Someone has wanted to secure money for Christmas presents early, based on today’s sales. Or could it, however, be securing funding for Father’s Day?

1 Like

Here are Rauli’s pre-comments, as L&T has its Capital Markets Day on Wednesday. ![]()

L&T is organizing a Capital Markets Day on Wednesday, where it will present the two companies planned to be demerged at the turn of the year, namely Luotea and the new Lassila & Tikanoja. The financial targets and strategies of the new companies have already been published. Thus, the day will mainly focus on presenting the targets and operations of the new companies in more detail, and we do not expect significant news.

4 Likes

Here are Rauli’s thoughts from L&T’s Capital Markets Day. ![]()

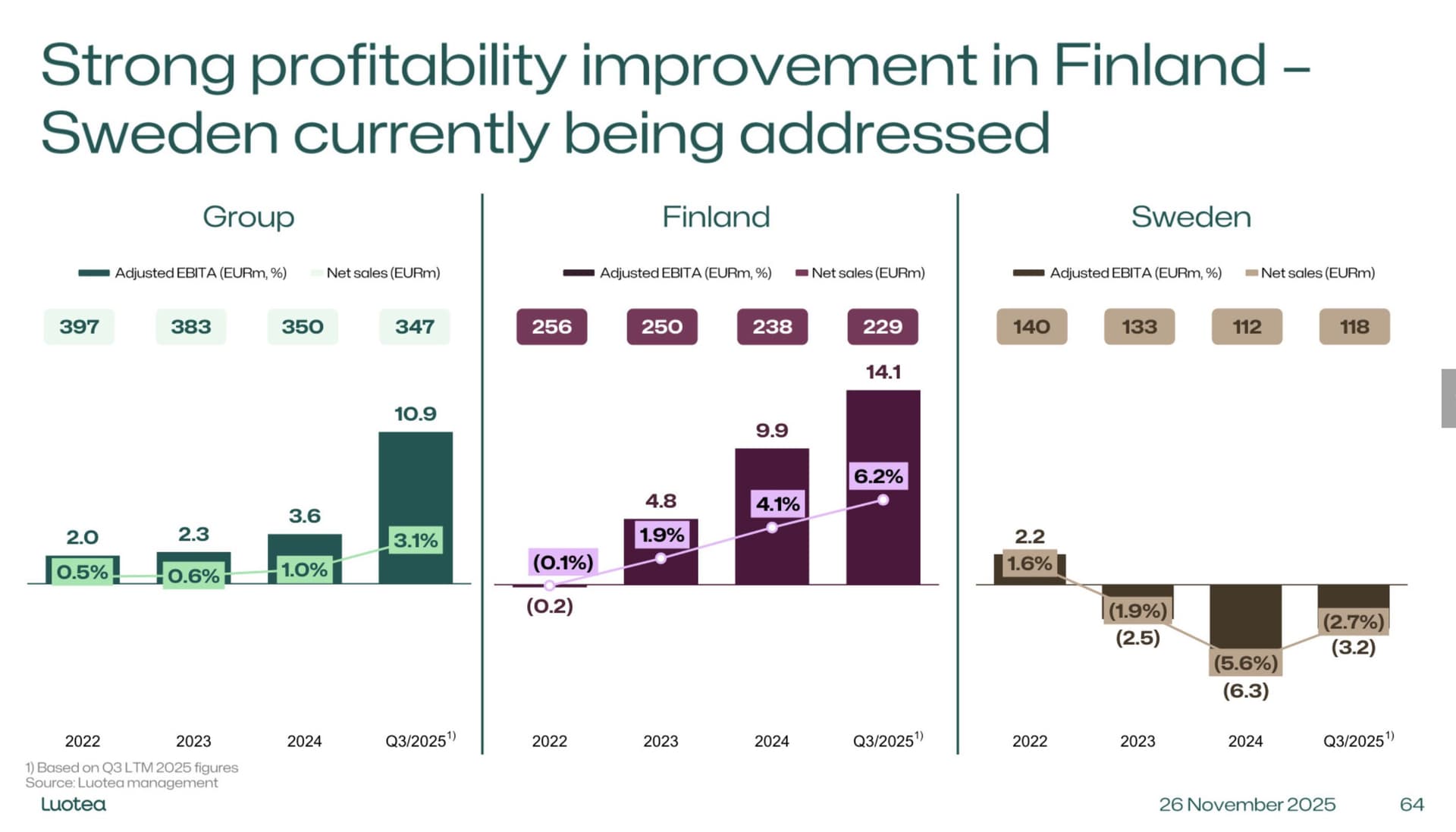

L&T held a Capital Markets Day yesterday, where it presented the two companies planned to be demerged at the turn of the year: Luotea and the new Lassila & Tikanoja. The financial targets and strategies for the new companies had already been published, so the day did not offer significant news. Regarding next year’s outlook, some additional clarity was provided for both companies, but these were also in line with our expectations. Thus, the day does not necessitate any forecast changes, although we will naturally assess the impact of the demerger on the company when it likely takes place at the turn of the year.

3 Likes

“Regarding acquisitions, the Swedish market, in particular, offers great potential”

Next company going to fail in Sweden? =S

Well, let’s hope for the best and fear the worst.

2 Likes

To clarify, acquisitions in Sweden are specifically sought by the “new L&T”, and they entered that market a couple of years ago with a so far successful acquisition. And by potential, I was referring to market size; it did not take a stance on value creation ![]()

Sweden’s losses, on the other hand, are on the side of the upcoming Luotea (which also has its roots in an acquisition). Fortunately, Luotea is not dreaming of acquisitions in the near future, especially not in Sweden, but not elsewhere either.

6 Likes

Here are Juha Varis’s highlights, which probably fit well into this thread. Of course, at least some of it is familiar to many. ![]()

https://x.com/JuhaVaris/status/1994688655143670010

8 Likes

So today an extraordinary general meeting, where the separation of the companies is expected to be approved, meaning one will become two even better companies ![]() , link to the webcast of the meeting starting at 4:00 PM: Lassila & Tikanoja ylimääräinen yhtiökokous 2025 - Inderes

, link to the webcast of the meeting starting at 4:00 PM: Lassila & Tikanoja ylimääräinen yhtiökokous 2025 - Inderes

8 Likes

In such demergers, is the acquisition cost or distribution ratio determined by the tax authority known when trading begins? In other words, is it possible to account for taxation if one continues as an owner of only one of the companies? The markets can price the new shares very differently from the tax authority, or how does this work?

1 Like

Generally, the tax acquisition cost is determined by the ratio of the net assets transferred to the demerged companies. If the fair values differ significantly from the distribution of net assets, the ratio of fair values can be used.

In the case of listed companies, the tax authority usually publishes the applicable ratios for determining acquisition costs a few months after the demerger.

Example Sampo/Mandatum: Sampo Oyj:n osittaisjakautumisessa syntyneen Mandatum Oyj:n ja Sampo Oyj:n osakkeiden hankintamenon määrittäminen verotuksessa - vero.fi

Example Cargotec (Hiab)/Kalmar: Cargotec Oyj:n osittaisjakautumisessa syntyneen Kalmar Oyj:n ja Cargotec Oyj:n osakkeiden hankintamenon määrittäminen verotuksessa - vero.fi

6 Likes

Here is the stock exchange release concerning the demerger decision, which was made as expected by the extraordinary general meeting:

4 Likes

I made a deep-dive on the upcoming demerger - Lassila & Tikanoja and Luotea, respectively. Happy to hear your thoughts!

17 Likes

Thanks for the great summary!

I am expecting M&A activity following the split and it is an obvious step to raise the value of both.

2 Likes

Here are Rauli’s comments regarding the confirmation of L&T’s demerger, among other things. ![]()

Lassila & Tikanoja announced yesterday that its Board of Directors has decided to carry out a partial demerger of the company. We view the news as an expected confirmation of a process that has been ongoing throughout the year. The demerger will take effect at the turn of the year, and trading in the separated companies will begin on January 2, 2026. Naturally, we will take the demerger into account in our analysis once it has been implemented. We have already tentatively assessed the value of the demerging companies in our previous analyses.

5 Likes

A new company appeared on the stock exchange today under the name Lassila & Tikanoja (which spun off from Lassila & Tikanoja, how else ![]() ). We’ve got this split-off company under coverage right from the start, and attached is the comprehensive initiation report. The business operations are, of course, the same as those covered in previous L&T deep dives, but the company has provided information in a slightly new way in connection with the demerger. Nothing revolutionary in my opinion, though, and information has been coming out gradually since last summer.

). We’ve got this split-off company under coverage right from the start, and attached is the comprehensive initiation report. The business operations are, of course, the same as those covered in previous L&T deep dives, but the company has provided information in a slightly new way in connection with the demerger. Nothing revolutionary in my opinion, though, and information has been coming out gradually since last summer.

The recommendation for the new L&T is Accumulate.

Today we also published an update on Luotea, which technically continues “on the foundation” of the old L&T, and the recommendation there is also Accumulate. It would probably be good to start a dedicated thread for it; I already tried, but the 500-word requirement for the opening post was too much, as I didn’t want to just copy-paste the report directly ![]()

A keen reader may notice that in the demerger, the target price for the two new companies is somewhat higher than for the previous L&T, and the outlook has also turned positive. Having looked at these splitting companies more closely and partly from a clean slate during December, I believe this was the right outcome. Thus, the demerger seems to clarify the value/potential of both in our eyes. Especially the new L&T clearly has the potential to also become an acquisition target.

I’m now going on vacation for a week, so if any discussion arises regarding these split companies, I’ll get back to it once I return.

27 Likes

Thread for Luotea has been opened. The opening post is still relatively concise, but the essential info and links can be found there.

https://forum.inderes.com/t/luotea-oyj-kiinteistopalveluita-tarjolla/71569

14 Likes

Not a big deal, but in the analysis, “DCF value sensitivity to changes in WACC %” doesn’t match the DCF calculation.

2 Likes

Linking the video filmed with Rauli about the new L&T here as well.

”The circular economy company Lassila & Tikanoja, formed as a result of a partial demerger, is hungry for growth in light of its stable business. Companies’ increasing recycling needs and L&T’s stable cash flow enable growth, but history has shown that achieving profitable growth is challenging.”

Topics:

00:00 Introduction

00:23 The new Lassila & Tikanoja

00:47 Circular economy operations divided into three service areas

03:23 Market growth

05:19 Growth-hungry targets

08:52 Valuation

11:17 What if the growth targets are not met?

8 Likes

Having some insight into the company, I can agree with the view that increasing profitable growth may be challenging.

I don’t know if growth at any cost is now being prioritized in the company’s strategy. Several local contracts have been won recently, and at the unit level, these are not exactly small. The new projects that have already started are apparently running at a loss, and based on inquiries, a larger upcoming project will likely follow the same line. These are not 100% facts, though.

I don’t know if this is a case of an individual failed local bid calculation or a general policy (hope not!).

This kind of activity does not increase my confidence as an investor. I am, however, under the belief that the company’s operations should be profitable. But as I stated, the perspective is only local, and in light of these actions, the big picture remains a bit of a question mark, at least for me.

11 Likes

I checked that Sampo value on Vero.fi, and it wasn’t stated very clearly ![]()

Based on the aforementioned grounds, the acquisition cost of a Sampo plc share is 91.66 percent of Sampo plc’s original acquisition cost before the partial demerger.

Based on the aforementioned grounds, the acquisition cost of a Mandatum plc share is 8.34 percent of Sampo plc’s original acquisition cost before the partial demerger.

Isn’t that quite clear? It gives you your own acquisition prices based on those.

5 Likes