This time I wrote about Kesla. This will not be an analytical text, and this industry (too) is difficult for me, so there will be no amazing independent conclusions. I googled for information about the company, read this thread, and naturally, I have extensively reviewed Inderes’ materials for this company, read other websites, and, of course, the company’s own homepage.

Kesla is a machinery engineering group over sixty years old that develops, manufactures, and markets forest technology. The company’s products include truck and industrial cranes, timber harvesting equipment, and tractor attachments.

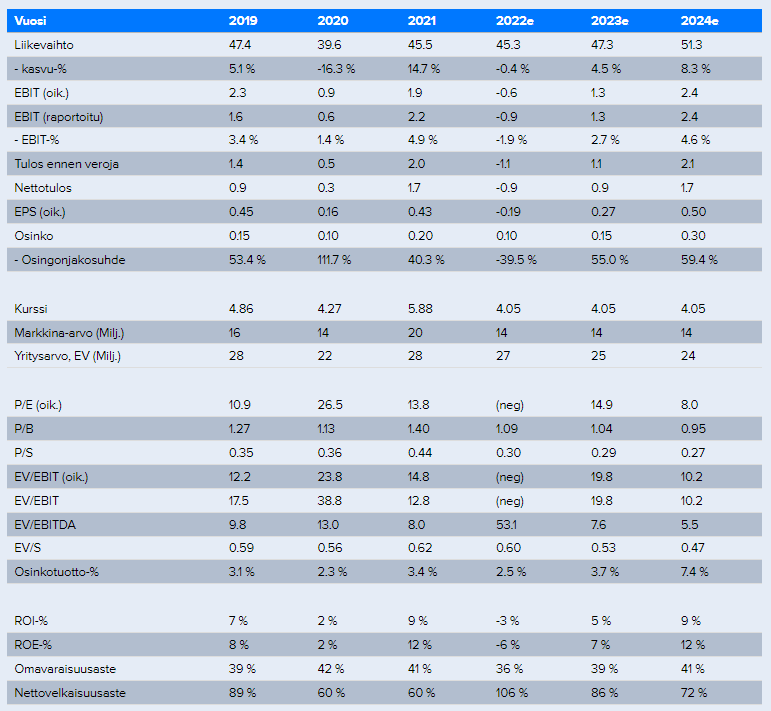

- Kesla’s turnover in 2021 was 45.5 million euros.

- Kesla employs 250 people.

- Its main office is in Joensuu, and other offices are located in Kesälahti, Ilomantsi, and Appenweier.

Kesla is a modern forest technology and material handling operator that produces contemporary and sustainable products, aiming for long-term customer relationships. Products are often made to fit the specific needs of each customer; Kesla may not compete on price, but it certainly does on quality and usability.

Russia’s and Belarus’s share of the company’s turnover was about 17 percent before the war, so this is Kesla’s biggest concern. The events in Russia ultimately came as a surprise, so Kesla didn’t really have time to prepare for them, which has been very strongly reflected in the figures and other performance. The company canceled orders worth 22 million euros concerning Russia, and the war also brought inflation and challenges in component availability.

Speaking of problems, cyclicity is a challenge, but it’s part of the business. The long-term outlook for the industry is hazy, but on the other hand, over the years, Kesla has performed reasonably well, even considering the cycles. However, the cycles of the company’s different sectors may run at slightly different paces, which somewhat balances the situation.

The third major challenge is margin issues and cost structure. The cost structure is rather rigid, and as far as I understand, there isn’t much flexibility, which combined with delightful inflation, is not an ideal situation. However, Kesla has the NOSTE automation project, which aims to make investments and developments that would improve the utilization of automation and digitalization in various areas, such as business processes, alleviate capacity and productivity bottlenecks, etc.

What fascinates me about Kesla is its innovativeness, high-quality products, and customer-friendliness. Also, long customer relationships, a strong market position, widely diversified customer base, and opportunities for acquisitions make me somewhat interested in this company that just issued a negative profit warning. The company is also working to address problems, for example, through the NOSTE project.

Russia became a big minus for the company, but on the other hand, there is potential to expand more strongly in Latin America and Southeast Asia, where the importance of these regions is growing in this industry. Through partners and various distributors, Kesla can gain new opportunities, and Kesla’s development-oriented approach may bring it additional revenue streams, for example, through lifecycle services. Could this become a very significant area for Kesla over the years?

Kesla faces really big challenges and various issues over which it ultimately has quite limited control. I don’t know if I can say this, but I will anyway; Kesla seems like a good company in itself, despite current challenges and a recent negative profit warning. With the help of partners and acquisitions, it has opportunities to grow; the company takes a long-term view and is development-oriented, the NOSTE project should increase profitability, and if we forget about Russia, there are long-term growth drivers in the market.

I omitted writing about things I didn’t fully grasp, so my writing is quite incomplete in many respects. I may also have misunderstood texts from Kesla, Inderes, or others, and I have drawn independent conclusions, which I would view with great reservation.

The Kesla thread has been very quiet, and the industry or the company is not very appealing to the masses, which is why I wanted to research this company, hoping that at some point I might find a good buying opportunity before others, if/when the company establishes a good and long upward trend.