Osaako joku auttaa… Torm yrityksen osakkeilla käydään kauppaa tanskan kruunuilla, mutta pääkonttori näyttää olevan Englannissa (vai onko)? Meneekö osinkojen verotus Tanskan vai Englannin lainsäädännön mukaan?

Prospectuksen täydennys toteaa seuraavaa:

https://www.sec.gov/Archives/edgar/data/1655891/000119312524150627/d842343d424b7.htm

Vuoden 2016 Exchange offer document myös viittaisi osinkojen verotuksen menevän Ison-Britannian mukaan.

https://www.sec.gov/Archives/edgar/data/1168351/000091957416012066/d7084350_ex1-2.htm

En tunne yhtiötä ja asiakirjojen nopealla selauksella jotain saattoi jäädä huomaamatta. Lopullisen tulkinnan joudut tekemään itse, mutta minusta yhtiö vaikuttaa englantilaiselta.

EDGAR-tietokanta on hyvä paikka etsiä tietoa Yhdysvalloissa listatuista yrityksistä.

Kiitos linkistä. Onpa tämä hankala… Alemmassa kuvassa aika selvästi sanotaan osinkojen menevät Ison-Britannian verotuksen mukaan, mutta alempana dokumentissa sanotaan “TORM A/S is headquartered in Copenhagen”. Eikö osinko veroteta sen maan verotuksen mukaan missä pääkonttori sijaitsee?

Pieni muistutus osakesäästötilin verotuksesta ja rahojen nostosta sieltä. Itselläni on kaksi arvo-osuustiliä ja osakesäästötili (OST) Nordnetissä. Olen kevään markkinaturbulenssissa myynyt osan osakeomistuksista ja käteistä oli siten kertyneenä odottamaan tulevia sijoituksia niin arvo-osuustileillä kuin OST-tilillä. Tänään tein päätöksen nostaa osan ”odottavia rahoja” pois Nordnetistä pankkitililleni ja sieltä ohjasin ne heti Svealle kasvamaan edes hieman korkoa. Huomasin vasta äsken tehneeni noston vahingossa käteisvaroistani OST-tililtäni (!). Kännykällä toimeksiantoa tehnessäni olin siis epähuomiossani valinnut noston tehtäväksi OST-tililtäni enkä arvo-osuustileiltäni. Ja tämän seurauksena joudun maksamaan OST-tililtäni tehdystä nostosta huomattavan euromäärän veroja (koska siellä oli n. 30% arvonnousu). Täysin turhaa, koska vastaava summa lojui arvo-osuustililläni nostettavaksi….Eipä tätä virhettä taida mitenkään oikaistuksikaan enää saada, mutta olkaahan muut tarkkana….

2 tykkäystä

Tuo Kööpenhaminan pääkonttoriviittaus on asiakirjassa, joka on päivätty vuonna 2016 ennen yritysjärjestelyn toteutumista. Keskeistä on, että mainittu yhtiö on Torm A/S eikä Torm plc. Edellisen viestin lainattujen tekstien mukaan listattu emoyhtiö Torm plc (UK), jonka kotipaikka vaikuttaa olevan Lontoo, omistaa kokonaan tytäryhtiö Torm A/S:n (DK), jonka kotipaikka on Hellerup Kööpenhaminan esikaupunkialueella. Torm plc maksaa osingon osakkeenomistajilleen, jotka voivat käydä kauppaa emoyhtiön osakkeella kahdessa pörssissä. Tanskalaisen tytäryhtiön Torm A/S osakkeet eivät ole olleet kaupankäynnin kohteena pörssissä vuoden 2016 yritysjärjestelyn jälkeen. Jos sijoittaja omistaa Isossa-Britanniassa sijaitsevaa yhtiötä, osingot tulevat Isosta-Britanniasta ja niihin sovelletaan Suomen ja Ison-Britannian välistä verosopimusta.

Aivan mahtavaa, iso kiitos tästä tulkinnasta ja salapoliisityöstä !!!

1 tykkäys

Terve. Jos yhtiön osake on listattu Lontoon, Amsterdamin ja New Yorkin pörssissä, onko osinkojen verotuksen suhteen (suomalaiselle AOT:lle) suurta merkitystä mistä osaketta ostaa?

Listauspaikalla ei lähtökohtaisesti pitäisi olla vaikutusta osinkojen verotukseen. Yhtiön kotipaikka ratkaisee verotuksen. Joissain valtioissa saatetaan pidättää paikallisia veroja myös siellä listatuista ulkomaisista osakkeista saaduista osingoista. Lontoon, Amsterdamin ja New Yorkin pörssit eivät ole tässä asiassa ongelmallisia.

Jos kyseessä on iso englantilainen yhtiö kuten Shell tai Unilever, Lontoosta ostaessa sijoittajalta peritään leimavero (stamp duty), joka on 0,5 prosenttia ostohinnasta. Toisaalta New Yorkin rinnakkaislistattua osaketta ostaessa näiden yhtiöiden jokaisesta osingosta peritään ADR/ADS-maksu.

Käsittääkseni Lontoossa leimaverolta välttyy AIM-listatuissa osakkeissa sekä niissä, joiden kotipaikka on Guernsey, Jersey, Mansaari tai ulkomaat. Näiden seikkojen ohella ainakin osakkeen likviditeetti eri pörsseissä on syytä ottaa huomioon ostopaikkaa valittaessa.

2 tykkäystä

Jos veronkiertäjät saadaan kiinni ja maksamaan omat veronsa, niin muiden ei tarvitse maksaa heidänkin osuuttaan.

Jos jutun kymmenet miljoonat olisi vuodessa edes 28,5 M€, tarkoittaisi se 5 €/suomalainen eli noin 10 €/veronmaksaja vähemmän verotustarvetta.

Kun tätä kryptovoittojen veronpimitystä on jatkunut vuosikausia, kertyy ihan kiva potti. Valitettavasti verottaja tutkii vain viisi vuotta taaksepäin, mutta korkoa verorikolliset saavat maksaa vajaat 10 % per vuosi eli vimpan päälle. Sakot ja vankeudet sitten erikseen.

Siis kukin suomalainen veronmaksaja maksaa yhden vuoden aikana laskennollisesti noin 150 € vähemmän veroja, jos ja kun kryptoverorötöstelijät pannaan kuriin. (Karkea suuntaa antava laskelma)

Pitäisikö mielestäsi painaa kaikki kryptoihin liittyvät vanhat veropetokset villaisella? Haluaisitko maksaa verot heidän puolestaan myös jatkossa?

2 tykkäystä

Aika lillukan varsia vielä varsinaisessa veronkierrossa/verosuunnittelussa, mutta hyvä jos kaikki verot saadaan suomeen. N 5% BKT:sta arvioidaan kierrettävän veroja. On pimeää työtä, kuittikauppaa, ALV-petoksia, käteispalkat ilman laskutusta, kirjanpitorikokset, pimeää yrittämistä, pääomien piilottamista, lähdeverojen kiertämistä yms..

Holdingyhtiöt ja kaikenlainen verojenvälttely ei ole liian monimutkaista kun rahaa löytyy reilusti. Ei tarvitse veroja maksella.. Tämä siihen päälle.

Vanha snippi mutta antaa jotain kuvaa minkäluokan ongelmasta puhutaan.. kaikenmaailman puliveivareiden takia tääkin maa velkaantuu..

Mutta eipä noita porsaanreikiä tulla koskaan tukkimaan riittävästi sillä silloinhan rikkaatkin joutuisivat kaikki ottamaan osaa talkoisiin..

1 tykkäys

Miten bonusosakkeiden verotus menee? Jos oletetaan, että mulla on vaikka postin bonus-osakkeita 100kpl ja pidän niitä vuoden. Jolloin saan 10 osaketta lisää. Koko potti on silloin 110kpl. Ja ne konvertoituvat tavallisiksi postin osakkeiksi. Onko näiden 10 osakkeen hankintahinta 0e ja muiden osakkeiden 7,5e vai jokaisen osakkeen hankintahinta 6,82e?

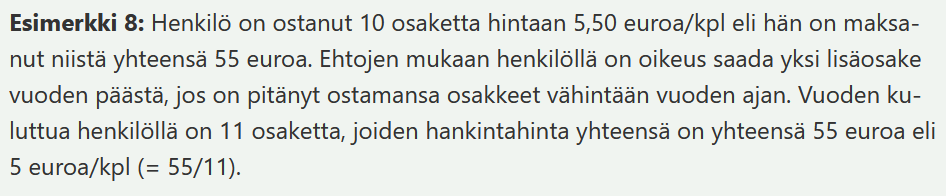

Jos ylimääräisten osakkeiden hankintahinnaksi tulee 0e, niin onko ne fivo-periaatteella ensimmäisenä vai viimeisenä jonossa?

Nähdäkseni jokaisen hankintahinta on noin 6,82 euroa.

”Bonusosakkeen hankinta-aika lasketaan alkuperäisten osakkeiden hankintahetkestä. Bonusosakkeen hankintameno määräytyy sen hinnan perusteella, joka bonusosakkeeseen oikeuttavista osakkeista niitä hankittaessa on maksettu. Yhden osakkeen hankintameno lasketaan esimerkiksi yllä mainitussa tapauksessa jakamalla kymmenestä osakkeesta maksettu hinta yhdellätoista. Näin laskettua hankintamenoa käytetään laskettaessa sekä alun perin hankittujen osakkeiden, että niiden nojalla saadun bonusosakkeen luovutuksesta syntyvää luovutusvoittoa tai -tappiota. Hankintameno-olettamaa käytetään, jos se on osakkeen todellista hankintamenoa suurempi.”

3 tykkäystä

Mitä mahdollisuuksia on saada selville, onko kuolinpesän osakas saanut ennakkoperintöä ja minkä verran? Samoin, onko viimeisen 3 vuoden aikana saanut lahjana rahaa?

Teoriassahan pitäisi tehdä ilmoitukset verottajalle, mutta mikäli ei ole tehty, voiko nämä saada selville muut osakkaat, verottaja, pesänselvittäjä?

Ei suora vastaus kysymykseen, mutta kysymys tuntuu sivuavan aihetta hallituksen uudesta esityksestä, jossa verottajalla olisi pääsy kaikkien kansalaisten tileille ilman kummempia perusteita.

Varmaan “ajatuksena” on ollut juurikin päästä karhuamaan lahja-/perintöveroja, kryptovoittoja, harmaata taloutta yms., mutta itse kyllä koen tuon mahdollisen uudistuksen olevan suoraan askel kohti syvempää isoveli valvoo-järjestelmää. (Siirtäkää parempaan keskusteluun jos sellainen löytyy)

Ja sitten se oma näkemys kysymykseen: jos kyseesen tulisi mahdollisesti verottajan kannaltakin kiinnostava summa, voisi verottaja ottaa asia selvityksee , jolloin ehkä kuolinpesäkin sais asiasta selkoa?

4 tykkäystä

En tiedä kuuluuko varsinaisesti tänne mutta laitan kuitenkin.

Eli nyt kun saa vuoden 2025 veroilmoitukseen laittaa vähennykset niin missä kohtaa tulee pääomatuloista tehtävät tulonhankkimismenot?

Ainoa kohta joka sieltä tulee niin kuitenkin lukee:

Älä ilmoita apurahoihin kohdistuvia kustannuksia, työasuntovähennystä tai pääomatuloihin kohdistuvia tulonhankkimismenoja. Ilmoita nämä vähennykset erikseen niille varatuissa kohdissa.

Ja tämän jälkeen ei tule erikseen mitään kohtaa johon nuo ilmoittaisi.

2 tykkäystä

Verottajalta löytyy ohjeet kuinka esitäytettyyn veroilmoitukseen mitkäkin asiat ilmoitetaan: Esitäytetty veroilmoitus - näin ilmoitat OmaVerossa tai paperilla - vero.fi

1 tykkäys

Esitäytetyssä veroilmoituksessa on laajemma tiedot kuin omaverossa nyt löytyvissä. Sinne esitäytettyyn tulee mm. pörssissä tai rahastoissa käydyt kaupat siten kun välittäjä(t) ne imoittaa, pankkien ilmoittamat korkotiedot jne… Sinne lienee tullee lisäkohta johon ne muut kulut saa lisättyä.

Niin ongelmahan oli että kyseistä kohtaa mihin vähennykset ilmoitetaan ei ole.

1 tykkäys

@Voihan Siellä on yhdessä kohdassa vapaatekstikenttä mihin nuo täytetään, mutta sekin on aluksi piilossa, eli pitää klikata kohta auki.

edit: se vapaatekstikenttä onkin siellä esitäytetyssä veroilmoituksessa, tuossa ennakkoilmoituksessa ei sitä kyllä löytynyt ![]()

1 tykkäys

Eli jos vielä selventää koittaa, Omaverosta ei Vielä löydy ko. kohtaa, tulee sitten näkyviin aikanaan kuukauden, parin sisään, kun esitäytetty veroilmoituskin saapuu. Samaa joku vuosi sitten pyörittelin ja kirosin. Juuri tällaisia ‘itsestäänselvyyksiä’ ei (missään) mainita..