Buffett’s investment philosophy is outwardly simple. You look for businesses among publicly traded companies that are guaranteed to make money decade after decade. You buy these companies at a reasonable price and let time do the rest. No day trading, constant market timing, stressing about macroeconomics, or dreaming of company-specific turnarounds.

Now, all you have to do is identify these excellent businesses. A company should have:

An understandable product or service

A long history of growing earnings

An industry that doesn’t constantly require large investments

Good return on capital

Low debt

Good management

Bright future prospects.

Which publicly traded companies you know best meet these criteria?

Extremely simple service. In practice, they take a commission from every bank card transaction. They essentially have a duopoly in the market. Strong growth for years now. In addition, there are many markets where payment cards are only just starting to become common.

I was going to answer Apple, but the correct answer is…

Microsoft - A company at the top of the world for four decades now. An excellent product portfolio and a technical ability to innovate. They have software but also hardware, and the company is not dependent on economic cycles in the same way as many others. A good brand but also suitably hidden, and I can’t think of a single scandal related to Microsoft offhand - cf. other US tech companies.

PepsiCo

Good portfolio and steadily reliable.

Well-managed, strong pricing power, and not too burdened by debt. Brand recognition and global market presence smooth out fluctuations.

In my opinion, KONE best meets Buffett’s criteria on the Helsinki stock exchange. Revenue and earnings are on a consistently strong growth path, the business idea is clear, and capital returns are around 30%. The company’s management does a guaranteed solid job – in addition to their core work, it has been impressive to see how, for example, in 2020, they withdrew from the bidding for Thyssenkrupp’s elevator business when the price and potential advance payments spiraled out of control. Furthermore, KONE is global, debt-free, and conducts business far into the future, propelled by the tailwind of urbanization.

The main reason many seem to have for not buying KONE is that the stock is always expensive. I’ve started to wonder if that’s truly a rational reason to refrain from buying. There are many other stocks that, when evaluated by metrics like the P/E ratio, are perpetually cheap. So, if KONE is expensive now, grows in value for, say, ten years, and is still expensive, what does the high valuation at the time of purchase really matter?

Both have been in my portfolio for over 7 years.

A similar company would be VeriSign Inc. (VRSN), which has a net income of $0.8 billion on a revenue of $1.37 billion – not cheap even now, but a candidate.

Here’s a company description:

VeriSign, Inc., together with its subsidiaries, provides domain name registry services and internet infrastructure that enables internet navigation for various recognized domain names worldwide. It enables the security, stability, and resiliency of internet infrastructure and services, including providing root zone maintainer services, operating two of the 13 internet root servers; and offering registration services and authoritative resolution for the .com and .net domains, which support global e-commerce. The company also back-end systems for .cc, .gov, .edu, and .name domain names, as well as operates distributed servers, networking, security, and data integrity services. VeriSign, Inc. was incorporated in 1995 and is headquartered in Reston, Virginia.

These days, in addition to price, the reason not to buy probably stems from the high China risk. It’s a great company, but geopolitics can’t be escaped. I hope Kone manages to acquire Toshiba’s elevators, and in my opinion, they could pay a rather high price for them. A large amount of steady, albeit slowly growing, business from a stable country would lower Kone’s risk profile.

You speak the truth. The other side of the coin is that KONE has many strong pillars in its China business. If construction slows down for a moment, the service market and the modernization of old elevator fleets remain. Not all risks can be avoided, but perhaps these companies best suited for long-term ownership distinguish themselves in risk management.

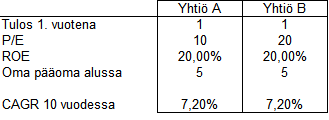

This can be modeled. Let’s imagine two companies, one with a P/E of 10 and the other with a P/E of 20, but which are otherwise identical, grow their earnings by 7.2% each year, thereby doubling their earnings in 10 years. Both companies have a return on equity of 20%.

Stock returns consist of three components:

Change in earnings

Change in valuation multiples

Dividends

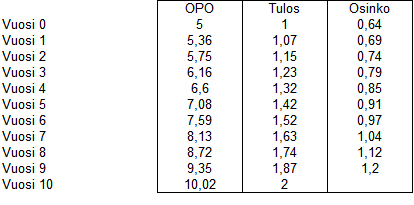

Here, it is assumed that the valuation multiple does not change, but remains the same. The dividend paid is the residual of earnings after investments. Let’s assume no tax is levied on dividends. Investments are required to grow earnings. The table looks like this:

Dividends accumulate to a total of 8.93 euros over the period (taxes are not taken into account).

Company A’s share price is 20 euros at the end, and Company B’s share price is 40 euros, according to their P/E ratios.

The annual return can be calculated with this formula:

Company A:

10 * (1+x)^10 = 20+8.93

x = 11.2%

Company B:

20 * (1+x)^10 = 40+8.93

x = 9.4%

A low valuation multiple thus slightly increases returns, assuming other factors remain constant, but perhaps not as much as one might think without calculating. The tax levied on dividends narrows the return difference, as does the lengthening of the investment period.

But there’s one fairly obvious flaw in the approach I’ve presented here. It’s not insignificant whether you pay double the price for a similar company. If you have 20 euros available at the beginning, you can buy one share of Company B or two shares of Company A. The P/E ratio tells you how many euros one euro of earnings costs. An investor who puts 20 euros into Company A earns double the dividends compared to someone who invests in Company B, and can also reinvest these dividends. In real life, the equations are such that a company with a high P/E is expected to grow its earnings, and a company with a low P/E is expected to see its earnings decline. A P/E premium (i.e., sacrificing some expected return) might also be paid because earnings are stable and predictable.

Successful investing is about buying a company that is affordable but

An excellent reminder of how returns are generated. Three important factors for me are:

Growing faster than competitors

Being more profitable (net margin, ROE) than competitors

Having a strong balance sheet, which ensures financial flexibility and investment opportunities even during downturns

In Finnish companies like Kone, one common problem is often the lack of investment targets. As you mentioned, it impacts how much can be invested in high-ROE opportunities. Kone has to pay out a large portion of its profits as dividends and cannot reinvest in targets that would yield returns consistent with the company’s +30% ROE. If you find a highly profitable company that can reinvest the lion’s share of its earnings year after year to grow the business while maintaining a high return on equity, the end result is staggering!

Edit:

On the other hand, it is even better to find a company that doesn’t even require capital for growth. Meaning the business grows with the same profitability without significant investments, and a large portion of the earnings can be distributed as dividends.

I fully subscribe to this goal. However, what I would do differently is that I think it’s more sensible to consider budding emerging industries, diversify into them before their significance is widely understood, and then just wait. In recent decades, these have included at least the rise of the internet and mobile business, the massive growth of the gaming industry, electric vehicles, the sharing economy, green energy production, cryptocurrencies and blockchains, AI, and now, currently, at least electric aviation.