Lentoasemilla on usein käytännössä monopoliasema palvelemallaan alueella; ne vievät valtavasti tilaa, aiheuttavat lentomelua ja vaativat suuria investointeja ja tarvitsevat tuekseen runsaasti muuta infrastruktuuria. Siksi uusia ei yleensä rakenneta tuosta vain.

Suuri osa lentoasemayhtiöistä on kokonaan valtion tai muun julkisen tahon omistuksessa ja niiden päätehtävänä ei nähdä voiton tuottamista omistajille vaan paikallisen väestön ja elinkeinoelämän vaatiman matkustamisen ja lentorahdin mahdollistaminen. Esimerkiksi suurimman osan Suomen kaupallisista lentoasemista omistaa valtionyhtiö Finavia minkä lisäksi muutama on kuntien omistamia.

Osa lentoasemista on puolestaan erilaisten pääomasijoittajien ja eläkevakuutusyhtiöiden omistuksessa, tästä esimerkkinä vaikka tänään uutisotsikoissa ollut Lontoon Heathrow.

Osa lentoasemista on kuitenkin listattu pörssiin joskin mukana on usein jokin julkinen taho enemmistöomistajana. Seuraavassa listaa tiedossani olevista pörssilistatuista lentoasemayhtiöistä:

- Aena

- 46 lentoasemaa Espanjassa - markkina-arvo 32.8 mrd€

- 46 lentoasemaa Espanjassa - markkina-arvo 32.8 mrd€ - Airports of Thailand

- 10 lentoasemaa Thaimaassa - markkina-arvo 15.6 mrd€

- 10 lentoasemaa Thaimaassa - markkina-arvo 15.6 mrd€ - Shanghai Airport

- Shanghain molemmat lentoasemat - markkina-arvo 10.3 mrd€

- Shanghain molemmat lentoasemat - markkina-arvo 10.3 mrd€ - Aéroports de Paris

- Pariisin kaikki 3 lentoasemaa - markkina-arvo 9.8 mrd€

- Pariisin kaikki 3 lentoasemaa - markkina-arvo 9.8 mrd€ - GMR Group

- 5 lentoasemaa Intiassa, 1 Filippiineillä ja 1 Kreikassa - markkina-arvo 9.6 mrd€ (yllä mainittu ADP omistaa 49%)

- 5 lentoasemaa Intiassa, 1 Filippiineillä ja 1 Kreikassa - markkina-arvo 9.6 mrd€ (yllä mainittu ADP omistaa 49%) - Grupo Aeroportuario del Pacífico

- 12 lentoasemaa Meksikossa ja 2 Jamaikalla - markkina-arvo 8.9 mrd€

- 12 lentoasemaa Meksikossa ja 2 Jamaikalla - markkina-arvo 8.9 mrd€ - Grupo Aeroportuario del Sureste - 9 lentoasemaa Meksikossa - markkina-arvo 8 mrd€

- Auckland Airport

- Aucklandin lentoasema - markkina-arvo 7 mrd€

- Aucklandin lentoasema - markkina-arvo 7 mrd€ - Zurich Airport

- Zürichin lentoasema ja muutama Etelä-Amerikassa - markkina-arvo 6.8 mrd€

- Zürichin lentoasema ja muutama Etelä-Amerikassa - markkina-arvo 6.8 mrd€ - Copenhagen Airport

- Kööpenhaminan ja Roskilden lentoasemat - markkina-arvo 6.8 mrd€

- Kööpenhaminan ja Roskilden lentoasemat - markkina-arvo 6.8 mrd€ - Fraport

- Frankfurtin lentoasema ja lisäksi erilaisia osaomistuksia ja operointisopimuksia vähän joka puolella - markkina-arvo 5.4 mrd€

- Frankfurtin lentoasema ja lisäksi erilaisia osaomistuksia ja operointisopimuksia vähän joka puolella - markkina-arvo 5.4 mrd€ - Flughafen Wien

- Wienin, Maltan ja Košicen lentoasemat - markkina-arvo 4.4 mrd€

- Wienin, Maltan ja Košicen lentoasemat - markkina-arvo 4.4 mrd€ - Grupo Aeroportuario Centro Norte - 13 lentoasemaa Meksikossa - markkina-arvo 3.7 mrd€

- Athens International Airport -

- Ateenan lentoasema - markkina-arvo 2.7 mrd€

- Ateenan lentoasema - markkina-arvo 2.7 mrd€ - Corporación América Airports

- 52 lentoasemaa eri maissa, mm. Argentiina ja Brasilia - markkina-arvo 2.6 mrd€

- 52 lentoasemaa eri maissa, mm. Argentiina ja Brasilia - markkina-arvo 2.6 mrd€ - Japan Airport Terminal

- liiketoimintaa eri lentoasemilla Japanissa mutta pääroolissa Hanedan lentoasema Tokiossa - markkina-arvo 2.5 mrd€

- liiketoimintaa eri lentoasemilla Japanissa mutta pääroolissa Hanedan lentoasema Tokiossa - markkina-arvo 2.5 mrd€ - TAV Airports Holding

- 15 lentoasemaa eri maissa mm. Turkissa, Keski-Aasiassa, Lähi-Idässä jne. - markkina-arvo 2.2 mrd€

- 15 lentoasemaa eri maissa mm. Turkissa, Keski-Aasiassa, Lähi-Idässä jne. - markkina-arvo 2.2 mrd€ - Beijing Capital International Airport Company - Pekingin molemmat lentoasemat - markkina-arvo 1.5 mrd€

- Toscana Aeroporti

- Firenzen ja Pisan lentoasemat Toscanassa - markkina-arvo 300 m€

- Firenzen ja Pisan lentoasemat Toscanassa - markkina-arvo 300 m€ - Aeroporto G. Marconi di Bologna - Bolognan lentoasema - markkina-arvo 290 m€

Yhtiöitä erottaa maantieteellisten sijaintien lisäksi liiketoiminnan luonne. Osassa tapauksista on kyse vain lentoasemien operoimisesta kun taas toisilla on isoja kiinteistö- ja vähittäiskauppa ym. bisneksiä. Velkatasoissa on myös eroja.

Alan kasvun moottorina on globaalin lentoliikenteen kasvu jota tukee mm. väestön vaurastuminen etenkin kehittyvissä talouksissa. Pitkällä aikavälillä on merkitystä sillä, minkä kohteiden houkuttelevuus kasvaa ja toisaalta sillä, mistä matkustetaan tulevaisuudessa enemmän.

Lentoasemayhtiöihin sisältyy aina poliittista riskiä koska ne ovat hyvin alttiita sääntelylle tai huonolle tai ailahtelevalle pääomistajan ohjaukselle. Esimerkiksi velkaiselle valtio-omistajalle voi tulla lyhytnäköinen kiusaus lastata lentoasemayhtiö raskaaseen velkakuormaan ja maksaa samaan aikaan sieltä osinkoja budjetin tilkitsemiseksi tms.

Muita riskejä ovat esim. geopolitiikka (ilmatilojen sulkemiset jne.) ja mahdolliset pandemiat.

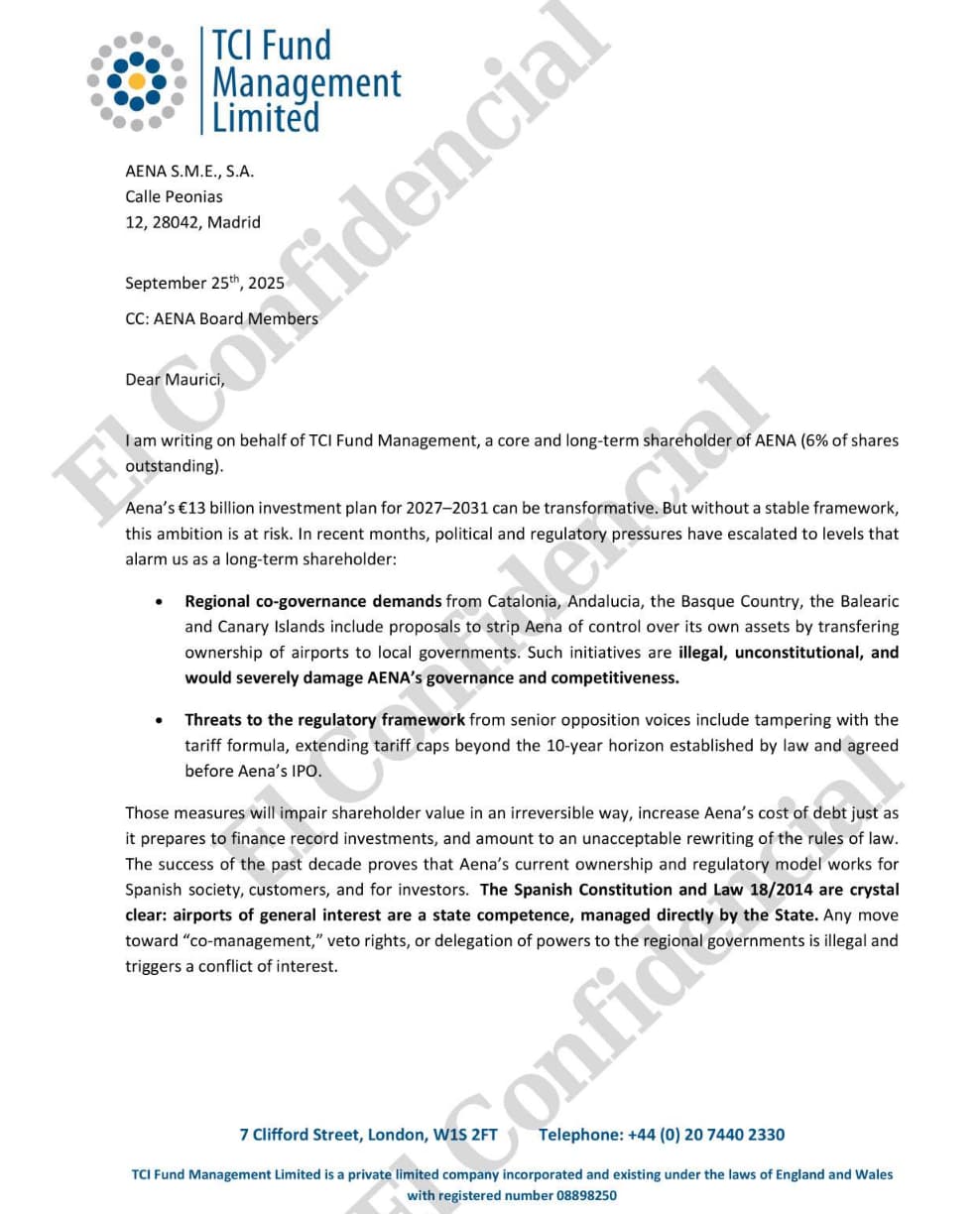

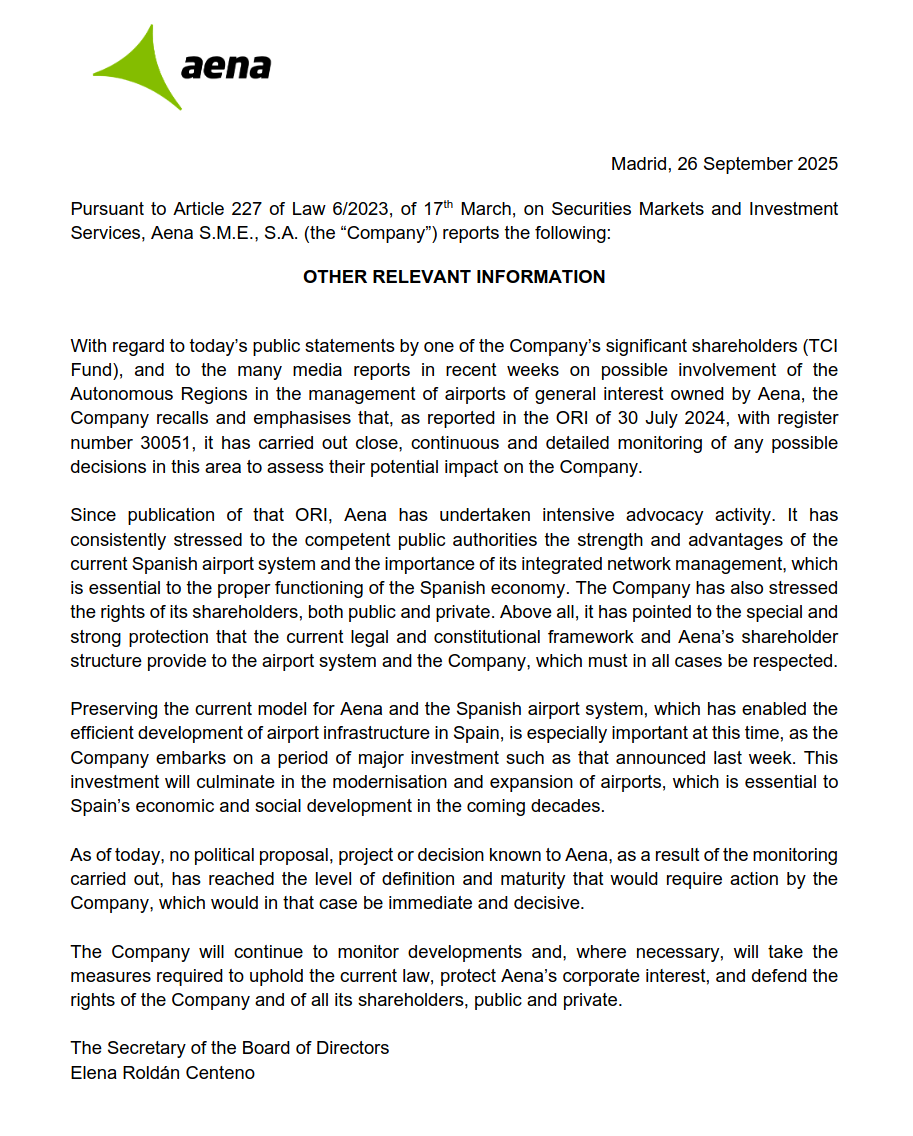

Omassa salkussani on tällä hetkellä pienehkö määrä parisen vuotta sitten ostettua Aenaa. Onko muita lentoasemiin sijoittaneita tai alaa tutkineita?