Today, Kesla published a positive profit warning and simultaneously released its business review.

https://www.inderes.fi/fi/tiedotteet/positiivinen-tulosvaroitus-kesla-oyjn-tilikauden-2023-liiketulos-kasvaa-selvasti-vuodesta

https://www.inderes.fi/fi/tiedotteet/kesla-oyjn-liiketoimintakatsaus-11-3132023

- Revenue grew by 72.5% and was EUR 16.4 million (9.5).

- Operating profit increased by EUR 1.2 million and was EUR 602 thousand (-596). The operating profit for the comparison period was burdened by a EUR 280 thousand impairment provision related to Russian operations.

- Cash flow from operating activities turned positive and was EUR 1,722 thousand (-3,398).

- Earnings per share increased and were EUR 0.13 (-0.16) for both A and B shares.

- Orders received remained at the comparison period’s level and were EUR 14.5 million (14.9).

- The order book remained at the comparison period’s level and was EUR 33.8 million (33.9).

- During the first quarter, Kesla concluded change negotiations regarding the Ilomantsi facility. The company also renegotiated a EUR 2 million maturing bullet loan and a EUR 3.0 million group account limit.

Key Figures

| EUR thousand, unless otherwise stated |

1−3/2023 |

1−3/2022 |

Change, % |

1−12/2022 |

|

|

|

|

|

| Orders received |

14,562 |

14,854 |

-2.0 % |

55,270 |

| Order book |

33,822 |

33,943 |

-0.4 % |

37,038 |

| Revenue |

16,365 |

*9,486 |

72.5 % |

45,863 |

| Operating profit |

602 |

-596 |

n/a |

-1,319 |

| Operating profit, % |

3.7 % |

-6.3 % |

n/a |

-2.9 % |

| Total comprehensive income for the period |

430 |

-535 |

n/a |

-1,181 |

| Earnings per share, EUR ** |

0.13 |

-0.16 |

179.4 % |

-0.35 |

| Return on investment (ROI), % |

8.4 % |

-9.3 % |

n/a |

-4.9 % |

| Return on equity (ROE), % |

13.8 % |

-15.8 % |

n/a |

-8.9 % |

| Cash flow from operating activities |

1,722 |

-3,398 |

n/a |

-5,377 |

| Gross investments |

65 |

193 |

-66.3 % |

3,811 |

| Net interest-bearing debt |

14,823 |

13,500 |

9.8 % |

16,478 |

| Net gearing ratio, % |

116.5 % |

104.4 % |

n/a |

134.0 % |

| Equity ratio, % |

34.6 % |

35.1 % |

n/a |

32.0 % |

| Average number of personnel |

253 |

249 |

1.6 % |

246 |

(*) Includes EUR 1.0 million in Russian trade.

(**) Both basic and diluted earnings per share for both A and B shares.

Revised guidance for 2023

Kesla estimates that its 2023 revenue will grow and its operating result will grow clearly from the previous year.

Previous guidance: Kesla estimates that its 2023 revenue and operating profit will grow from the previous year.

(*) In its guidance, the company has transitioned to using the term ‘operating result’ (liiketulos) instead of ‘operating profit’ (liikevoitto).

CEO Marko Pekkola:

"After a challenging financial year 2022, we succeeded in the first quarter in growing revenue to EUR 16.4 million, which is 74.25% more than in the comparison period (9.5). The growth in revenue was driven by the clearing of delivery backlogs, which was achieved through the development of production processes and improved component availability.

The key to Kesla’s financial development in 2023 continues to be the removal of bottlenecks in production chains and restoring the production rhythm to a normal level. Improved delivery capacity combined with intensified management of fixed costs and working capital improved business profitability and cash flow. The operating result improved clearly from the comparison period, being EUR 602 thousand (-596), and correspondingly, the cash flow was EUR 1,722 thousand (-3,398).

Our focus areas in 2023 are particularly the improvement of profitability and bringing net gearing to the target level, towards which we have already done good work in the first quarter. We have succeeded in turning the result positive, and net gearing has decreased during the first quarter from 134.0% to 116.5% (104.4). The amount of net debt decreased by EUR 1.7 million in the first quarter.

Order flow has remained strong throughout the first quarter. The value of orders received remained nearly at the level of the comparison period, being EUR 14.6 million (14.9). The share of exports grew and was 62.4% (60.9%). Demand was particularly strong for truck and industrial cranes. At the end of the quarter, the order book was at the comparison period’s level at EUR 33.8 million (33.9).

During the first quarter, together with our personnel and stakeholders, we have managed to correct the direction of the business and we continue that work to meet our customers’ expectations.

We have begun a strategy update. We will publish the targets in accordance with the new strategy during the third quarter."

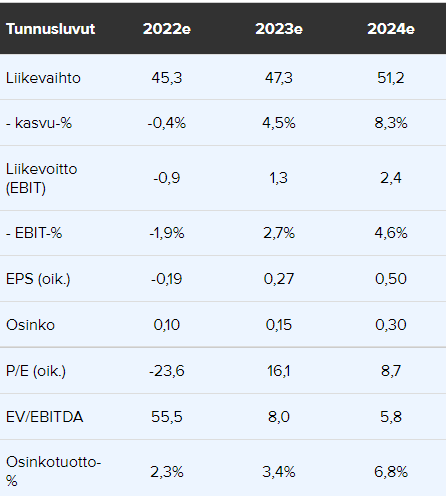

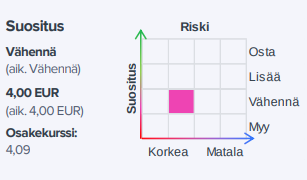

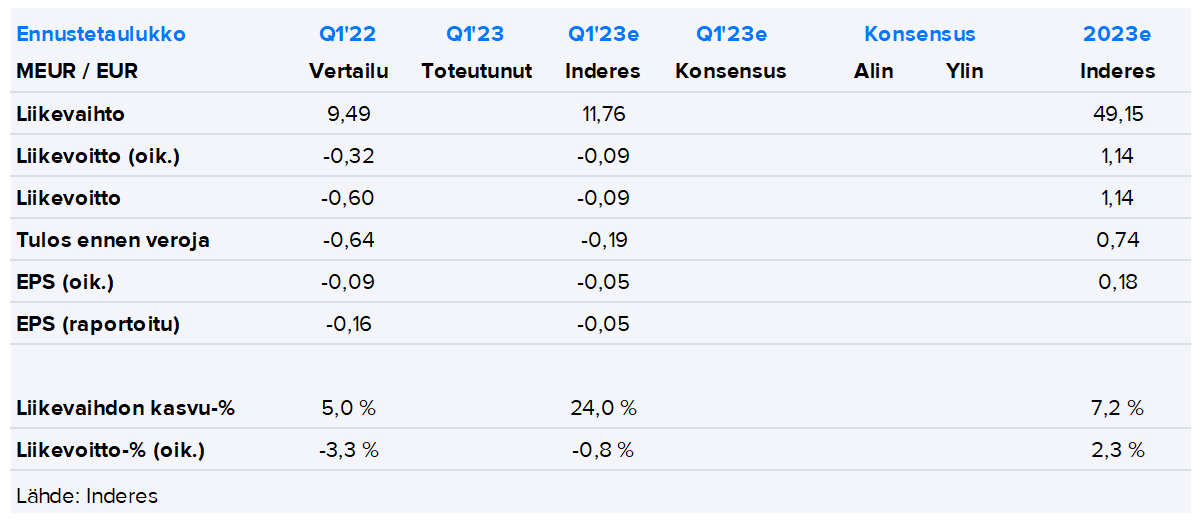

Inderes’ advance expectations: