Kysymyksestä tuli tangenttina mieleen että esim. Yhdysvalloistahan löytyy jätehuoltoyhtiöitä jotka ovat vertikaalisesti integroituneita eli omistavat paitsi roska-autot, myös kaatopaikat. Esim. pk-seudulla Sortti-asemat ja Ämmässuon kaatopaikan omistaa HSY eli kuntayhtymä.

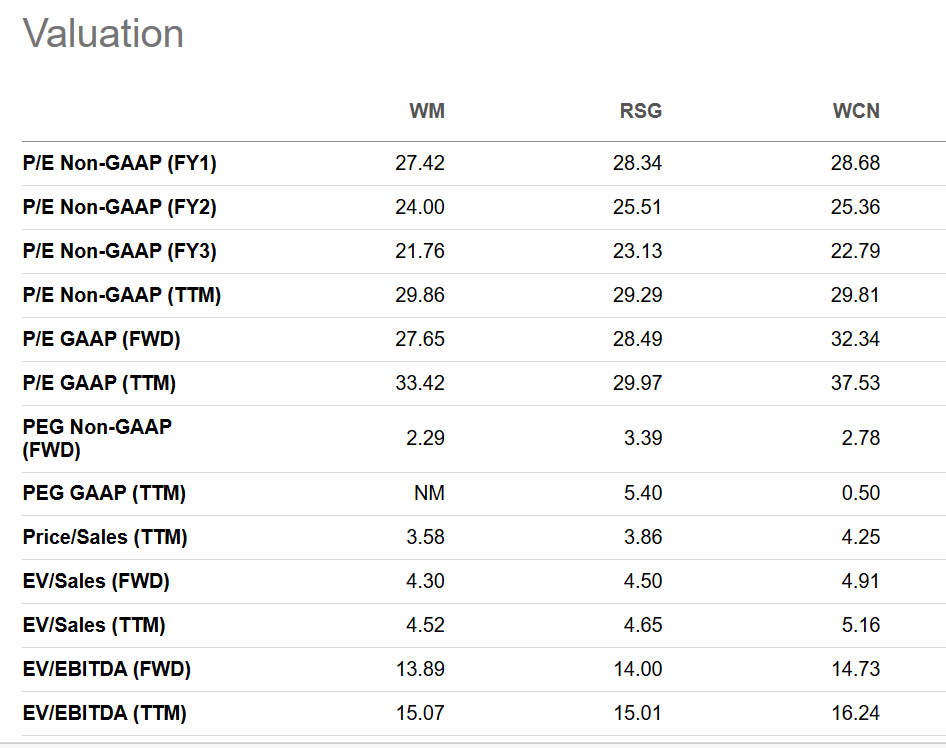

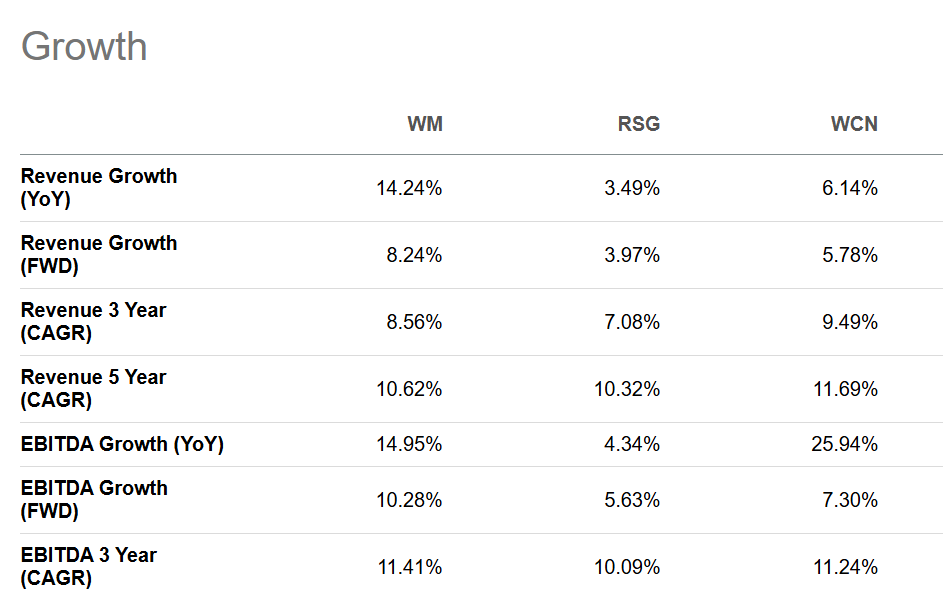

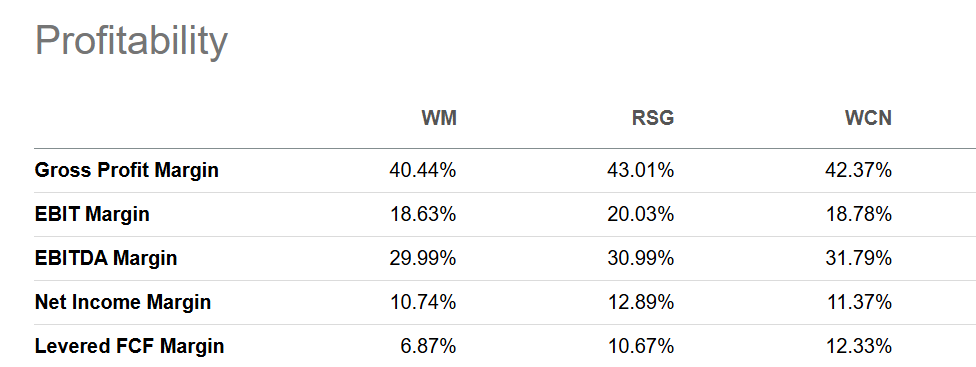

Amerikassa pörssiyhtiöt kuten Waste Management, Republic Services ja Waste Connections omistavat kaatopaikkansa ja paikalliset sortti-asemien vastineensa ja ovatkin laatu- eivätkä arvoyhtiölaarissa.

Täydennyksenä vielä tähän - tässä on nyt ilmeisesti kaksi hieman vastakkaista muutosta kyseessä, jota toki Rauli voi sitten kommentoida lisää - etenkin 2) kohta.

1) Kotitalouksien ja taloyhtiöiden jätehuoltoa on ohjattu jo pidemmän aikaa enemmän kunnalliseen järjestelmään (kunta/kunnallinen jätehuoltoyhtiö).

Kotitalouksille ja taloyhtiöille lisätään myös tulevaisuudessa enemmän velvoitteita (esim. tiukemmat vaatimukser lajittelulle ja kierrätykselle).

Tämä on ollut järjestelmän ydin jo pidemmän aikaa ja rajoittanut markkinaehtoista kilpailua. Tämä on luonnollisesti rajoittanut L&T:n kasvua, koska tulot virtaavat kuntapuolelle.

2) Kuntien vastuuta rajoitetaan kotitalouksiin, mutta sote-laitokset, palveluasuminen jne. poistuvat kuntavastuusta. Tämän pitäisi tuoda enemmän bisnestä yksityiselle sektorille mukaan lukien L&T.

En tiedä kuinka suuri tämä markkina on, mutta kuvittelisin että Suomessa sote-laitokset ja palveluasuminen ovat kohtuullisen kokoisia markkinoita ja kasvavia väestön vanhetessa.

Nämä yhtiöthän eivät ole varsinaisesti säänneltyjä monopoleja vaan periaatteessa joku kilpailija voisi päättää perustaa uuden kaatopaikan mutta lupia on hyvin vaikeaa saada. Kukaan ei halua naapuriinsa uutta kaatopaikkaa.

Toki, pahoittelut jos tämä on jäänyt epäselväksi laajassa raportissa.

i) kunnallistaminen tarkoittaa asuinkiinteistöjen jätehuollon siirtymistä kuntien järjestettäväksi. Kunta kilpailuttaa varsinaisen jätehuollon operoivan. Jos ajatellaan kiinteistöä jossa L&T on aiemmin ollut vastuussa jätehuollosta, niin kunnallistamisen jälkeen he voivat joko jatkaa kunnan alihankkijana (vähän vähemmän liikevaihtoa koska L&T ei enää “omista” jätettä ja heikompi kannattavuus) tai menettää koko busineksen (jos joku muu voittaa kilpailutuksen). Toki L&T voi toisaalta voittaa aiemmin muiden toimijoiden operoimia kiinteistöjä.

ii) Iso muutos jätelaissa tämän suhteen tapahtui jo 2021 ja kehitystä tähän suuntaan oli myös sitä aiemmin. Lain vaikutukset kuitenkin tulevat asteittain kun kunnat ottavat kiinteistöjä omalle vastuulleen ja siksi vaikutuksia nähdään vielä 2026-27, suurin isku pitäisi olla jo takana.

iii) Periaate tulikin jo tuossa yllä. Vaikutus on kuitenkin ollut lähtökohtaisesti negatiivinen, kun kunnallistaminen tuo diilit tiukkaan julkiseen hintakilpailuun. Eli tämän myötä L&T on menettänyt liikevaihtoa ja odotamme tämän näkyvän myös 2026-27 lievästi negatiivisena.

Joo, tosiaan tämä kotitalouksien kunnallistaminen on jo pidempään käynnissä ollut muutos, jonka pitäisi olla lopuillaan. Viime aikoina on tehty tai suunniteltu muutoksia L&T:lle myönteiseen suuntaan mm. hankintalain muutoksena ja myös tuossa mainitsemassasi jätelaissa. Nämäkin vaikutukset näkyvät oletettavasti asteittain.

Mutta optimisti voisi nähdä tuossa L&T:lle potentiaalia historiallista/meidän ennusteita kovempaan kasvuun 2027 tai 2028 lähtien kun regulaatiovaikutukset kokonaisuutena alkaa kääntymään positiiviseksi. Olen ennustanut aika maltillista kasvua, kun firman kasvuträcki on aika vaatimaton ja toisaalta hyvän kannattavuuden säilyttäminen vaatinee kuria hintakisoissa.

EDIT, tämä jäi vastaamatta:

Enpä osaa tarkasti sanoa tuon markkinan kokoa, muistaakseni yleisesti firma sanoi marraskuun CMD:llä ettei mitään yksittäistä regulaatiomuutosta ole näköpiirissä joka toisi merkittävää hyppyä kasvuun. Koko markkinallehan yhtiö arvioi 3 % vuosittaista kasvua vuosikymmenen lopun ja meidän ennusteissa on 2 % eli voisi sanoa että ei ole mitään merkittävää uutta markkinaa L&T:n osalta. Mutta nämä on ehdottomasti jätehuollon kannalta tärkeitä markkina-ajureita eli pidetään niitä kyllä silmällä.

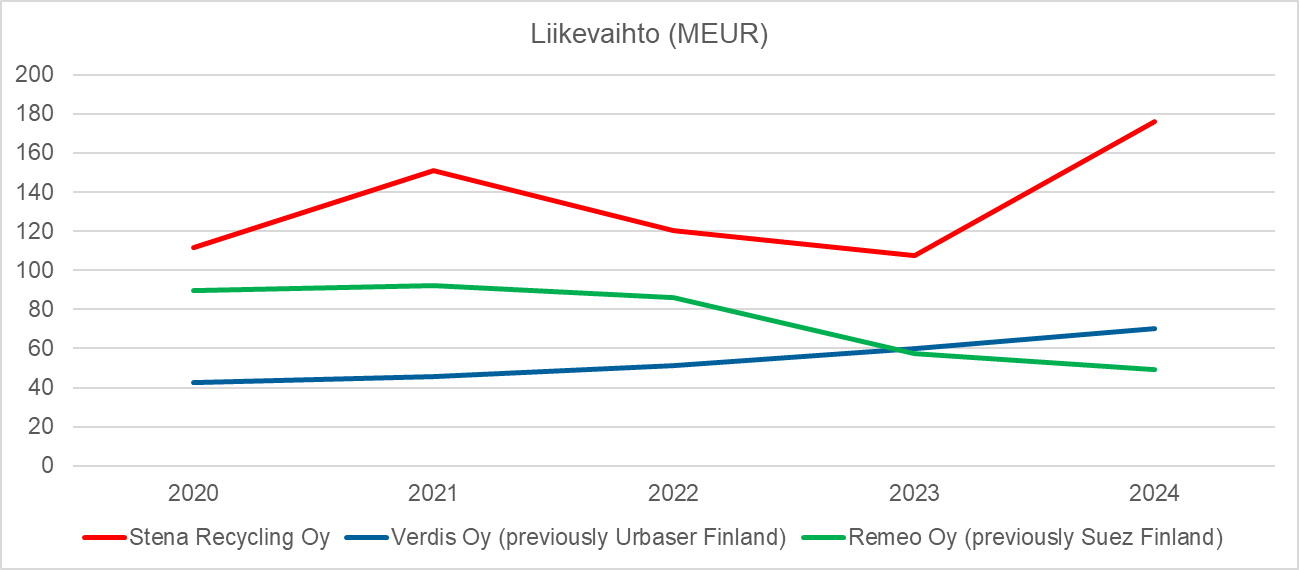

Jos voin vielä kysyä niin miten kommentoisit ympäristöpalveluiden kilpailijoita Suomessa - etenkin Verdis ja Remeo. Molemmat ovat private equity/office omisteisia, mutta näiden kahden kilpailijan liikevaihdon kehitys on ollut hyvin erilaista:

Verdis: Liikevaihto kasvanut n. 40 MEUR (2020) → 70 MEUR (2024).

Remeo: Liikevaihto supistunut huomattavasti 2023-24 (-37 MEUR vs 2022).

Mietin, että onko Remeo kenties hävinnyt joitakin merkittäviä kuntasopimuksia kun taas Verdis on ottanut markkinaosuutta yrityspuolella?

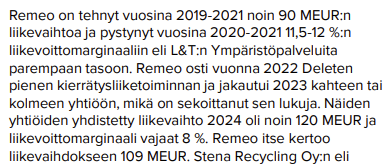

Remeon luvut on vähän sekavat yritysjärjestelyjen myötä, käsitykseni mukaan ihan noin kovaa laskua ei ole ollut. Verdis on tosiaan kasvanut reippaasti ja päässyt kelpo kannattavuutenkin 2024. Alla teksti Remeon osalta laajasta, sieltä sivulta 17 löytyy jätekilpailijoiden kehitystä muutenkin. Sitä en tiedä minkätyyppisiä sopimuksia kukin on voittanut.

Täytyy sanoa että nuo kuntasopimukset eivät ole aina edes se fokus alue. Yleensä julkiset kilpailutukset kankeita ja välillä mitä erikoisimpia vaateita (myös keppiä voi tulla rajusti). Julkiset sopimukset tuo kyllä volyymia, mutta katteet painuu kyllä matalalle.

Alalla työskentelevänä voin sanoa yleisesti fiiliksen olevan että pian isot (Remeo, L&T, NG, Stena, Verdis) ryhtyvät napsimaan pieniä markkinoilta. Tässä tulee ehkä sitten kisa siitä kuka onnistuu parhaiten. Saksan jättiläisen Remondiksen saapumista on huhuttu jo parisen vuotta.

Mitä muutoksia yleisesti odotetaan 2030 mennessä:

Sekajätettä vähemmän (ainakin %-osuudelta)

Kierrätysvaatimuksia lisää

Vaarallista jätettä enemmän johtuen luokituksista

Jakeet materiaaliköyhempää (SER / autot yms)

Prosessien läpinäkyvyys ja asianmukaisuus korostuu

Asiakkaat kaipaavat entistä enemmän “oikeita” ratkaisuja ja ovat valmiita maksamaan

L&T-sijoittajien on oltava jätehuollon ystäviä joten rohkenen laittaa ketjuun tämän tuoreen videon japanilaisen Chigasakin kaupungin (240,000 asukasta) jätehuoltolaitoksen roskakuskin tavallisesta työpäivästä :

Valtaosa Japanin väestöstä asuu tiiviisti rakennetuissa kaupungeissa joissa roska-autot keräävät säntillisesti lajiteltua jätettä lyhyillä reiteillä ja kapeilla kaduilla - siksi monet roska-autot ovat siellä pieniä. Koska väentiheys on suuri, keräysasemat ovat tiheässä. Sekajäte yleensä poltetaan.

Liikevaihto oli 94,8 miljoonaa euroa (89,4). Liikevaihto kasvoi 6,0 %.

Oikaistu EBITDA oli 11,5 miljoonaa euroa (12,8), joka oli 12,1 % (14,3) liikevaihdosta

Oikaistu EBITA oli 0,2 miljoonaa euroa (2,6), joka oli 0,3 % (2,9) liikevaihdosta. Kannattavuutta heikensivät jätehuollon volyymin lasku, polttoaineiden hinnannousu sekä kasvaneet poistot.

Liikevoitto oli -0,8 miljoonaa euroa (3,5), joka oli -0,9 % (3,9) liikevaihdosta.

Osakekohtainen tulos oli -0,01 euroa (0,11). Osakekohtainen tulos ei ole vertailukelpoinen vuosien välillä, koska esimerkiksi yhtiön ulkoisia lainoja ja näihin liittyviä nettorahoituskuluja ei ole sisällytetty vuoden 2025 carve-out -taloudellisiin tietoihin.

Liiketoiminnan rahavirta investointien jälkeen oli -3,2 miljoonaa euroa (3,6). Rahavirtaa heikensivät osittaisjakautumiseen liittyvien, Lassila & Tikanojan ja Luotea Oyj:n välisten erien maksut, yhteensä 6,9 miljoonaa euroa. Edellä mainitut seikat huomioiden liiketoiminnan rahavirta investointien jälkeen pysyi edellisvuoden tasolla.

Eero mainitsee tämän katsauksessa: “Tammi-maaliskuun kannattavuutta rasittivat jätehuollon volyymien laskun lisäksi polttoaineiden hinnannoususta johtunut n. 0,5 miljoonan euron kustannusten kasvu edellisvuoteen verrattuna” . Pieneltähän tuo vaikuttaa, mutta onhan heillä osa kalustosta sähköistetty.

Sähkökin oli Q1 kallista Sen hinnannousulla toki häviävän pieni merkitys kun ei niitä sähköautojakaan vielä paljon ole suhteessa polttomoottorikaluston määrään.

L&T:n Q1-tulos jäi odotuksistamme ja vertailukaudesta. Yhtiö toisti koko vuoden ohjeistuksen, mutta tulosennusteemme laski sen alalaitaan. Arvostus on mielestämme defensiiviselle ja tasaiselle liiketoiminnalle edullinen (oik. P/E ja EV/EBIT noin 10x). Matalan arvostuksen lisäksi tuotto-odotusta tukevat arvioissamme tuloskasvu, osinkotuotto sekä L&T:n mahdollinen päätyminen yrityskaupan kohteeksi. Toistamme osta-suosituksen, mutta laskemme tavoitehinnan 8,5 euroon (8,6e).

Pari muuta reaktiota tulokseen Kauppalehden pikauutisista: OP Pohjola laskee Lassila&Tikanojan suosituksen vähennä-tasolle (aik. lisää) ja laskee tavoitehinnan 7,10 euroon (aik. 8,30 eur.)

Danske Bank laskee Lassila&Tikanojan tavoitehinnan 8,50 euroon (aik. 9,00 eur.)

Sainkin tuossa yksityisviestillä tietoa, että OP näkee ohjeistusriskiä eli mahdollinen tulosvaroitus loppuvuonna. @Rauli_Juva ei tainnut sitä suoraan liputtaa, vaikka ennusteet ohjeistuksen alalaidalla ovatkin.

Eipä tullut tosiaan kirjoitettua tuota, mutta selvähän se on, että riski on ihan huomattavakin, kun ennuste on ihan haarukan alareunassa. En usko että yhtiön omakaan arvio on enää rangen keskikohdassa, kun Eero selvästi mainitsi markkinanäkymän heikentyneen helmikuusta (jolloin ohjeistus annettiin) jonka lisäksi dieselin noususta tulee 0,5-1,0 MEUR hittiä (kun Q2:n alkuun tullee myös sen Q1:n 0,5 MEUR:n lisäksi).