Avataanpas ketju mielenkiintoiselle espanjalaiselle matkailualaan keskittyneelle ohjelmistoyhtiölle, joka on erityisesti tunnettu nimensä mukaisesta Amadeus-varausjärjestelmästä lentoyhtiöille ja matkatoimistoille. Yhtiö on perustettu 1987 ja on maailman johtava toimija omissa nicheissään. J.P. Morganin analyysin mukaan yhtiöllä olisi yli 40 %:n markkinaosuus sekä GDS-järjestelmissä (global distribution systems) että PSS-järjestelmissä (passenger service systems for airlines). Amadeus oli nimenä tuttu jo aiemmin, mutta satuin bongaamaan yhtiön löytyvän Terry Smithin luotsaaman Fundsmithin salkusta (tuoreessa kirjakerhossa puhuttiin juuri Smithin sijoitusfilosofiasta). Tämä herätti kiinnostuksen vilkaisemaan yhtiötä hieman lisää.

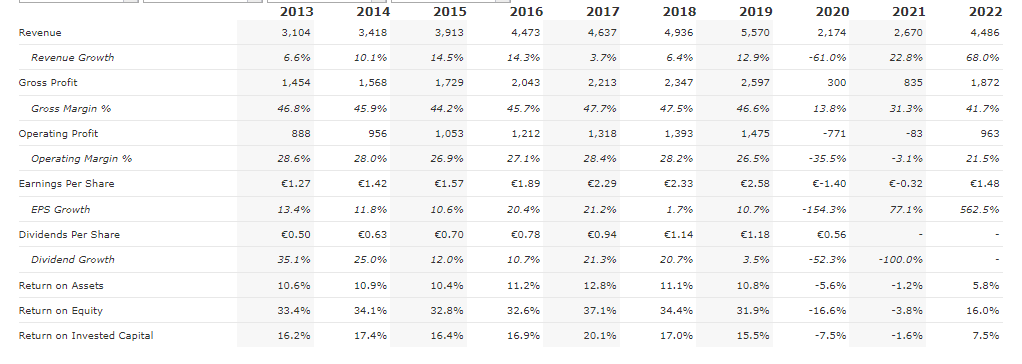

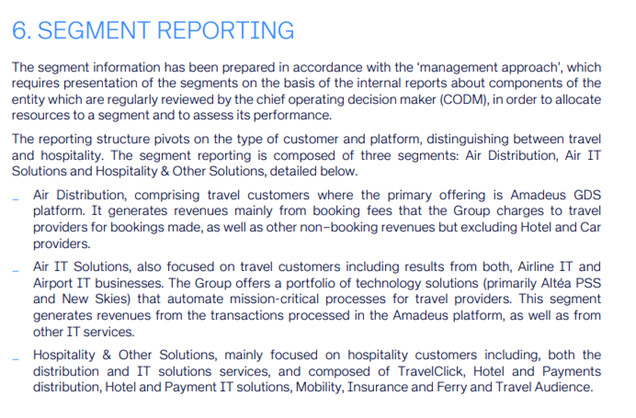

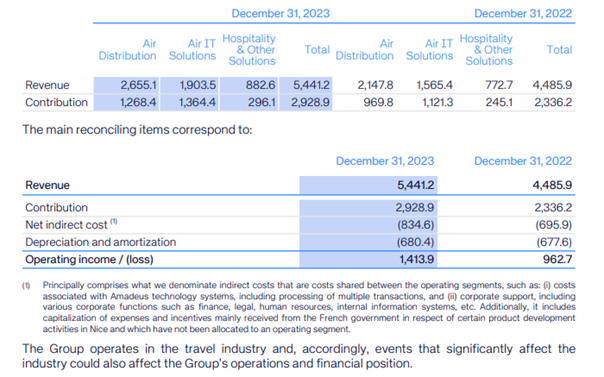

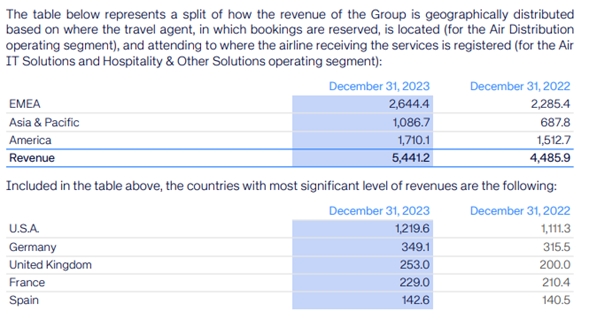

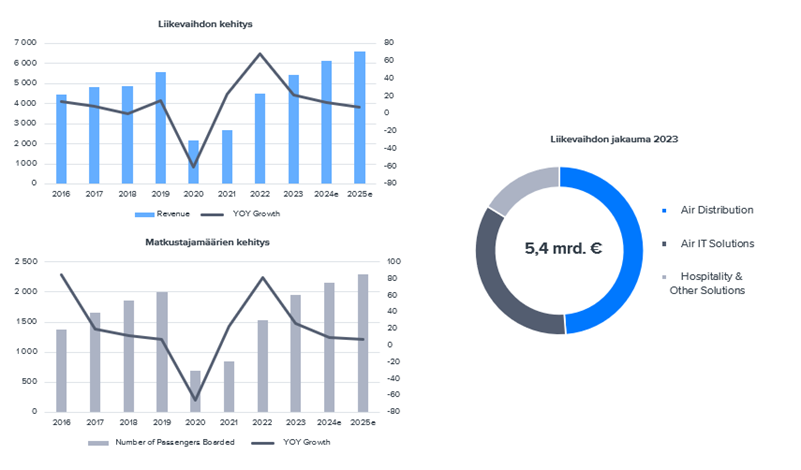

Alla vuosikertomuksesta liiketoiminta-alueet ja liikevaihdon maantieteellinen jakauma. Vuonna 2023 liikevaihto kasvoi 21 % 5,4 miljardiin euroon. Tästä lohkesi 1,4 miljardia oikaistua liiketulosta (26 % lv:sta) ja 1,15 miljardia vapaata kassavirtaa (21 % lv:sta).

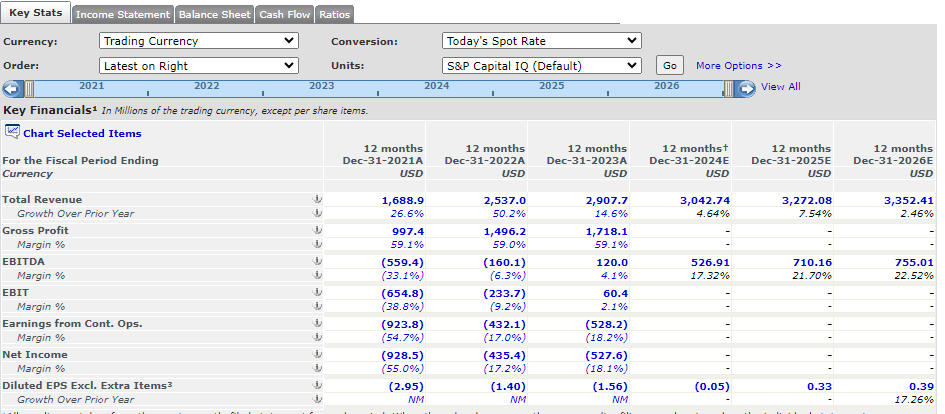

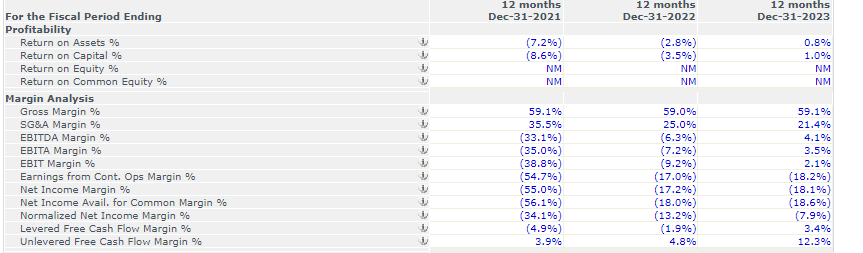

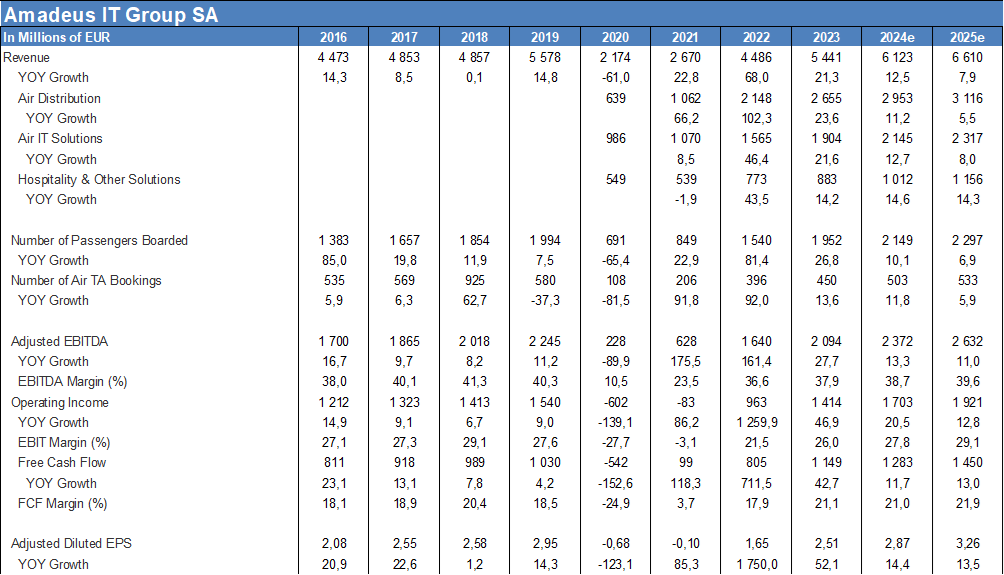

Tässä pieni yhteenvetotaulukko Bloombergilta avainluvuista ja analyytikoiden lähivuosien ennusteista:

Luvuista visualisoituna näkee aika suoraan, että yhtiön liikevaihto nojaa yhtiön järjestelmien kautta tehtyjen varausten määrään. Koronapandemia iski näin ollen voimalla yhtiön lukuihin ja oikeastaan nyt vuonna 2024 liiketoiminta, kuten myös matkustajavolyymit näyttäisivät elpyvän pandemiaa edeltävälle tasolle.

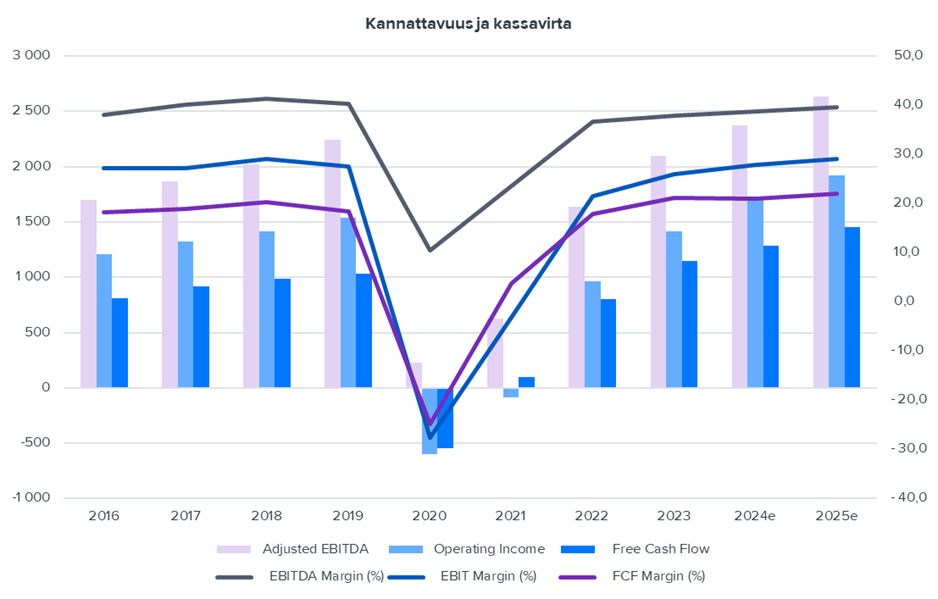

Sama kehitys on luonnollisesti nähtävissä tuloksen ja vapaan kassavirran kehityksessä. Kaiken kaikkiaan yhtiötä voisi tituleerata tällä hetkellä kannattavasti kasvavaksi kasvuyhtiöksi ja marginaalit sekä kassavirtakonversio (liikevoitosta) mukavalla tasolla.

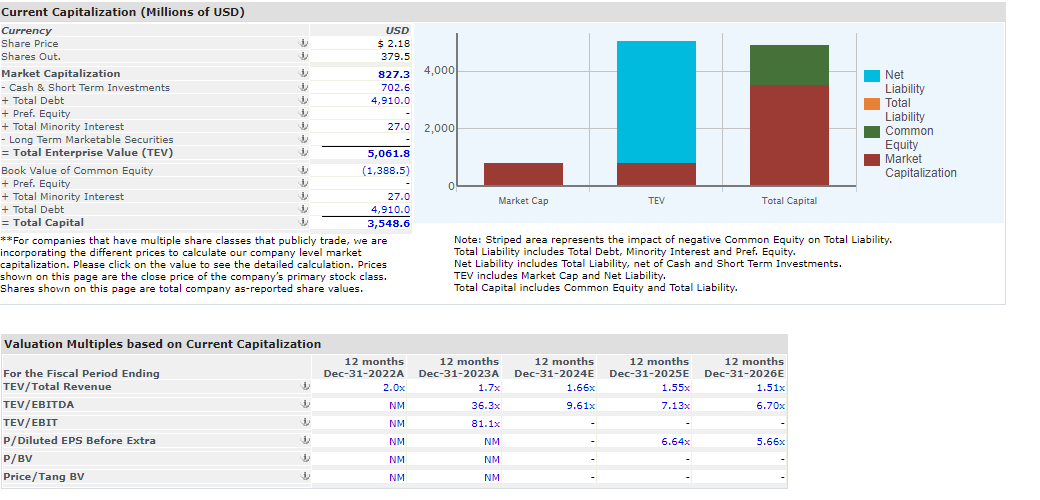

No mitäs tämmöisestä yhtiöstä sitten saa arvostusmielessä pulittaa, alla Bloombergilta konsensusennusteiden yhteenveto ja multippelit:

Nykyisellä noin 25 miljardin euron markkina-arvolla (n. 57e osakekurssi) osake treidaa tälle vuodelle P/E 20x ja vapaan kassavirran tuotto (FCF-yield) 5 %:n hujakoilla. Ei vaikuta mitenkään mahdottoman korkealta moniin muihin teknoveijareihin verrattuna, mutta esim. J.P. Morganin analyysin perusteella tietty discount on perusteltu. Syinä tähän on hitaampi pitkän aikavälin tuloskasvunäkymä moniin teknoyhtiöihin verrattuna, ja kyllähän tuo koronapandemiassa nähty syklinen elementti luo taustalle myös riskitekijänsä. Velkaa on hyvin maltillisesti taseessa ja viimeisimmän osarin mukaan nettovelka/käyttökate noin 1x tasolla.

Yhtiöllä Bloombergin mukaan peräti 33 analyytikkoa seuraamassa ja suositusjakauma näyttää tällä hetkellä tältä:

J.P. Morganin analyysista lainaus heidän näkemyksestään osakkeen suhteen:

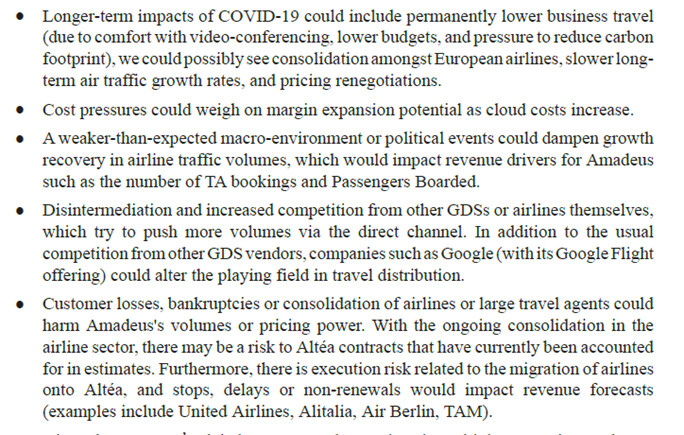

Ja keskeisiä riskejä casen kannalta:

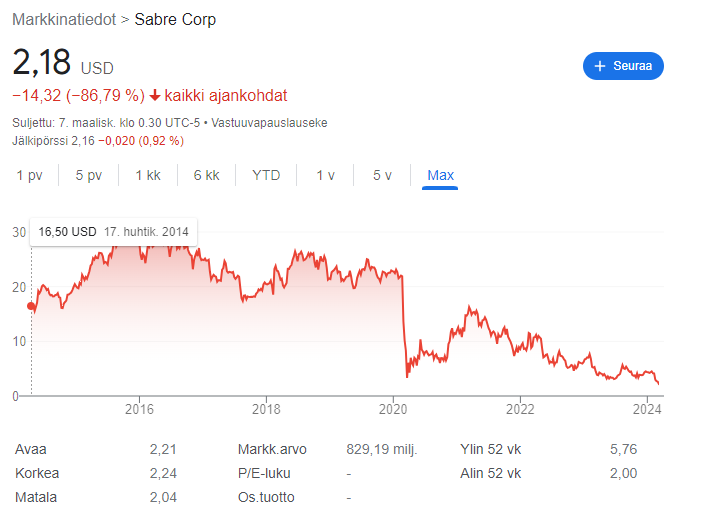

Pidemmän aikavälin kurssikäyrä heijastelee tyypillisen Smithin portfoliosta löytyvän arvonluojan nousevaa käppyrää, joskin tässä koronapandemia näkyy erityisen voimalla:

Kokonaisuutena tuo nykyinen arvostus ei mielestäni kyllä näytä pahalta erittäin vahvan markkina-aseman omaavalle toimijalle. Nappasin pienen seurantasiivun, niin pysyy mielenkiinto vilkaista välillä yhtiön kuulumiset. Jos arvostus tuosta jonkin verran nousisi, niin pidätän oikeuden ottaa voitot nopeastikin kotiin ![]()

Disclamerina mainittakoon, että en tunne yhtiötä tai toimialaa hyvin, joten kyseessä enemmän fiilissijoitus Smithin peesissä. En esimerkiksi osaa arvioida yhtään tuota riskeissä esiin nostettua uusien toimijoiden kilpailu-uhkaa tai lentoyhtiöiden pyrkimyksiä yrittää ohjata matkustajavolyymeja suoraan heidän omiin kanaviin/järjestelmiin.

Kiinnostuneille linkki yhtiön sijoittajasivuille: