It was wonderful to find L’Oréal’s initiation here. Thank you for that!

I strongly believe that as the world reopens, luxury brands, in particular, will increase their sales.

During the pandemic, parties have been missed, and people have saved money. It’s time to invest. We’ve seen indications of this, for example, in this earnings season, where the earnings growth of retail stocks has been inconsistent. For example, Stockmann, which focuses on women, increased its earnings.

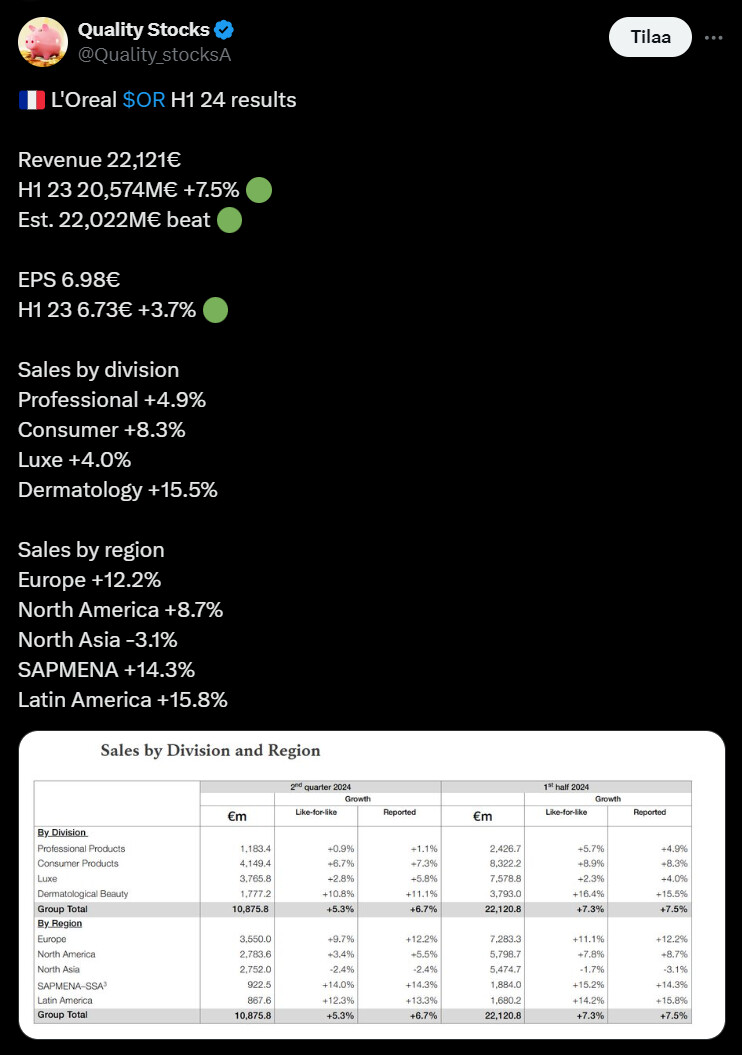

L’Oréal reported an 18.0% increase in earnings compared to the reference period. While the reference period wasn’t particularly strong, growth was also achieved (+9.3%) compared to pre-pandemic Q3 2019.

I assume that many on this forum are not familiar with L’Oréal’s brands and market position as such. I could elaborate on this a bit. Why? To help understand why I believe we can see growth, for example, over a year-long period.

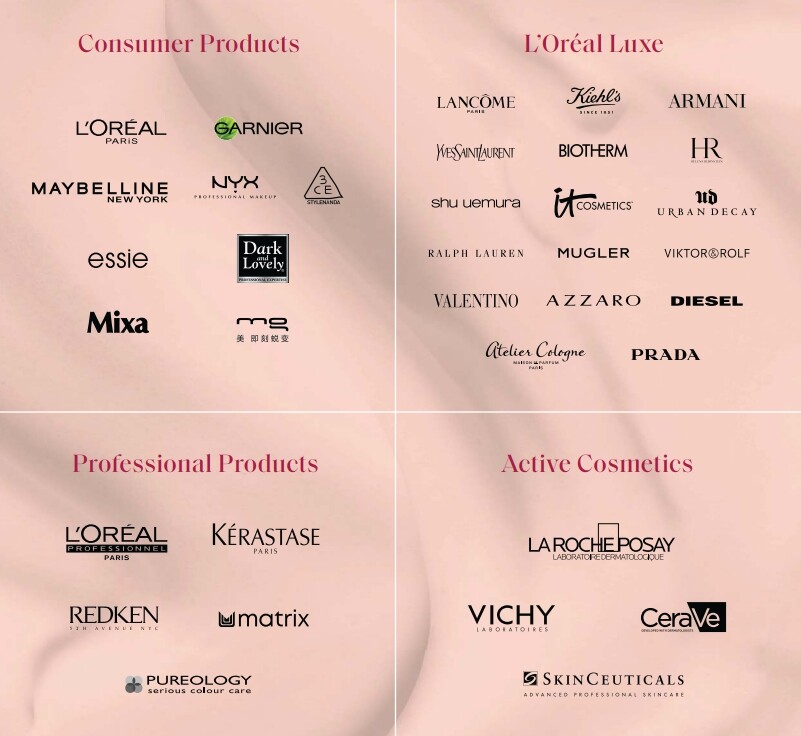

Firstly, typically, products from all divisions include skincare and cleansing products, makeup, hair cleansing, treatment, and coloring products.

While I mainly talk about women, there are, of course, products for men too. Women are just the biggest consumers, at least for now.

Previously, products from a specific division were found targeted at certain points of sale, but I have noticed that it seems to be the norm now that products from all divisions are sold mixed together. In other words, you can find everything in supermarkets today. But to clarify the typical potential buyer, I’ll go through the old sales channels.

L’Oréal Luxe

All the L’Oréal Teams around the world are committed to create the best of Conscious Luxury

L’Oréal Luxe products include brands that are branded as products worth paying more for. Perfumes, for example, remain usable longer compared to consumer products due to the raw materials used and the history associated with perfumes. Biotherm’s facial cleansers are said to keep the skin younger for longer. Yves Saint Laurent eyeshadows are said to contain more color pigment. IT Cosmetics, because you only have one skin.

Luxe products are therefore for those moments when you want to treat yourself, pamper a loved one, or yourself. Typical places to buy Luxe products are specialized cosmetic stores like Kicks, Stockmann, or ship or airport stores.

Parties and travel increase the demand for Luxe products in the form of souvenirs.

Sales increased by 25.4%, and compared to Q3 2019, growth was as high as 13.3%. Was there pent-up demand visible in Q3, or were they stealing a competitor’s market share? I don’t know. Time will tell.

L’Oréal Consumer Products

Because, we are all worth it.

As long as I can remember, L’Oréal’s consumer products have encouraged women who consider themselves ordinary to take care of themselves. Consumer products are for everyday makeup, and when you don’t feel the need to pay extra for your makeup. “Value investor’s makeup.”

Many of us also have a small artist inside, and the affordable price also encourages us to try new things ourselves. Supermarket hair dyes are perfect for satisfying a hair coloring addiction.

Typically, the makeup and skincare products located near the entrance of supermarkets trigger my shopping urge. If I don’t deliberately avoid the aisle, I easily pick up something. I don’t think I’m the only one.

I took a longer look at the list of brands for once, and it’s quite surprising how large a portion of my local supermarket’s cosmetics section they fill. I should check it Lynch-style, but off the cuff, it might very well approach half.

Sales increased by +5.2% and exceeded the 2019 reference period. This division therefore saw the most moderate increase.

L’Oréal Professional Products

Hairdressing is an art form. We won’t mass produce hairstyles. Hairdressers, their expertise, will always play a role. L’Oréal is entirely at their service.

Products from the Professional division were previously typically sold in hair salons and at wholesale suppliers for hair salons. Hairdressing students are subtly brainwashed during their studies about the excellence of certain brands’ product development, and L’Oréal’s products are increasingly seen as industry leaders. Company representatives visit schools during studies to talk about the products and their chemistry. The products are used for practicing coloring on others and are favored in everyday life. Upon graduation, students pass on this knowledge to their clients, and as industry professionals, their information is trusted.

Previously, hairdressers tried to sell their customers products that could not be obtained elsewhere, but I believe this has changed. First, professional hair care products began appearing, for example, at Stockmann. Stockmann was allowed to sell the products because a hair salon operated on its premises. When, for example, Tigi (not a L’Oréal product) first put its products on sale in supermarkets, many hair salons removed Tigi from their selection. Nowadays, it’s a pleasure to see that L’Oréal’s Professional products like Redken and L’Oréal in Paris are actively used by hairdressers and found on supermarket shelves.

In Q3 2021, sales grew by 22.5% compared to Q3 2019.

L’Oréal Active Cosmetics Division

Adding Health to Beauty

Many women are not particularly keen on using chemicals for beauty care and are cautious about them. There are also many women who have allergies or particularly dry or atopic skin and cannot use ordinary products.

Active Cosmetics is probably the only division whose products I’m not very familiar with. For a long time, they were mainly found on pharmacy shelves. Now I’ve spotted them everywhere else, and in some stores, they are categorized under natural cosmetics. I don’t know if it’s just what the papers are writing or if young people are interested in natural cosmetics? For a thirty-something like me, natural cosmetics mean The Body Shop, but is there room for growth here? The Body Shop’s products are ridiculously expensive. To be honest, the color palette of these products doesn’t necessarily suggest that they will become lasting favorites among young people, at least not yet. Perhaps a new brand could emerge here, as the company has expertise.

The division saw growth of 34.5%, and the Q3 results stated that growth was continuing.

On September 20, Henkel, L’Oréal, LVMH, Natura &Co, and Unilever announced their intentions to develop a scoring system that allows consumers to compare the environmental impact of products. By being able to create the scoring system themselves, there is usually a good opportunity to make it favorable for themselves.

The reason I wanted to go through these different product portfolios is because of what I intuitively feel and consider fairly obvious:

As the world gradually reopens, people have saved money and are most likely to spend it on celebrations and investing in themselves. Taking care of oneself. The need for various products will gradually increase as people meet others outside the home more often. Hairdresser visits will no longer be delayed, days without makeup will decrease, and globally, various celebrations are approaching.

L’Oréal states that during the pandemic, it invested in social media visibility to attract young people to its brands. As travel increases, many people will pick up souvenirs. It will be interesting to see how growth develops. Will it develop steadily?

There’s also an opportunity to gain market share from competitors.