A small Lithium update.

Lithium Price and Costs

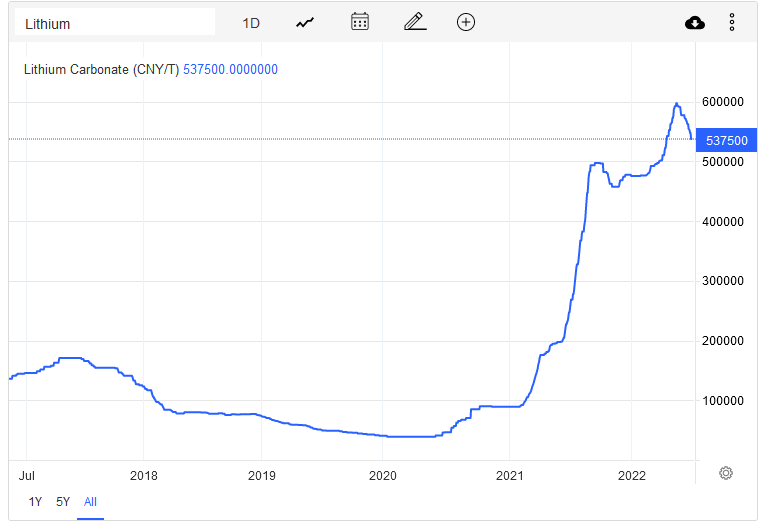

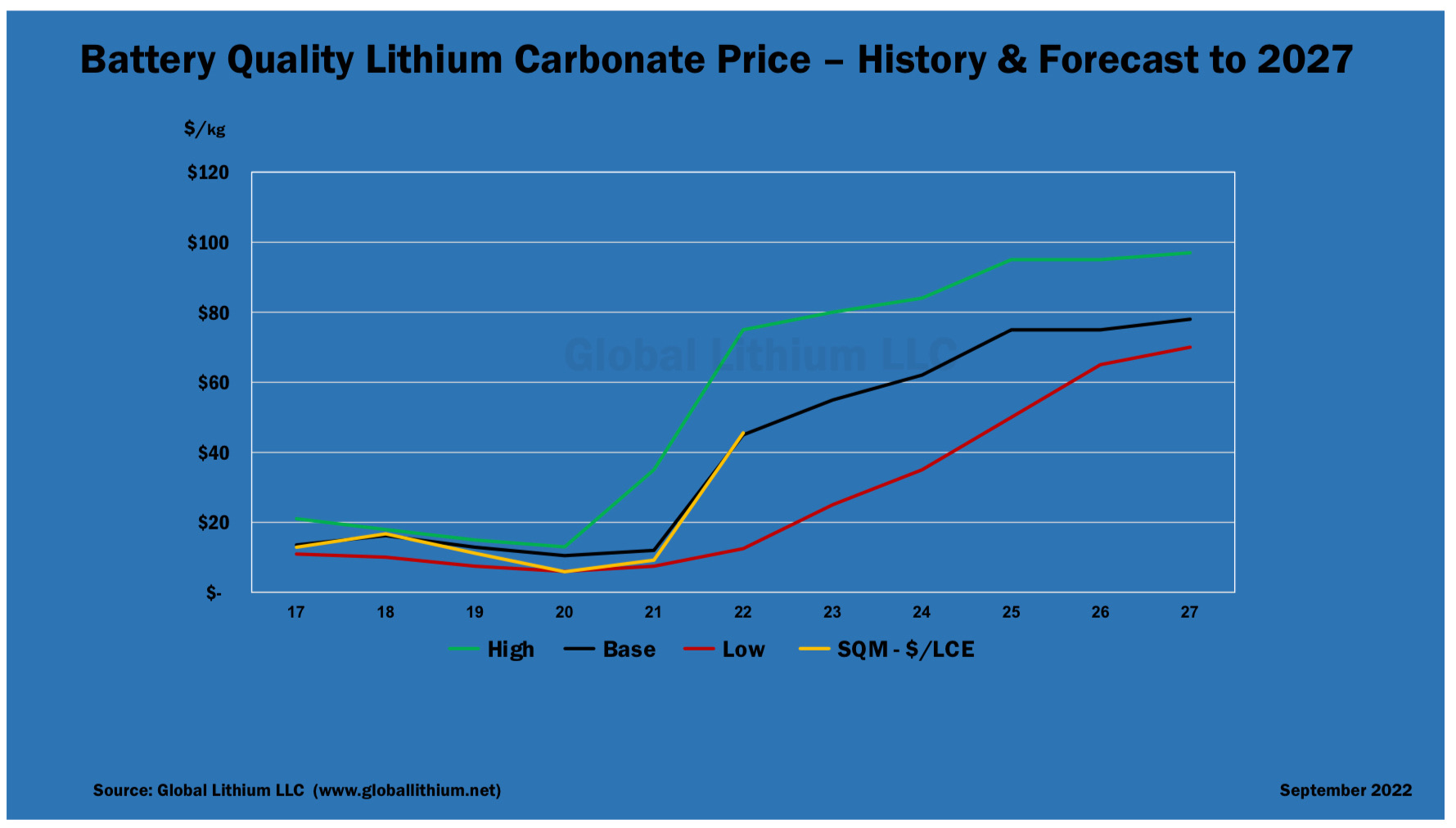

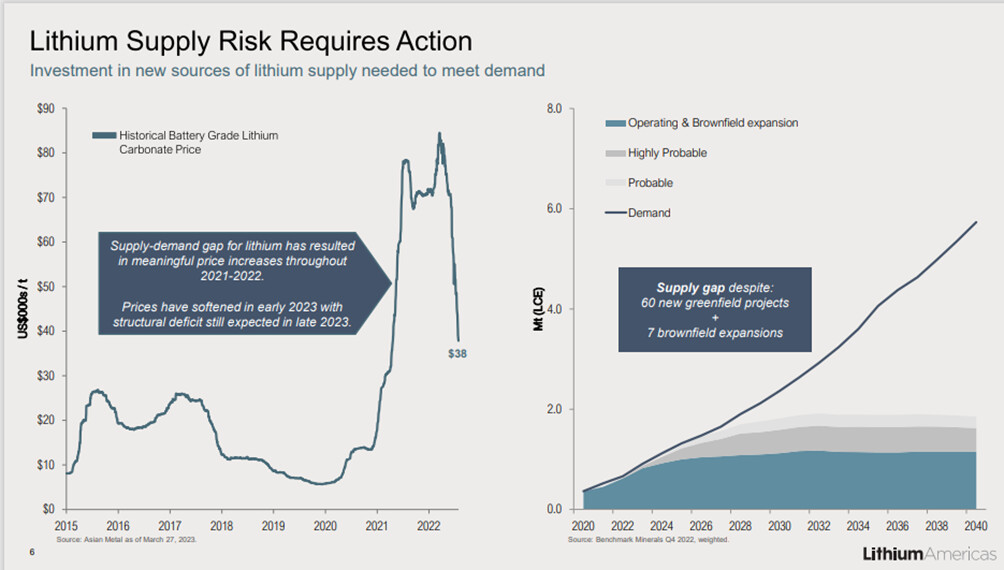

The market price of lithium has plummeted during 2023. The most followed price is the China spot price for lithium carbonate (on the left in the attached LAC slide). The same slide shows Benchmark Minerals’ presentation on the supply and demand imbalance.

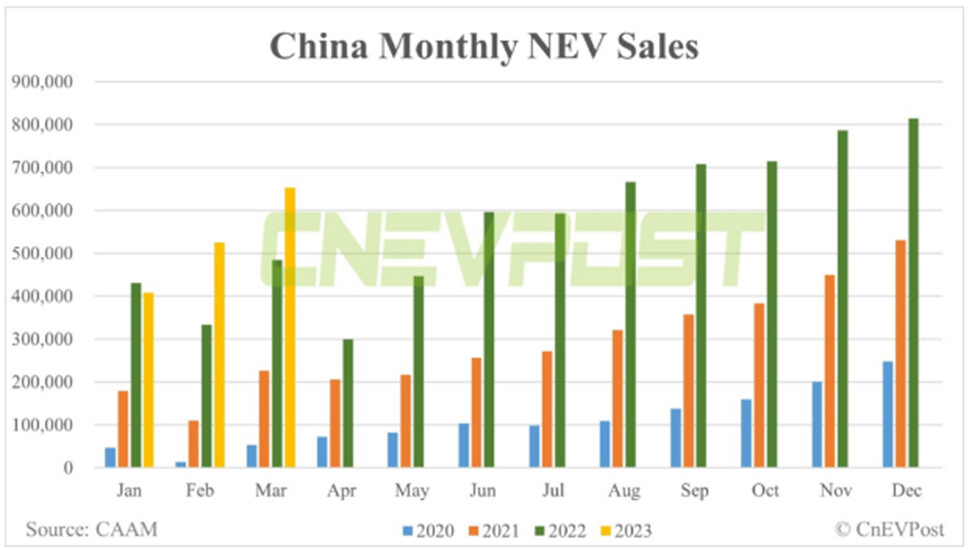

In China, Q1 is always weak. This year, in addition to normal seasonal variation, H1 is seeing internal combustion engine (ICE) vehicle inventories being cleared with massive discounts due to upcoming Chinese emission regulations, which is temporarily reducing EV demand in H1. Even so, China’s EV sales don’t look completely catastrophic after a poor January:

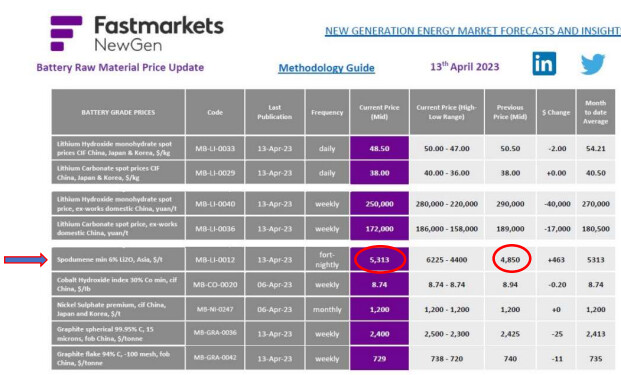

Now might be an interesting moment in the spot market. The spot price of spodumene, used as a raw material for lithium carbonate and hydroxide (which never fell as sharply as the end-product price), has turned upward. (This is a good thing for Sigma, for example, which specifically produces and sells that spodumene, partly at spot prices. Sigma’s own estimates are calculated with a spodumene price of $3,956, which would result in a free cash flow of $1.8B in late 2024. Market cap is currently $4.1B. Sigma’s spodumene is 5.5% grade; the spot price is for 6% spodumene.)

According to quite credible estimates, the current spot price of raw material spodumene means that the end product, lithium carbonate, is being sold below cost, which has already led to production cuts in China while demand shows slight signs of recovery. Lithium can no longer be produced cheaply in large quantities; instead, Chinese producers in particular have to extract lithium raw material expensively from lepidolite. Therefore, costs at the right end of the cost curve are something quite different from the low-cost producers at the left end. This creates a new floor for the price of lithium.

“Daniel Jimenez highlights the current disconnect between spot spodumene prices and spot lithium carbonate (LC) prices in China. He points out that the spodumene concentrate price has increased to $5,313 per tonne, which translates to a lithium carbonate cost of $52 per kilogram, without any margin for the refiner. However, current spot prices for lithium carbonate in China are between $25 and $35 per kilogram, creating an apparent discrepancy.”

Personally, I interpret this to mean that if the price of spodumene does not turn downward again (which I don’t believe it will), we will see the bottom for carbonate within a few months. If this holds true, the bottom for lithium stocks may have been in March for now. If so, March might have been the best buying opportunity since '21, and we are still not very far from it. Naturally, a macro-level analysis must be done separately, and a larger recession could disrupt the picture. However, a lot of spodumene is sold to China, so geography must be included in the macro analysis.

Edit: I won’t change the previous paragraph afterward, but after further research, it is quite possible that the price of spodumene will decrease during Q2-Q4. Although demand is growing, in addition to Sigma’s significant production, several producers will enter the market in the coming months, which could momentarily saturate the market.

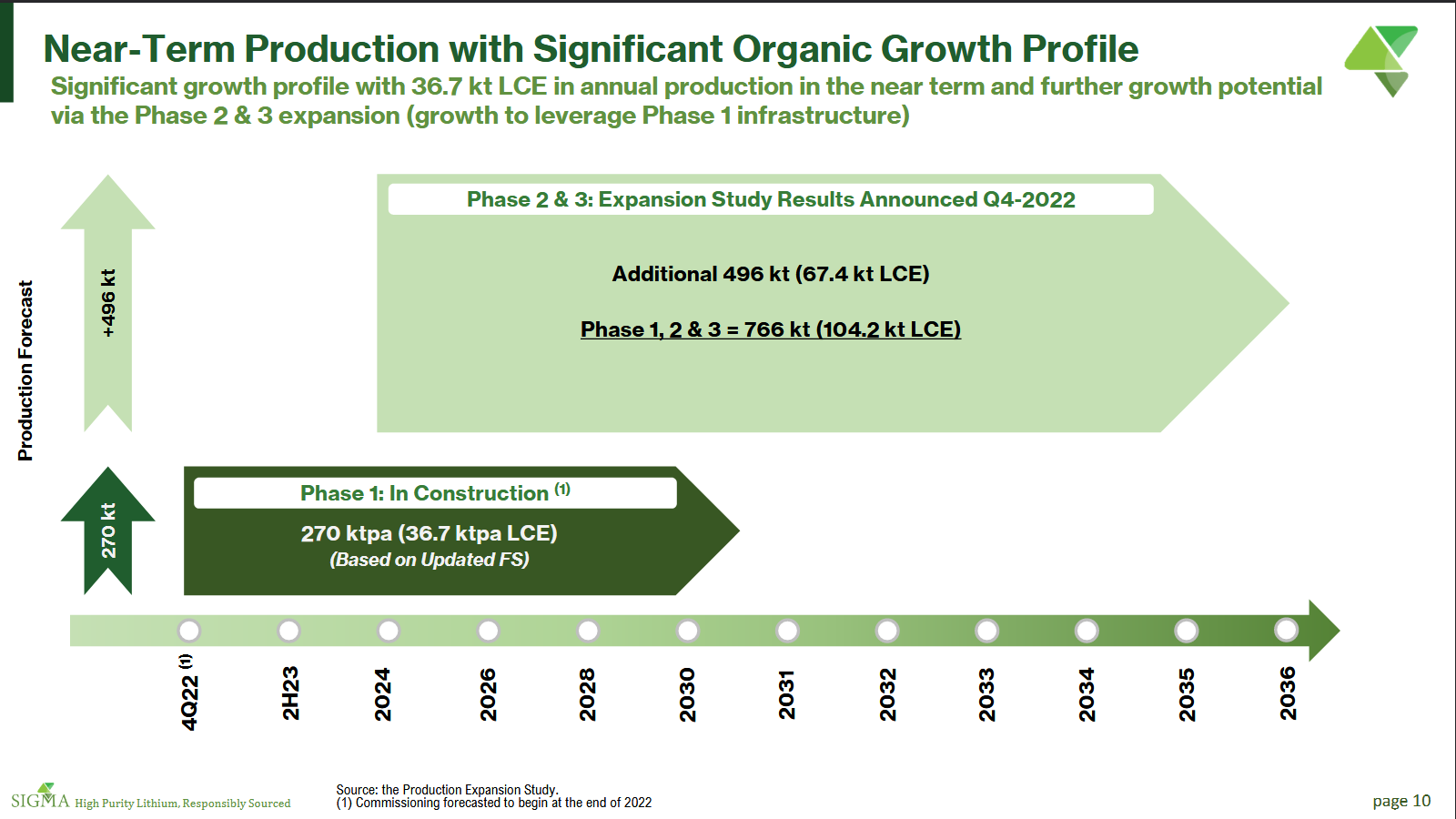

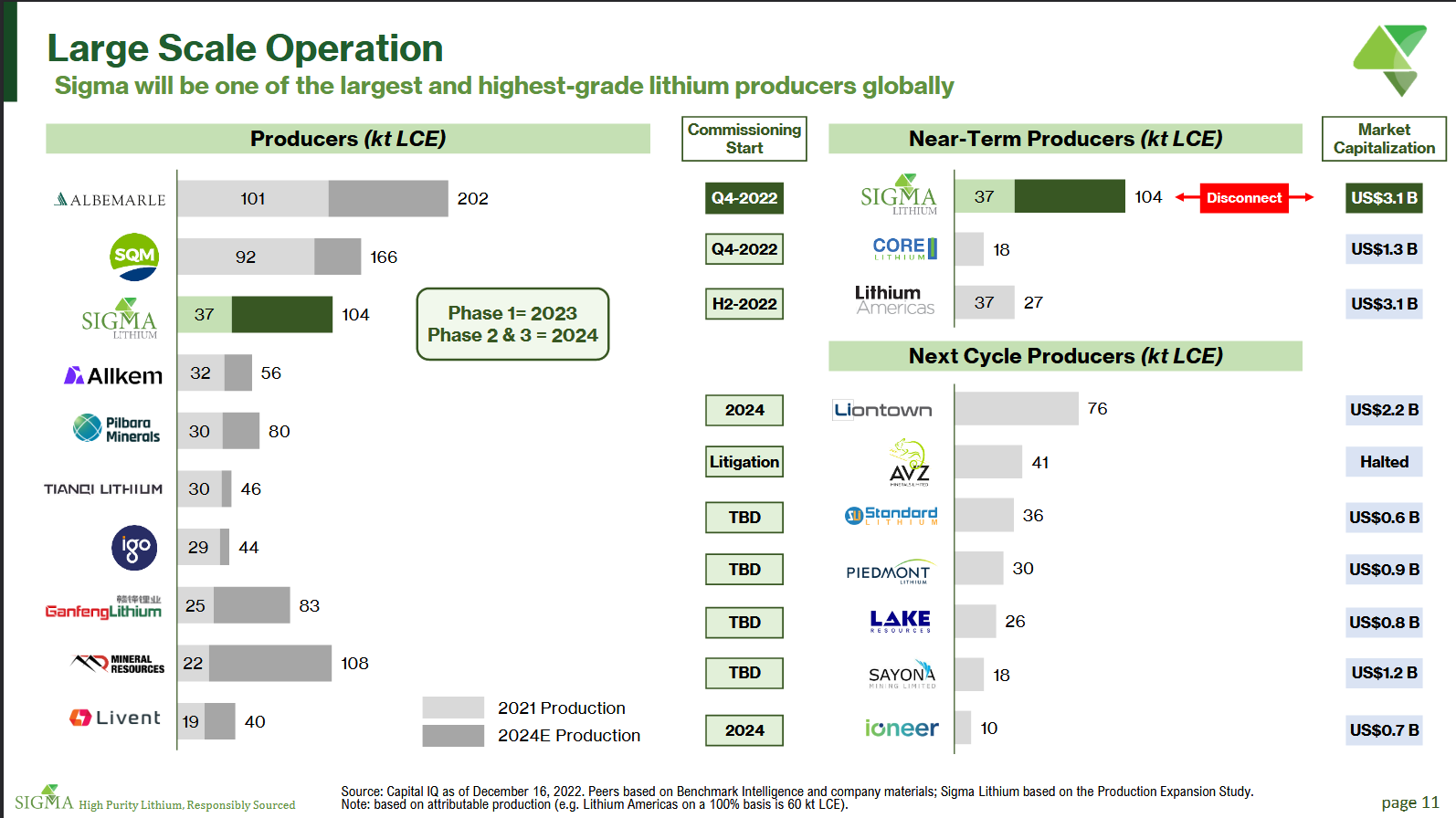

Lithium Americas

LAC updated its situation earlier this year. The separation of North American (Thacker Pass) and South American operations is still expected, though there is no precise information yet. However, this enables, among other things, obtaining US government-guaranteed loans for up to 75% of Thacker Pass’s massive capex. Otherwise, the project might be difficult to finance. There is potential in LAC, but the capex for Phase 1 of Thacker Pass alone is $2.3B. The result here is an end product, so this cannot be directly compared to the raw material producer Sigma, but Sigma’s capex in Brazil is approx. $300M including phases 1-3, resulting in 104 kt (LCE) production and $2.5B revenue. LAC’s Thacker Pass Phase 1 production is 40 kt (LCE) in 2026 and the revenue forecast is $1.1B with a selling price of $36k/tLCE. These are not directly comparable, and LAC’s assets are much larger than Sigma’s, but the figures provide some indication. LAC still faces the risk that lithium at Thacker Pass must be extracted from clay. So far, no one has done this successfully on a commercial scale, but they have a quite credible plan for it.

In South America, LAC’s Caucharí-Olaroz is expected to start commercial production at the end of H1. After the ramp-up, it should produce 40kt of the end product, lithium carbonate. The capex here is also quite high, about $650M, but this is already financed. Revenue could be $1.4B when Phase 1 is running at full capacity.

M&A

Consolidation continues. Some car manufacturers (e.g., GM) are entering the mining business. Tesla (Musk) says mining lithium is easy but refining is difficult, and is building its own refinery. Some experts disagree completely: a refinery can be built in a few years, but opening a mine takes a decade. Large lithium mining companies want more assets and are buying smaller ones. Lithium giant Albemarle’s hostile bid for Australian Liontown instantly nearly doubled Liontown’s share price. Yet, the bid did not go through. Sigma has been pushed up by several sale rumors, and Sigma is owned by investment bankers and is certainly for sale. On the other hand, Sigma is now hitting a developing resource shortage with massive production and will need more assets in the 2030s. There are a couple of interesting small projects near Sigma that could be bought at a reasonable price. Additionally, there are rumors of interest from large non-lithium mining companies in smaller lithium juniors. In my opinion, the market is still in an interesting phase.