It’s time for another small portfolio review. No dramatic changes have occurred in the portfolio since the last review, but I wrote a “Kill your darlings” (freely translated as “kill your best ideas”) memo for myself in the spirit of Charlie Munger, and why not share these thoughts for others’ enjoyment.

The idea is specifically to destroy my own positions, so the writings are intentionally negative. Nevertheless, in many cases, I will elaborate on the core business idea to refresh my own understanding and for the reader’s enjoyment.

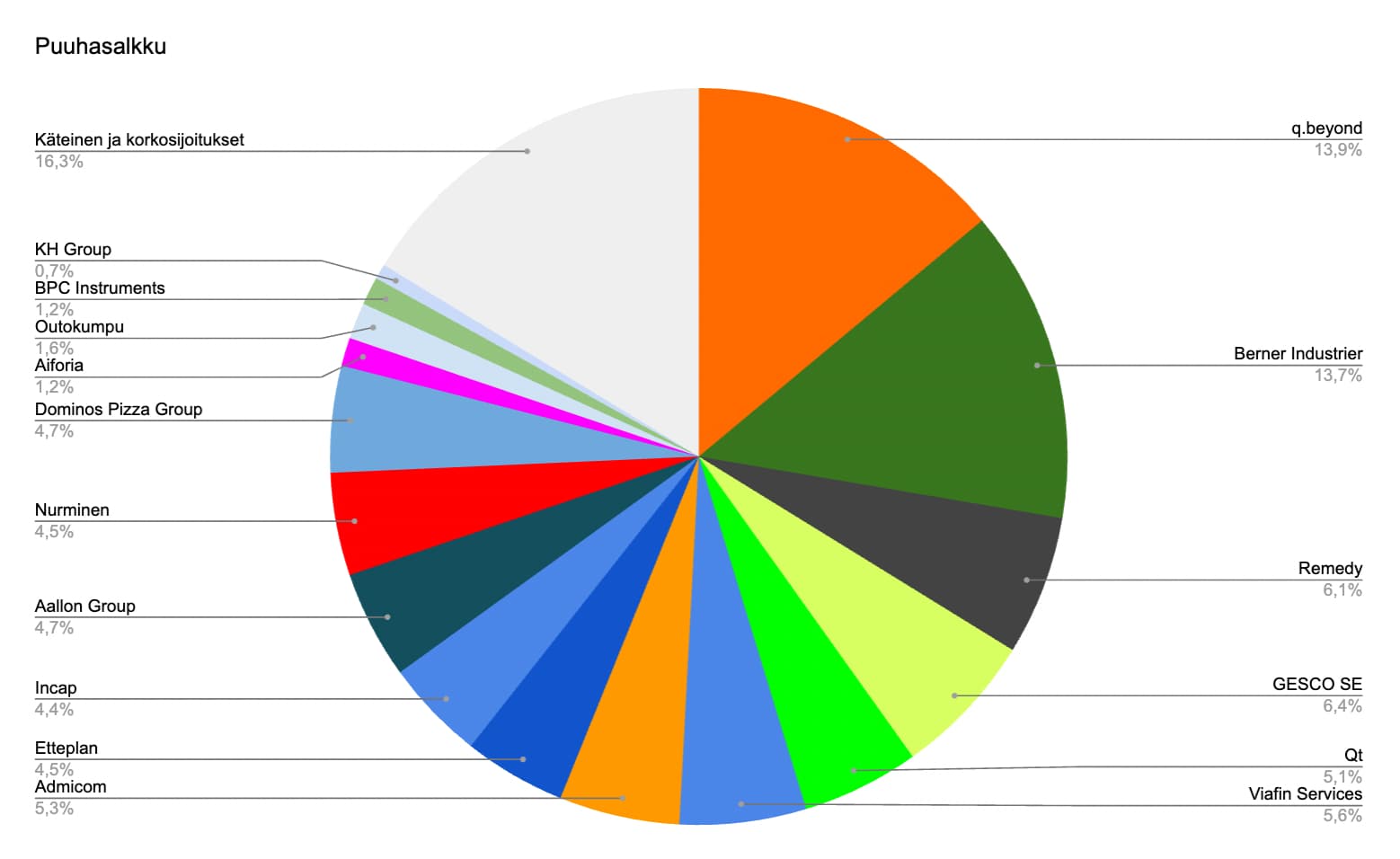

“Kill your darlings” -memo

q.beyond AG is a German IT service company in the midst of a profitability improvement, with its own data centers and a solid net cash position. The stock looks dirt cheap, EV/S 0.4x, but companies in the sector are generally inexpensive anyway. That’s briefly about the good points. The company’s historical track record of profitability is non-existent, data centers are operating at undercapacity, and sector profitability in Germany is poor anyway. Germany’s stimulus package and digitalization needs are not materializing, however, because Germany is what social philosopher Seppo Räty wisely said it is. The company’s investment in cybersecurity monitoring centers also sounds timely, but I remember from Nixu that it’s not exactly a gold mine when guys are staring at monitors with hamburgers in hand.

Berner Industrier AB is a Swedish serial acquirer that has made significant progress in its profitability turnaround. The stock has received the multiples (TTM P/E 36x) and label of a high-quality serial acquirer, even though only one acquisition has been made during the current CEO’s tenure (even if he has a Lagercrantz background) and the profitability turnaround has not yet been definitively proven.

GESCO SE is a German interpretation of a serial acquirer. The company’s historical track record of profitability is highly variable, and its largest business, tool steel wholesaler Doerrenberg, drags the entire group down like a heavy anchor in a weak economic climate. P/B 0.5x looks cheap, but why pay more when returns on capital are abysmal. The new CEO only talks about lean management and improving profitability, but usually, the company’s reputation remains while the management’s reputation is tarnished in turnaround cases! A strong balance sheet is of no use if money flows back into weak businesses.

Remedy is an Espoo-based small-budget triple-A game studio, whose recent track record is mixed. The critical success of Alan Wake II cannot buy food from the store when commercial success is still pending. To top it all off, 30 MEUR was invested in the co-op game Firebreak (a shoemaker should stick to his last). Risks are accumulating disproportionately on the shoulders of the next release, Control II.

Viafin is an industrial maintenance service company whose rapid historical growth is no guarantee of future growth in a sluggish Finnish economy. Cheap acquisitions offer no comfort when the profitability of the acquired targets disappears into the overall mediocre profitability. And why would anyone be interested in owning Viafin, even if it’s available at EV/EBIT 10x.

Qt Group is a Finnish technology company with historical hype and growth, which has recently hit a snag. The serial negator trades at EV/EBIT 17x based on this year’s forecasts, but why trust the future when the company has mostly delivered negative surprises in recent years? Successes in a few previous acquisitions have compensated for the slowdown in core product growth, but success in those does not guarantee success in the latest acquisition. It’s not easy for software companies to transform into multi-tool software portfolio companies.

Admicom is a Finnish construction software company, but why would the company grow when there’s no end in sight to the construction industry recession? Without growth, it’s difficult to create value. In this sense, an EV/EBIT of 18x based on this year’s forecasts feels uninteresting. And will AI eat software companies in the long run?

Etteplan… Why would anyone be interested in a rather dry engineering firm burdened by the general economy, even if the price tag were around 10x EBIT with normalized profitability? When there’s no growth, pricing inevitably gravitates towards basic multiples, which are around 10 for normal companies.

Dominos Pizza Group is a British master franchise company operating the Domino’s brand in the Isles. The company’s earnings have not grown for years, and it’s difficult to improve on a market share of over 50%. Although the stock trades at approximately P/E 10x based on near-term forecasts and has a dividend yield of over 5%, drivers for further growth are missing in the challenging British economy. To top it all off, the company threatens to pour its abundant cash flow into another brand, where it will surely fail!

Aallon Group is a Finnish serial acquirer of accounting firms. Organizational restructuring means an increased risk level in a people-centric business, and the sector as a whole isn’t growing tremendously. A P/E of 12 based on current year forecasts might seem cheap, but who thinks about valuation in times like these! Consolidating accounting firms is fashionable nowadays, and prices are surely about to skyrocket, which will derail the profitability of inorganic growth.

BPC Instruments is a Swedish bio-sector measurement instrument company. Some investors might find a 90% market share in such a growing niche sector very interesting, but all positive attributes are overshadowed by the CEO’s 60% ownership stake in a tiny company. Can we trust him? Successes are already priced into the stock as it trades at P/E 27x.

Aiforia is a Finnish AI company that enhances the work of pathologists. A great idea, but press releases alone don’t put bread on the owner’s table!

Nurminen Logistics. A P/E of 9x is not a cheap valuation for a relatively scalable and moderately capital-intensive business, because the current earnings level is partly based on the company’s exclusive lucrative contract to transport so-called strategic fertilizers from the eastern border. How long will this last?

Incap. This electronics contract manufacturer may have proven in recent years that it possesses genuine sustainable cost competitive advantages thanks to its agile and lean organization. But the largest customer still brings a huge slice of the bread to the table. Owning Incap is like participating in a vodka shot competition for pyromaniacs in a dynamite storage facility.

Cash Position. Why hold cash when American stock markets rise every day? Every day, new meme stocks and meme coins offer an opportunity for quick enrichment, which only a wimp like me, who fails to grasp the bigger developments, would miss out on. Perhaps you hold them in a short-term interest fund and earn interest income, but that pales in comparison to the hourly returns of cryptocurrencies.

Finally, I could shoot down the entire portfolio. I have clearly emphasized cheap valuations and turnaround cases in my stock picks across Europe. Most companies also need top-line growth for that. Their industries are such that without an upturn in economic growth, it’s difficult to achieve it. If it doesn’t come, the stocks will languish. Patience is a virtue.

Turnaround companies also have a bad habit of relapsing, so with such a portfolio, one constantly has to actively seek new targets and patch up old holes. This is probably what it feels like if you owned a dilapidated detached house! When the roof is repaired, the end wall collapses onto the carport.Normally, a more suitable style, which I have historically practiced, is to sit tight on excellent companies. Many excellent Finnish companies have become a