The question brought to mind a tangent: for example, in the United States, there are waste management companies that are vertically integrated, meaning they own not only the garbage trucks but also the landfills. In the Helsinki metropolitan area, for instance, the Sortti stations and the Ämmässuo landfill are owned by HSY, a municipal federation.

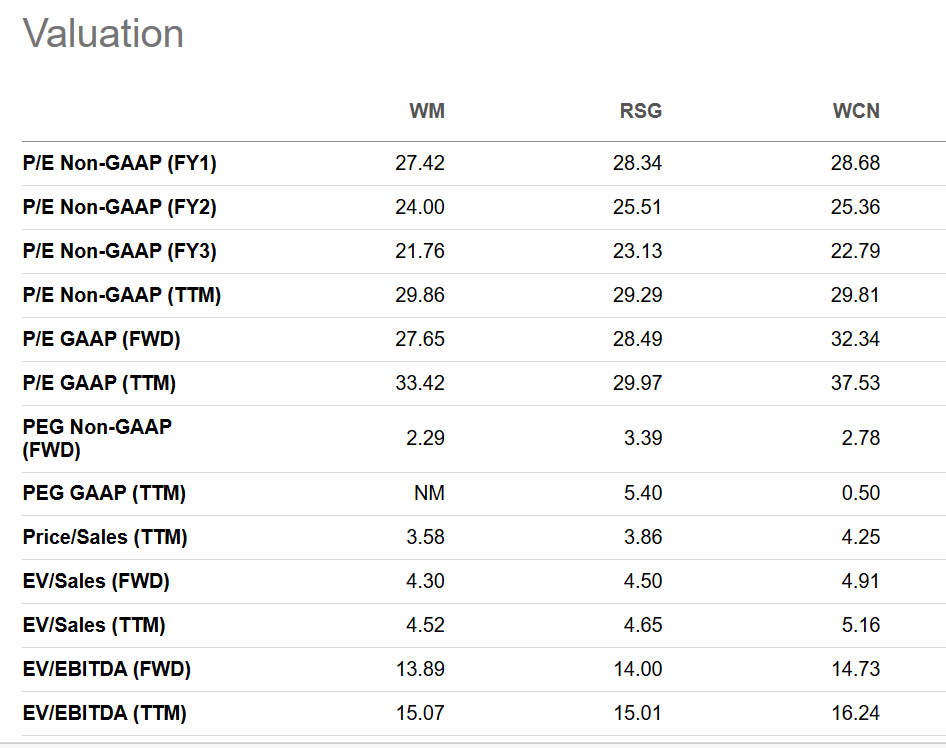

In America, listed companies like Waste Management, Republic Services, and Waste Connections own their landfills and local equivalents of recycling centers, and are indeed categorized as quality stocks rather than value stocks.

As an addition to this – it appears there are two somewhat opposing changes at play here, which Rauli can certainly comment on further – especially point 2).

1) Household and housing company waste management has been steered toward the municipal system (municipality/municipal waste management company) for a long time now.

More obligations will also be added for households and housing companies in the future (e.g., stricter requirements for sorting and recycling).

This has been at the core of the system for quite some time and has limited market-based competition. This has naturally restricted L&T’s growth, as revenues flow to the municipal side.

2) Municipal responsibility is being limited to households, but social and health care (SOTE) facilities, assisted living, etc., are being removed from municipal responsibility. This should bring more business to the private sector, including L&T.

I don’t know how large this market is, but I would imagine that in Finland, social and health care facilities and assisted living are reasonably sized markets and growing as the population ages.

Waste Management, Waste Connection, and Republic Services have been trading at quality company multiples for a very long time already (P/E 20-30x, EV/EBITDA 12-15x).

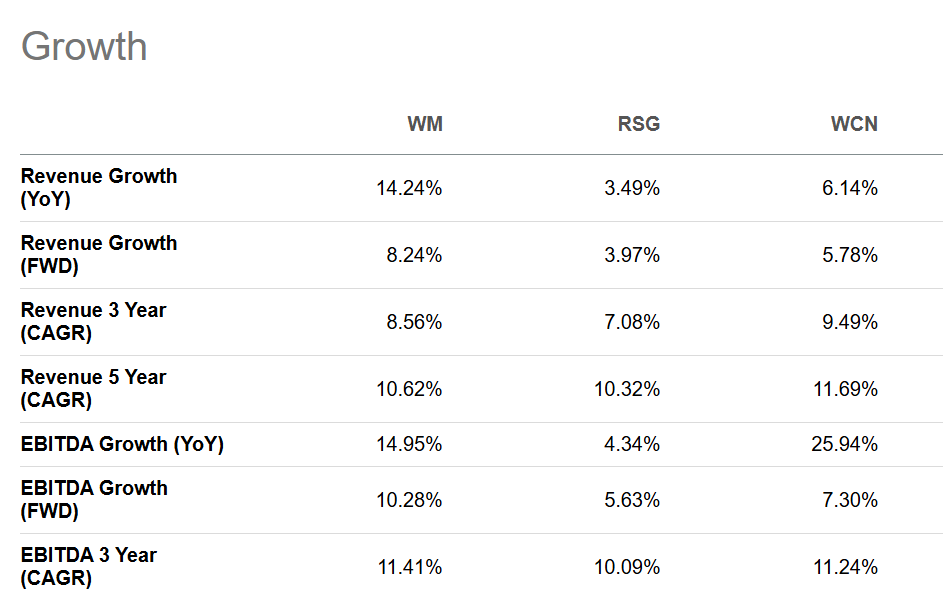

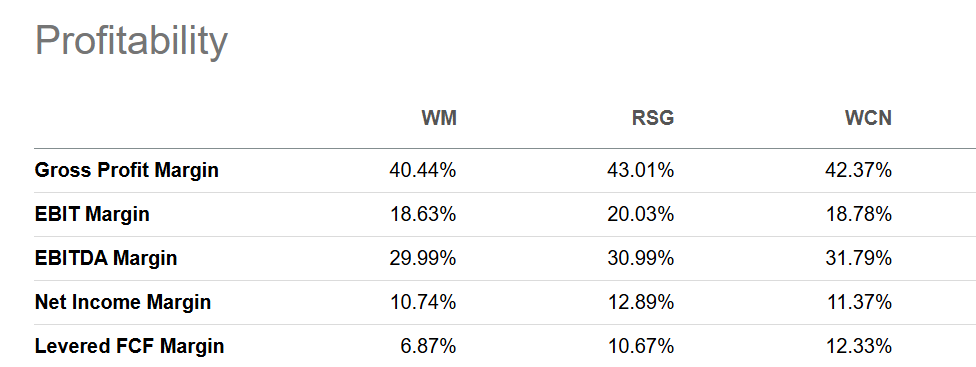

But the fundamentals are also very strong, as you said, and this is reflected in the figures, whether we are talking about growth or profitability. On a completely different level than L&T.

Probably partly why Rauli doesn’t use these as peers.

These companies aren’t actually regulated monopolies; in principle, a competitor could decide to establish a new landfill, but permits are very hard to get. Nobody wants a new landfill in their neighborhood.

Certainly, my apologies if this remained unclear in the comprehensive report.

i) Municipalization means the transfer of waste management for residential properties to be organized by municipalities. The municipality tenders the actual waste management operations. If we consider a property where L&T has previously been responsible for waste management, after municipalization, they can either continue as a subcontractor for the municipality (slightly less revenue because L&T no longer “owns” the waste and lower profitability) or lose the entire business (if someone else wins the tender). Of course, L&T could, on the other hand, win properties previously operated by other actors.

ii) A major change in the Waste Act regarding this already occurred in 2021, and development in this direction also happened before that. However, the effects of the law will come gradually as municipalities take responsibility for properties, and thus effects will still be seen in 2026-27; the biggest impact should already be behind us.

iii) The principle was already outlined above. However, the effect has been fundamentally negative, as municipalization brings deals into strict public price competition. This has led to L&T losing revenue, and we expect this to show a slightly negative impact in 2026-27 as well.

Yes, indeed, this municipalization of households has been an ongoing change for some time, which should be nearing its end. Recently, changes favorable to L&T have been made or planned, for example, as an amendment to the Procurement Act and also in the Waste Act you mentioned. These effects are also expected to appear gradually.

But an optimist could see potential for L&T to grow faster than historical rates/our forecasts from 2027 or 2028 onwards when the overall regulatory effects begin to turn positive. I have forecast rather modest growth, as the company’s growth track is quite modest, and on the other hand, maintaining good profitability will require discipline in price competitions.

Thank you very much, Rauli! This clarified things well.

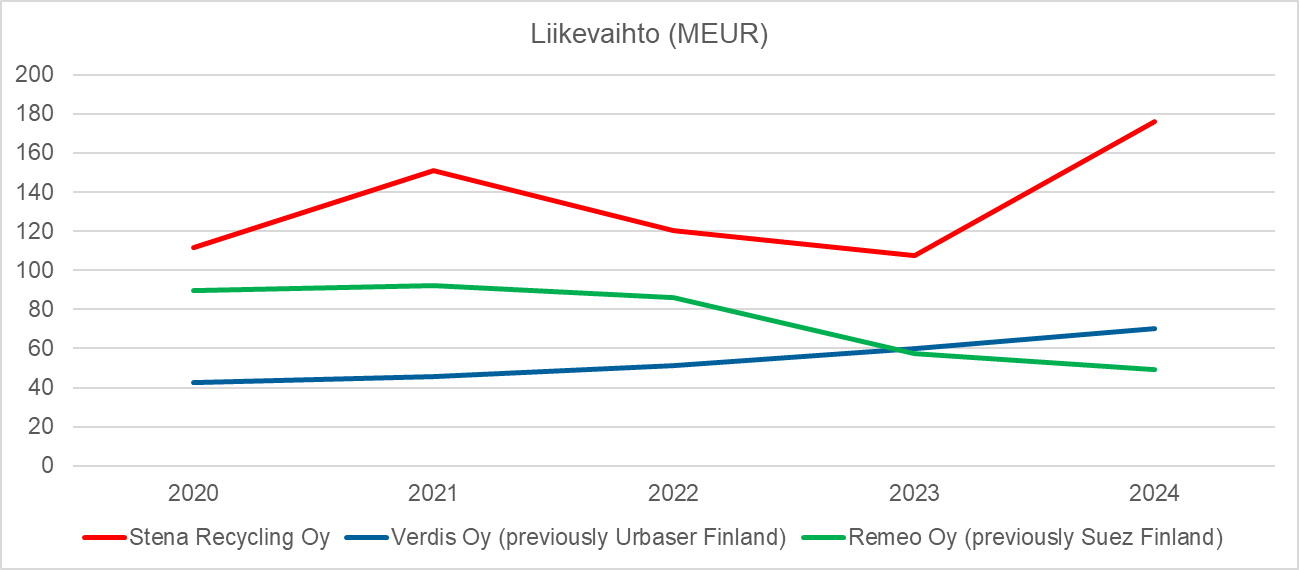

If I may ask one more thing, how would you comment on the environmental services competitors in Finland – especially Verdis and Remeo? Both are private equity/family office owned, but the revenue development of these two competitors has been very different:

Verdis: Revenue has grown from approx. 40 MEUR (2020) → 70 MEUR (2024).

Remeo: Revenue has contracted significantly in 2023-24 (-37 MEUR vs 2022).

I’m wondering if Remeo has perhaps lost some significant municipal contracts while Verdis has gained market share on the corporate side?

Remeo’s figures are a bit messy due to corporate restructurings; as I understand it, there hasn’t been quite such a sharp decline. Verdis has indeed grown significantly and reached decent profitability in 2024 as well. Below is the text regarding Remeo from the initiation report; page 17 also shows the development of waste management competitors in general. I don’t know what types of contracts each has won.

I have to say that those municipal contracts aren’t always even the focus area. Usually, public tenders are rigid and sometimes involve the strangest requirements (there can also be heavy penalties). Public contracts do bring volume, but margins definitely get squeezed low.

Working in the industry, I can say the general feeling is that soon the big players (Remeo, L&T, NG, Stena, Verdis) will start snapping up the smaller ones from the market. This will perhaps lead to a race over who succeeds best. Rumors about the arrival of the German giant Remondis have been circulating for a couple of years now.

General changes expected by 2030:

Less mixed waste (at least as a percentage)

More recycling requirements

More hazardous waste due to classifications

Material-poorer fractions (WEEE / cars etc.)

Emphasis on process transparency and compliance

Customers increasingly demand “real” solutions and are willing to pay