Tätä kyllä vähän haastaisin kun omaan silmään näyttää, että nykyiseen hintaan on leivottu jo todella paljon odotuksia. Millä mittarein tai tunnusluvuin katsot Lemonaden halvaksi?

5 tykkäystä

En pysty itse Paperbagia parempaan analyysiin LMND valuaatiosta, tässä video 2kk takaa. Matkalla voi tulla jopa töyssyjä, mutta fair value lienee tänä päivänä jossain $150-200 nurkilla ja eiköhän tuo vuoden loppuun mennessä näy myös kurssissa.

Teen tässä nyt työtä sitten sinun puolestasi, mutta tuo kaveri (lemonade super bull) näyttää excelistään ottavan arvionsa. Lyhyesti kai niin, että jos laskee, että vuonna 2029 tälle annetaan PE 100 arvostus niin olisi nyt arvoltaan tämä osake 182 dollaria. Tietenkin huomiona, ettei lemonade ole vielä yhtään positiivista kvartaalia tehnyt, ja Q3 25 liikevaihtoa tuli 162 miljoonaa dollaria ja tulos oli -37,5 miljoonaa dollaria. Yhtiön market cap on muuten 6 miljardia dollaria, eli nähdäkseni tässä on todella paljon odotuksia lastattu osakkeen hintaan.

5 tykkäystä

Superkasvajan arvottaminen on haastavaa. Toki, jos nykyinen kasvu alkaisi sakkaamaan voisi tuota hinnoittelua kyseenalaistaa. Mutta tilanne on ollut viimeisen vuoden päinvastainen. Jos homma ei käänny voitolliseksi loppu vuonna 26, kuten LMND johto on sanonut. Olisi se ehdottomasti red flag.

Tottakai Lemonade on riskinen. Kasvukipuja yms varmasti tulee ja näitä seurataan LMND-communityssäkkin tarkasti. Myös kilpailijat, esim Geico on palkannut porukkaa, jonka pitäisi kuroa LMND etumatka umpeen.

Mutta yritys on poikkeuksellinen, johto on kokenut ja heillä on kokemusta startuppien kasvattamisesta. Myös ajoitus on ollut kohdillaan, sillä he alkoivat kehittämään AI-vetoista vakuutusyhtiötä yli 5 vuotta ennen kuin AI:sta tuli kuumaa.

Vakuutusyhtiöidenhän on helppoa kasvattaa liikevaihtoa myymällä halvemmalla kuin muut jos ei tarvitse tehdä vakuutustoiminnalla voittoa, mikä on tällä hetkellä tilanne Lemonadella. Itse en puhuisi tässä nyt “superkasvajasta” vaikka liikevaihto onkin kasvanut, mutta näyttää nähdäkseni normaalilta hyvältä kasvulta tuon kokoiselle liikevaihdolle. Kun liikevaihto on miljardiluokassa tulee kasvuprosentitkin näyttämään todennäköisesti erilaiselta. Jos en nyt väärin muista, niin osa liikevaihdon kasvusta on tällä hetkellä myös jälleenvakuuttamisosuuden pienentämistä, mitä ei ikuisesti voi tehdä, eikös tämä ole tilanne?

Ymmärrän superkasvajien arvon määrittämisen vaikeuden yritysten kohdalla kuten Iren tai Nebius, jotka vaihtavat liiketoimintansa nopeasti bitcoinien louhimisesta → AI konesaleiksi ja liikevaihto kasvaa monia satoja prosentteja vuodessa.

Jos haluaa miettiä paljonko on odotuksia ladattu osakkeen hintaan tällä hetkellä niin, voit miettiä että 0% kasvulla, paljonko maksaisit tuon verran liikevaihtoa ja negatiivista tulosta tekevästä yrityksestä?

Tässä vielä liikevaihto:

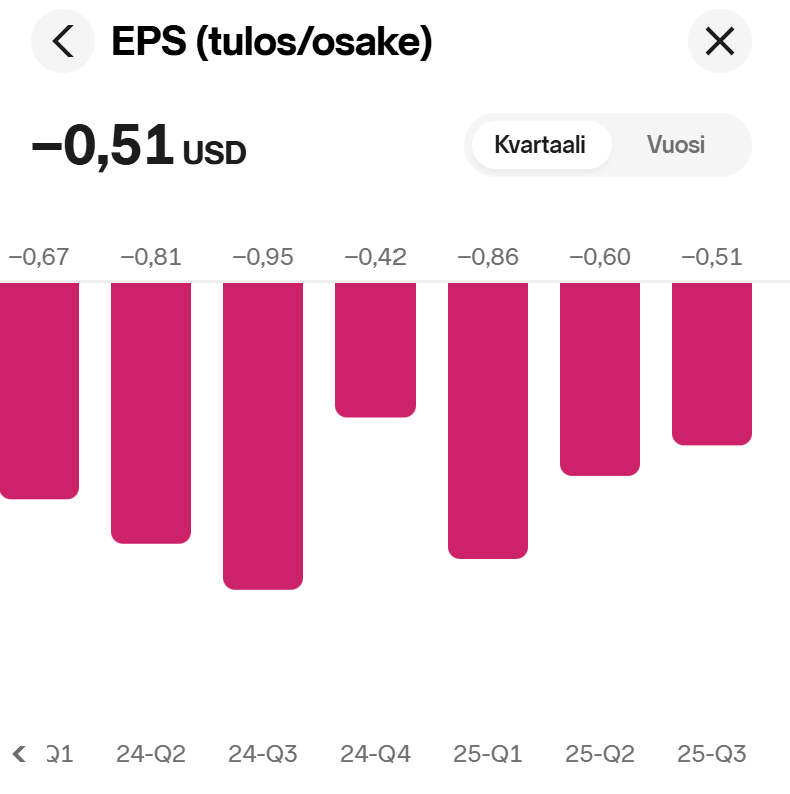

Eps kehitys:

7 tykkäystä

Tässä ketjussakin jo käsitelty, mutta bisnes tekee jo voittoa jos ei kasvupanostuksia oteta huomioon. Jälleenvakuuttamista pienennettiin tänä vuonna 55%→20% ja se tulee näkymään LV:ssä vaiheittaan ja ensi kesänä kokonaan voimassa.

9 tykkäystä

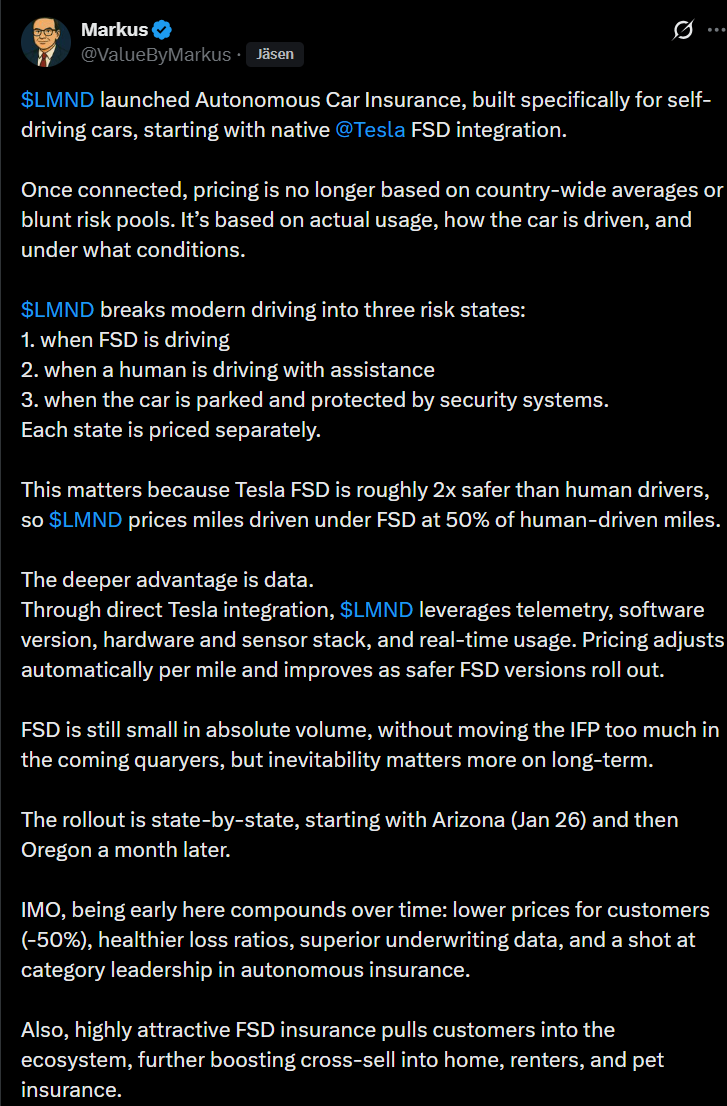

Tässä on Markuksen tviitti siitä, kun Lemonade lanseerasi itseohjautuville autoille suunnatun autonomisen autovakuutuksen. ![]()

IMO, being early here compounds over time: lower prices for customers (-50%), healthier loss ratios, superior underwriting data, and a shot at category leadership in autonomous insurance.

https://x.com/ValueByMarkus/status/2014094118188630384

Markus “lainasi” tässä tviitissään vanhaa tviittiään lokakuulta:

https://x.com/ValueByMarkus/status/1979261528189673770

2 tykkäystä

Laitetaan vielä linkki alkuperäiseen: https://x.com/elonmusk/status/2014039116854300810?s=46

Oli eilen mennä latte väärään kurkkuun, kun iltasella avasin pörssin ja hinta kolkutteli satasen ovilla. Heti aamulla twiitin nähtyäni, olin varma että $90 menee rikki. Matka on vasta alussa, se on varmaa että volaa tulee riittämään jatkossakin. Joku ~40 päivää Q4 tulokseen ja 2026 ohjeistukseen. Mahtava vuosi 2026 edessä!

Nordnetissa sijoittajien määrä kasvaa kivasti, mutta vertailun vuoksi Faronilla on yli 12k omistajaa…

4 tykkäystä

Arvopaperissa mielenkiintoinen artikkeli Lemonadesta ja siitä, miten yhtiö mullistaa perinteistä toimialaa FSD-vakuutusratkaisullaan: Lemonaden yhteistyö Teslan kanssa ravistelee Sampoakin – Vakuutusalan disruptoija on ladattu täyteen sijoittajien toiveita | Arvopaperi

”Sijoittajat saattavat olla ylioptimistisia, mutta sitä ei voi kieltää, etteikö yhtiö ravistelisi koko vakuutusalaa. Perinteiset vakuutusyhtiöt uhkaavat jäädä kilpailussa jälkeen, elleivät ne nopeasti omaksu tekoälyä keskeiseksi osaksi liiketoimintaa.”

2 tykkäystä

Kuulostaa mielenkiintoiselta. Harmittavasti näkyy olevan maksumuurin takana.

Osakkeen hintahan on hieman korjaantunut kun se on lasketellut parissa viikossa like 30%. Pian alkaa tulla Q4 ja 2026 ennakkoja! Kirpeitä aikoja.

Jotenkin vaikea kuvitella, etteikö perinteisissä vakuutusyhtiöissä olisi herätty tekoälyn tulemiseen. Toki isommissa yrityksessä muutokset tapahtuvat varmasti hitaammin, mutta löytyy niiltä varmasti myös eri tavalla resursseja siihen, kun tekoälyä halutaan kehittää omaan liiketoimintaan sopivaksi.

1 tykkäys

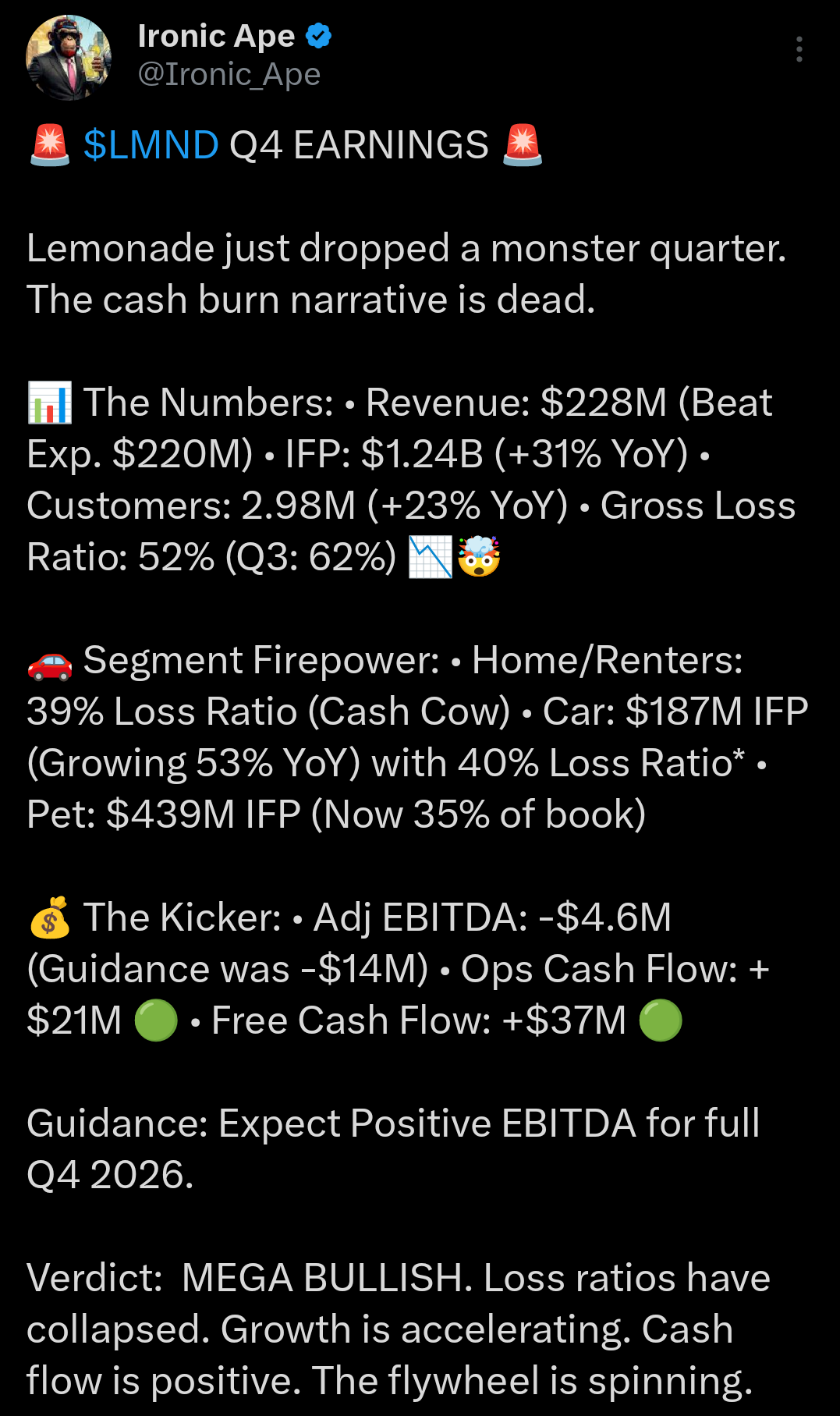

Jos haluaa tuloksen alla fiilistellä markkinoiden parasta LMND-analyytikkoa niin tässä:

Markkina on tarjonnut ostopaikkoja hiljattain. Itsellä ei ole ollut vapaita pelimerkkejä lisätä.

4 tykkäystä

Jaahas, Lemonade näyttäisi olevan kelpo nousussa afterissa. Liekköhän jollain parempaa tietämystä vai vain reilumpaa spekulointia tuloksesta, joka julkaistaan myöhemmin tänään ![]() Noh jokatapauksessa kaukana ollaan vielä Tesla-uutisten siivittämästä noin 100 dollarin tasosta, josta ei ole aikaa kuin noin kuukausi. Omistajilla jännittävä päivä edessä tänään, sillä tuloksen mukana saadaan myös koko vuoden 2026 ohjeistus!

Noh jokatapauksessa kaukana ollaan vielä Tesla-uutisten siivittämästä noin 100 dollarin tasosta, josta ei ole aikaa kuin noin kuukausi. Omistajilla jännittävä päivä edessä tänään, sillä tuloksen mukana saadaan myös koko vuoden 2026 ohjeistus!

7 tykkäystä

Se on siinä. ”By any measure, the fourth quarter of 2025 was our strongest ever.”

5 tykkäystä

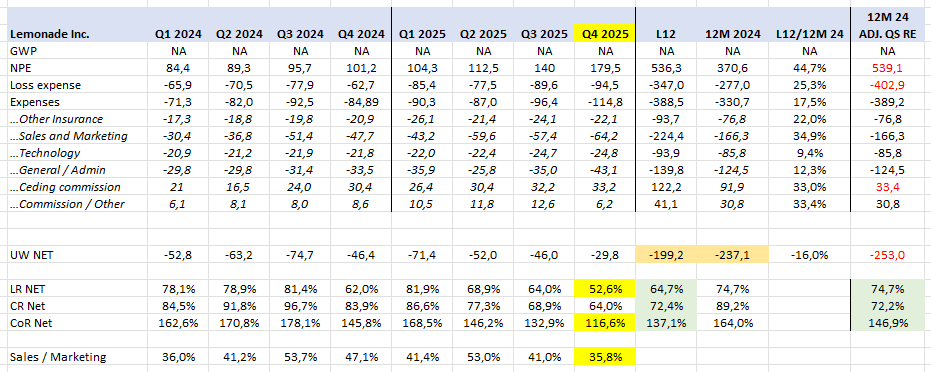

Positiivista (keltainen) - negatiivista (vihreä ja ruskea). Ohjeistus heikko. Pitkä matka kannattavaksi, vakuutustoiminnan burn n. 200 MUSD p.a.

7 tykkäystä

Tuo n. 200M käytetään asiakashankintaan. Kuten myön Stickström toteaa X:n puolella. LTV/CAC jauhaa hyvää kaikilla rahoilla mitä asiakashankintaan laitetaan.

Mutta mukava nähdä @AP_1981 positiivisia kommentteja! ![]()

4 tykkäystä

Unrivaled Investing päivittänyt Lemonade katsausta. Mielestäni huomioi hyvin mm. Kasvusatsaukset.

3 tykkäystä