This is a company primarily focused on waste management, recycling, and renewable energy. More about the company in English below.

“The company’s network includes 346 transfer stations, 293 active landfill disposal sites, 146 recycling plants, 111 beneficial-use landfill gas projects and six independent power production plants. Waste Management offers environmental services to nearly 21 million residential, industrial, municipal and commercial customers in the United States, Canada and Puerto Rico. With 26,000 collection and transfer vehicles, the company has the largest trucking fleet in the waste industry”

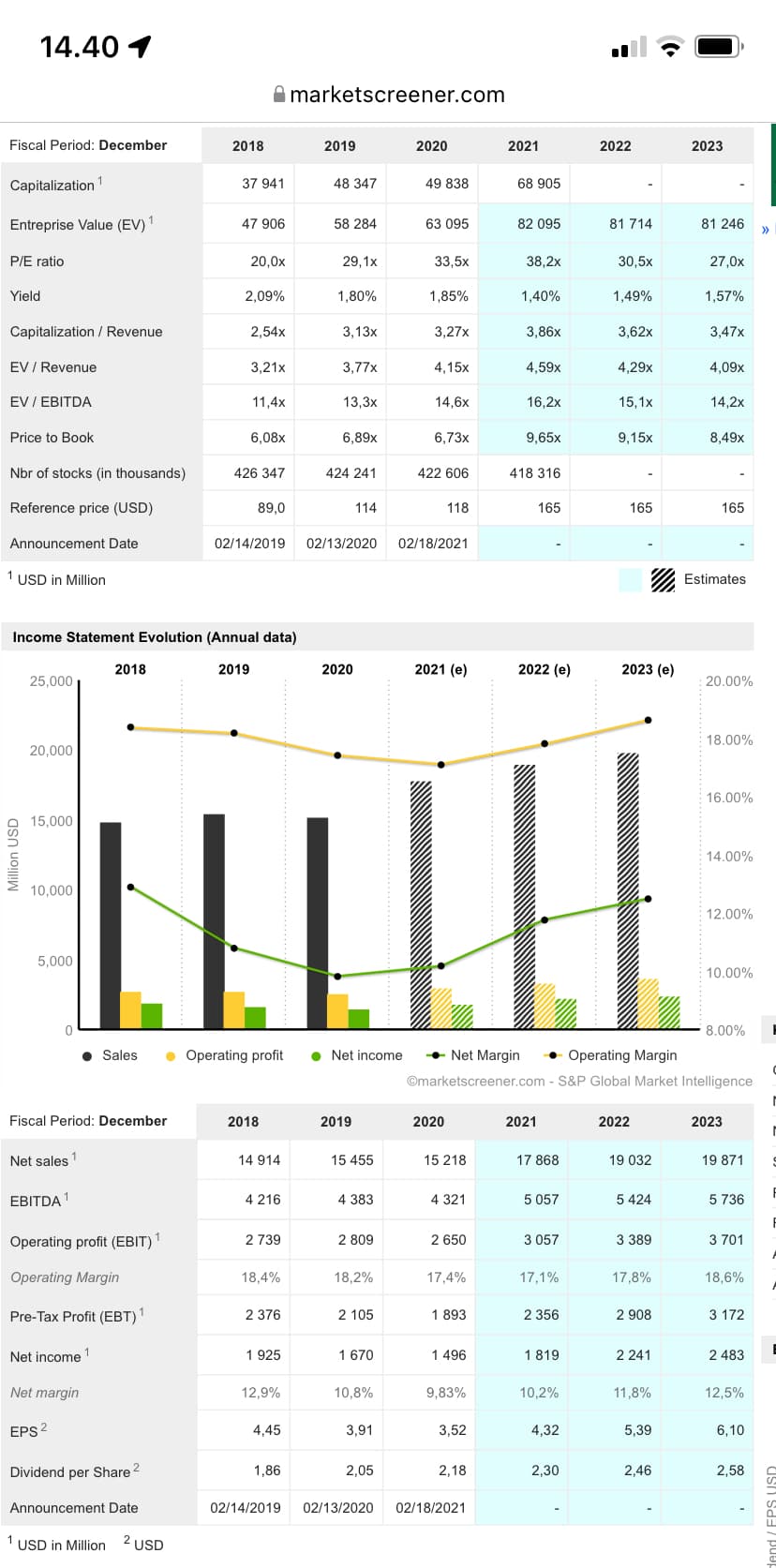

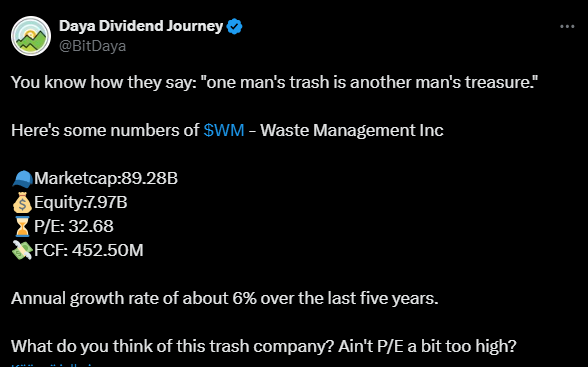

Isn’t this the American Lassila & Tikanoja? Undoubtedly, the American company is probably a much better managed company in this comparison, but at least my own choice, based on valuation, has been the domestic alternative:

L&T:

P/E 15

Forward P/E 14

DY 4%

In addition, Lassila’s EV/Sales is about 0.85, while the same figure for Waste Management is about 4.5! The American company therefore makes a huge amount of higher margin relative to sales. Or is WM’s business fundamentally different from L&T’s?

The stock’s return curve is impressive, but it’s almost entirely due to rising multiples while earnings growth has been weak. I’ve been glancing at it regularly now and then, but the multiples just don’t make any sense.

Waste Management just published its latest results and plans for the coming year.

The company achieved strong growth and significantly improved its profitability, especially concerning its core business and waste management services. The company has streamlined the integration of the Stericycle acquisition and significantly raised its savings targets.

Operational efficiency is also reflected in the cost structure and automation, thanks to which the company has reduced staff turnover + improved the profitability of waste processing. So-called “sustainability investments,” such as biogas plants and technological improvements in recycling, are already generating clear added value.

This year, the goal is to continue growth, optimize business operations, and strengthen its financial position.

WM had a strong start to the year, and the company reported succeeding in its strategic goals.

Revenue growth and cost efficiency improved in the core business, while investments in sustainability projects progressed, and new business related to healthcare services developed as expected. Waste Management has acquired parts of Stericycle’s business, particularly operations related to healthcare waste and secure information destruction, and this integration has proceeded excellently.

The company is confident in achieving its set 2025 targets.

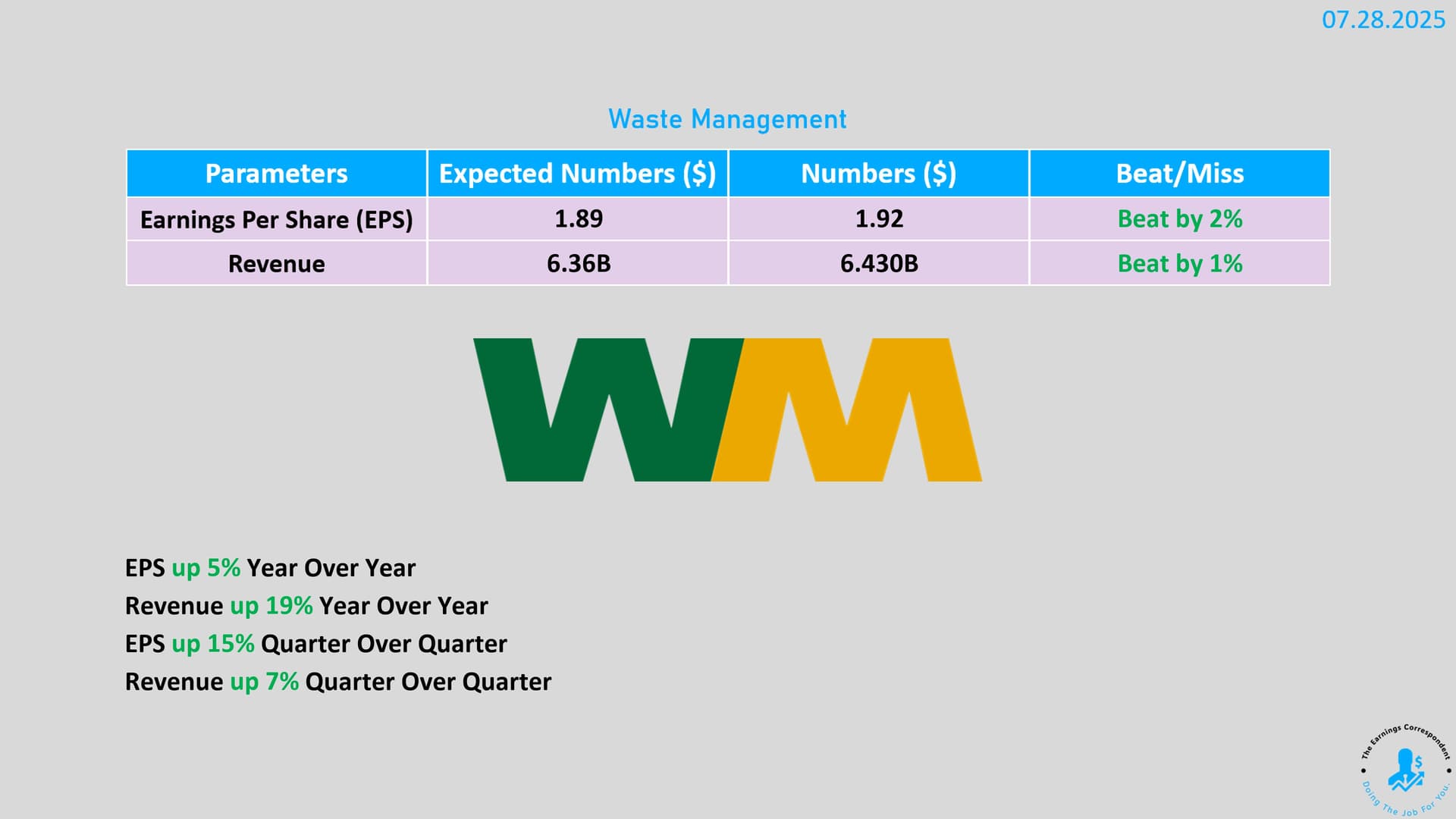

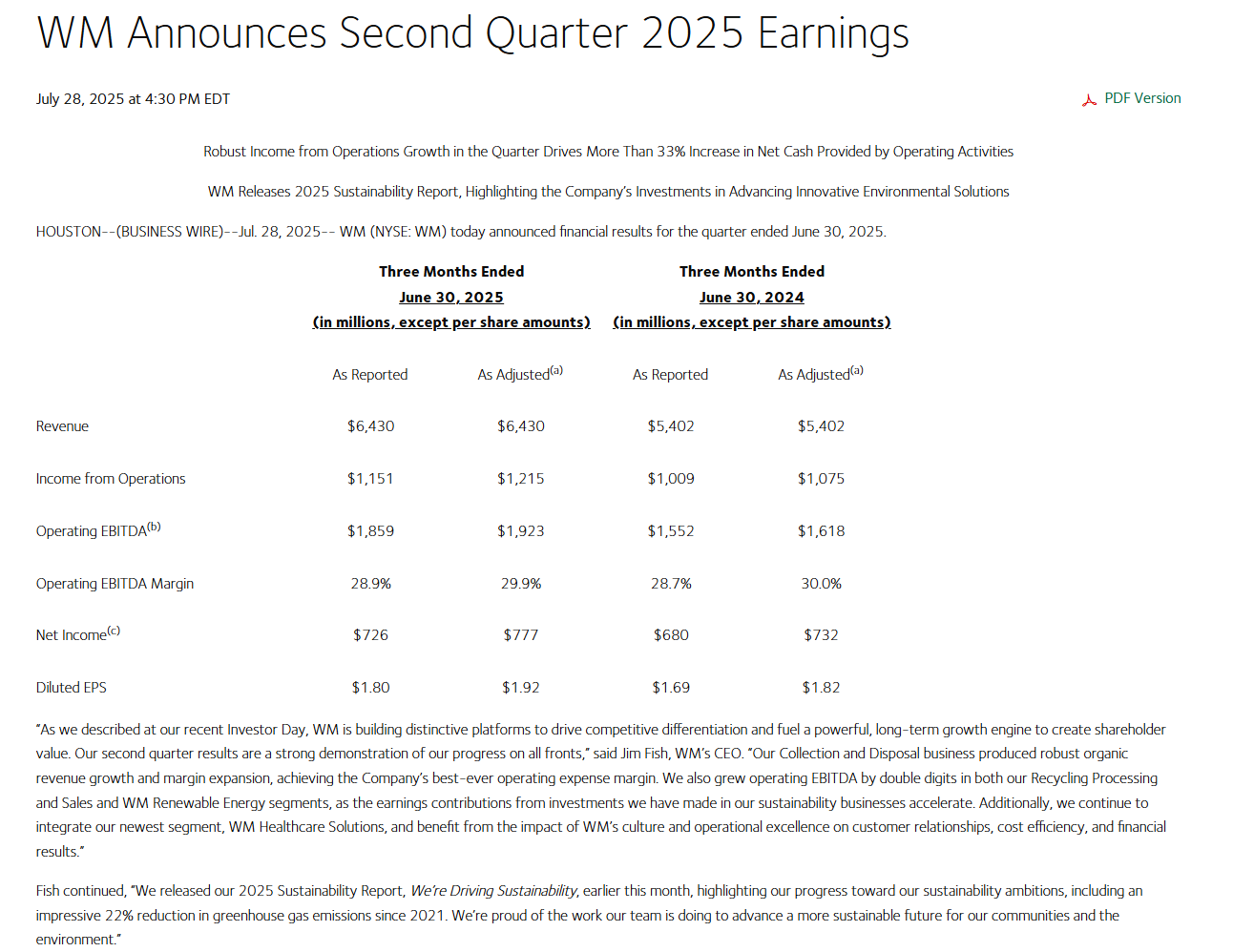

Waste Management reported a strong second quarter, exceeding both earnings and revenue expectations. Revenue grew significantly year-over-year, driven particularly by core businesses such as waste collection and processing.

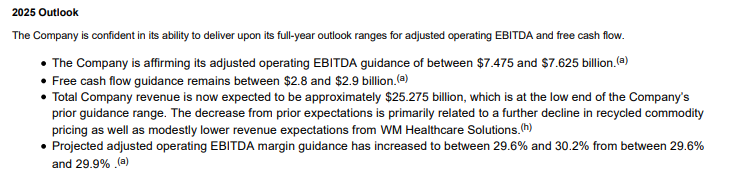

The company slightly lowered its full-year revenue forecast due to severe early-year weather and low recycling prices, but profitability outlook remained strong.

The company refined its EBITDA target upwards and raised its free cash flow guidance due to tax benefits, whatever those may have been.

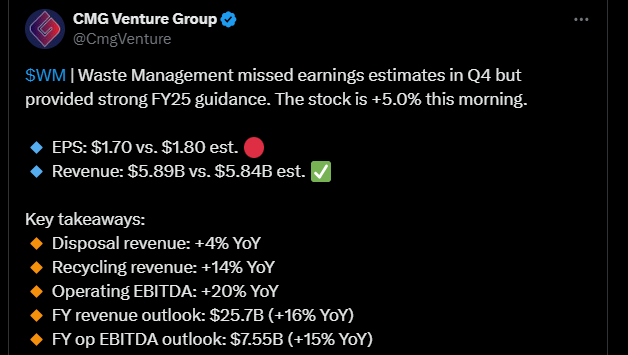

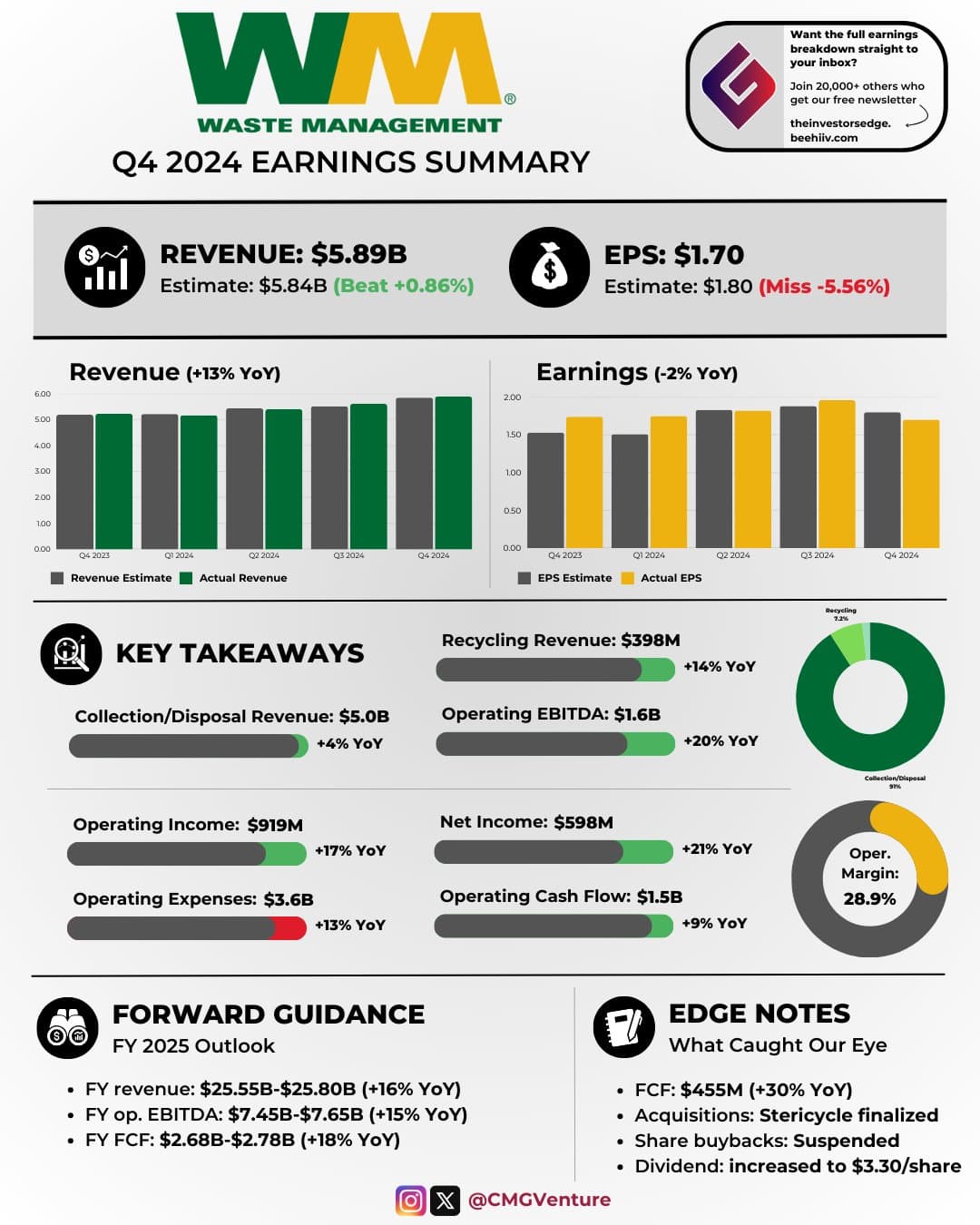

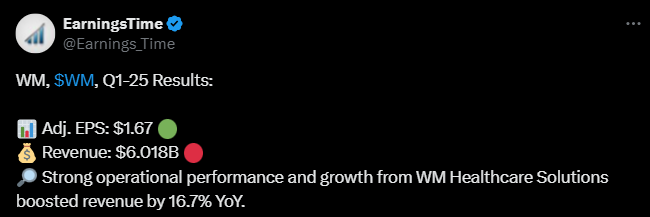

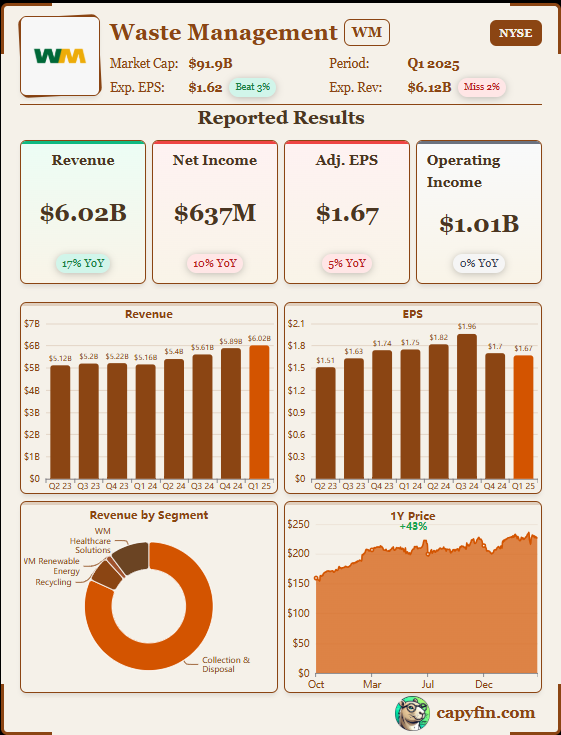

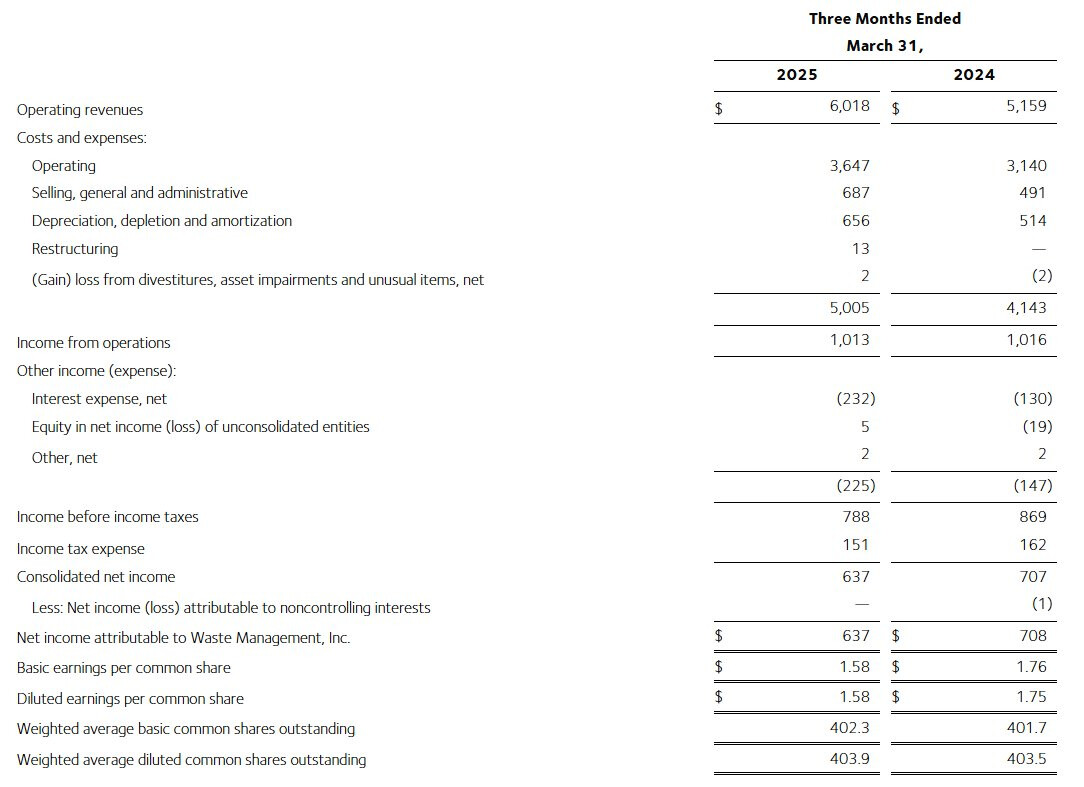

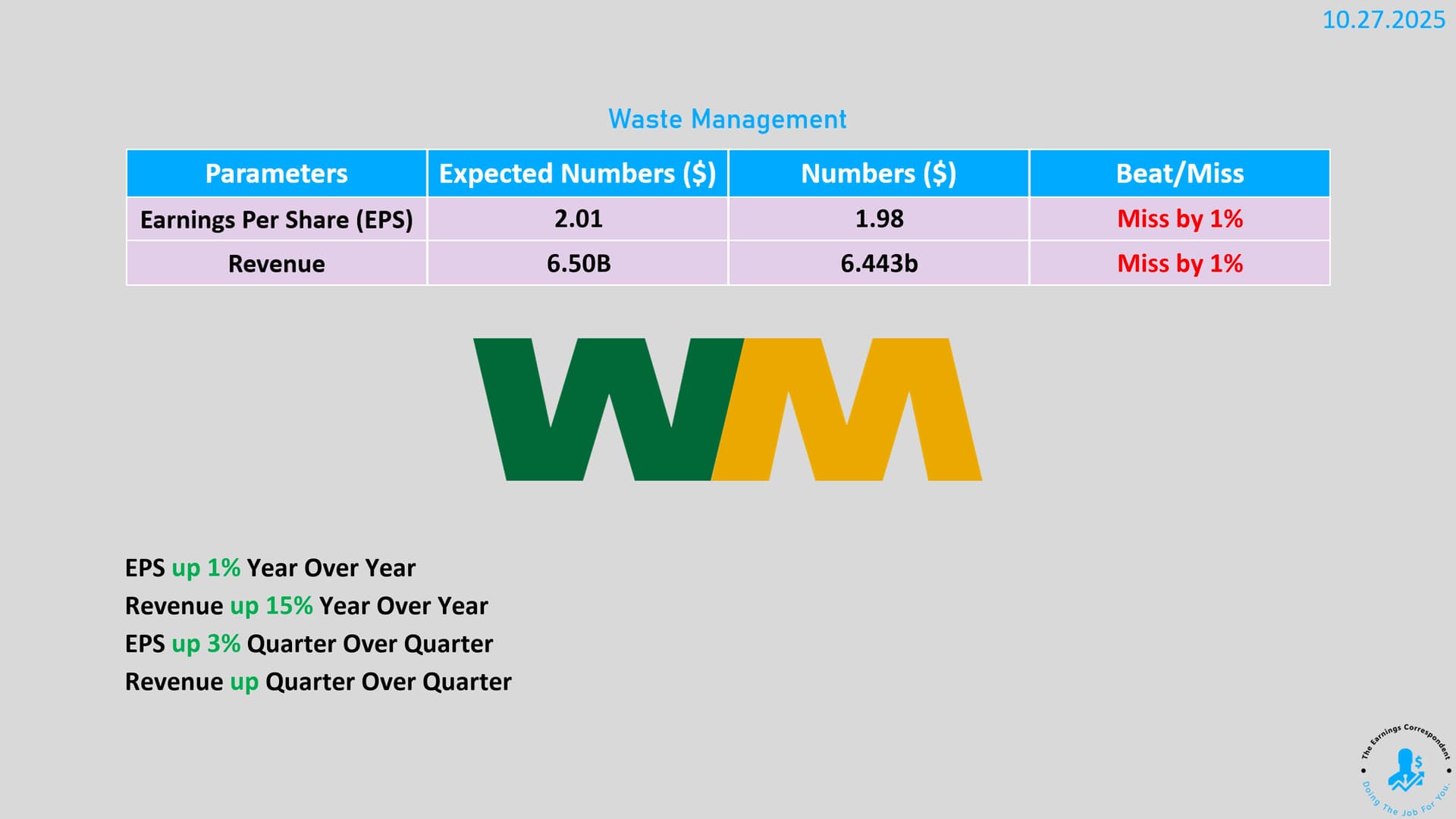

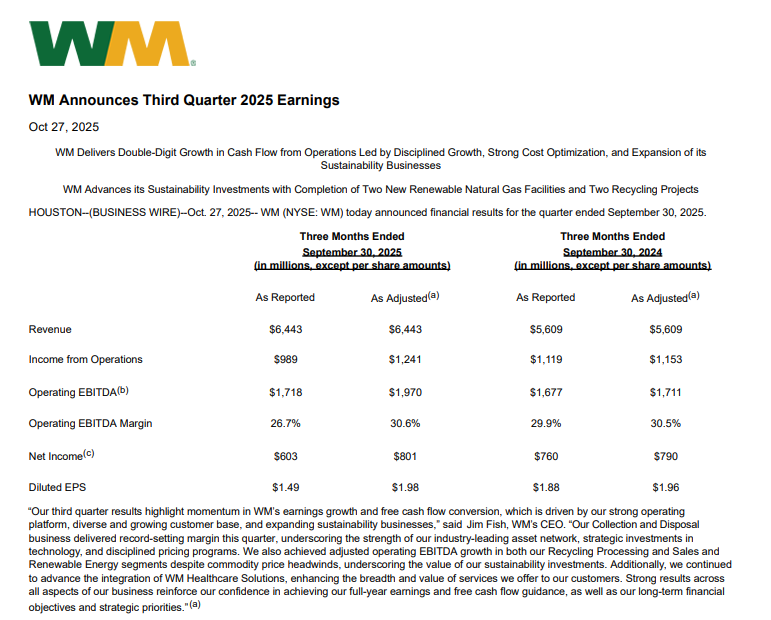

Waste Management reported its results; earnings and revenue fell slightly short of market expectations, but both still grew from the previous year.

The company continues to show stable performance, supported by demand for waste management. A slight dip compared to forecasts does not shake the overall picture of steady and predictable growth, but it is a small disappointment for the market… as of this writing, down about 3 percent.