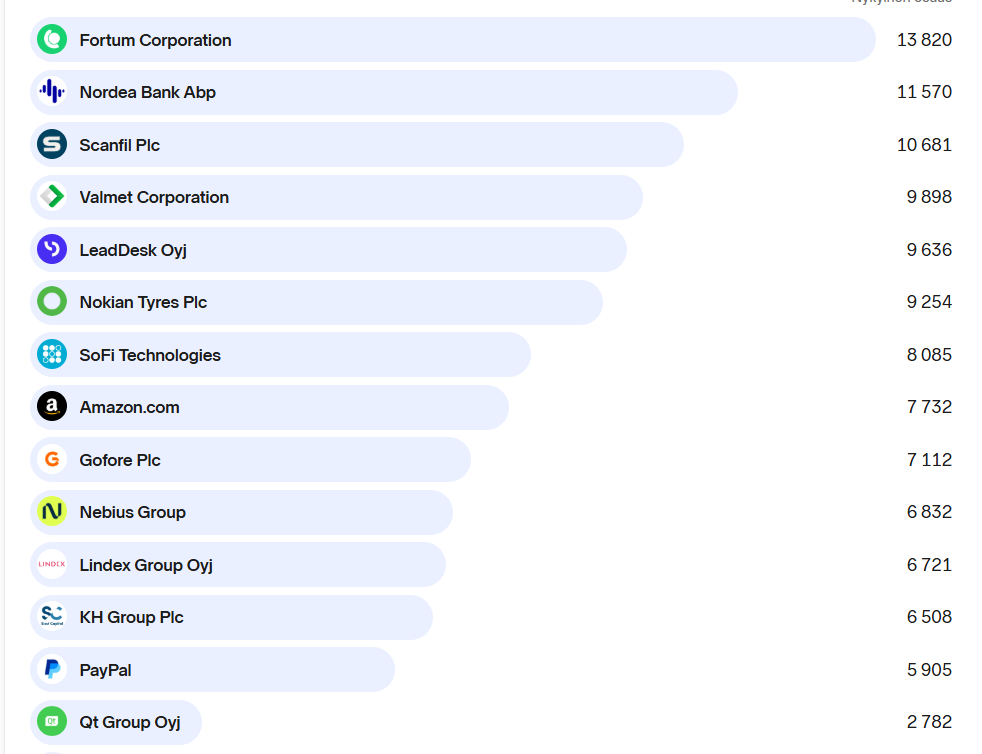

My portfolio hasn’t changed much since the fall of 2024; sometime in November 2024, I added more Valmet and Scanfil on top of my existing holdings.

Last year, i.e., 2025, I bought Nebius and SoFi for my portfolio.

Mainly for psychological reasons, I paid off the rest of my mortgage last year, which explains why more money didn’t flow into stocks.

I didn’t actually sell or reduce anything, because after some reflection and research, I didn’t feel the need—well, there would have been a need, as my portfolio lagged the benchmark index by well over 30 percent. If I had bought more last year, that money would likely have gone, at least for the most part, into companies already in the portfolio.

I have commented on each of these companies several times and don’t really have much more to say about them. I have, from time to time, gone through the companies in my portfolio individually, reflecting on their significance in my own holdings.

PYN Elite

I still hold PYN Elite, which I have indeed added to a few times since the initial purchase. It’s been a bit of a poor investment so far, barely in the green.

Crypto portfolio

Nicely in the red, about one percent of my total wealth.