Staring in the rearview mirror doesn’t suit investing very well. Soon even Inderes will have to raise its forecast again. A €50 / share target price would have been a fairer forecast from you. So that you don’t have to constantly be lagging behind. You guys tend to have the handbrake stuck on ![]()

3 Likes

I browsed through the thread again, and maybe about 80% of the discussion is negativity regarding risks, the stock being expensive, and losing the technical lead to competitors.

I recommend everyone watch the company’s CMD if you haven’t seen it yet. It answers many questions that have been raised here before. CMD

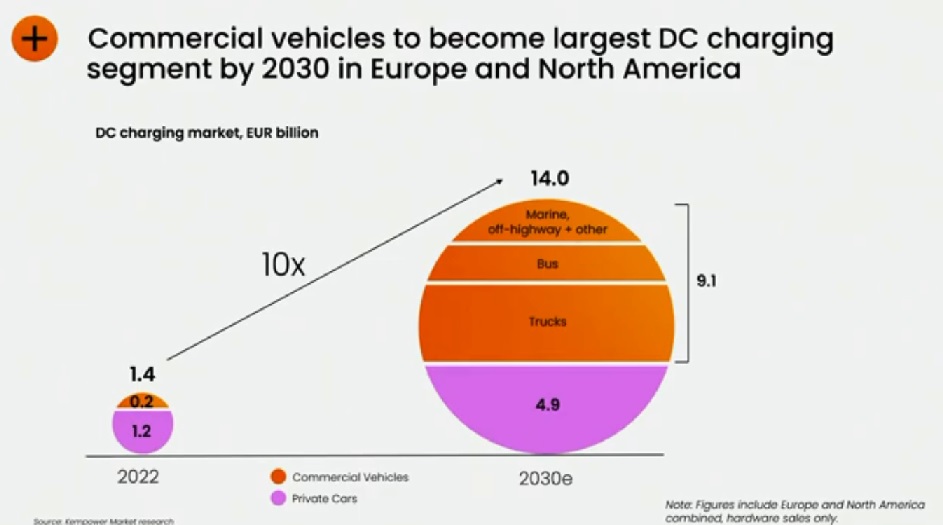

There has been very little discussion here about the company’s opportunities, and in my opinion, they are absolutely massive if they succeed in their goal of being a top 5 player by 2030 in the European and North American markets.

In that market, the TAM has risen from 4 billion to 14 billion in two years according to the company, and this includes hardware sales only.

Software and services are on top of this, which according to them will be a significant part of revenue by then.

Additionally, the company already has sales elsewhere in the world, e.g., Australia, which are not included in that market calculation.

The company now has a factory in Lahti, which will generate ~300M€ in revenue this year, and a similar-sized factory is coming to North America by the end of this year. With these two units, one could expect to reach 600M€ in revenue.

A month ago, the company announced it would double its facilities in Lahti in stages during next year, which should consequently double the capacity in Europe as well. The new production space also included an option to expand the facilities later.

By the end of 2024, capacity could therefore be around 900M€, if all three production facilities can reach current levels of efficiency.

I personally believe that the company will achieve its financial targets as early as the end of 2026 (750M€ revenue + EBIT 10-15%).

They are already a major player in Europe and, in my opinion, they have very good products that competitors have not yet been able to match.

They have grown significantly faster than the market and have done so profitably.

It’s true that, for example, ABB’s and Volkswagen’s muscles for R&D are huge, but still, ABB hasn’t managed to create a similar dynamic power sharing.

Also, Volkswagen hasn’t managed to bring battery pre-heating to its MEB-platform cars in two years, even though smaller competitors were able to do it in a few months.

If they haven’t managed to do it in this time, why would they succeed later?

This is a good example: when products are designed the wrong way for the market in question, it can be impossible to change them later to meet market requirements.

If Kempower can continue to be the best choice for its customers in that market, then taking 8-15% of that previously mentioned 14 billion market by 2030 illustrates the opportunities they have in the future.

It should be remembered that the global charging market is still at its very beginning and is predicted to grow at ~30% CAGR until 2030.

29 Likes

Affärsvärlden has published an analysis of Kempower, resulting in a neutral recommendation. The company’s strong growth figures and targets are noted, as well as its somewhat demanding valuation.

It states that the company may suit a growth investor’s portfolio and anticipates that market competition will intensify before long.

It doesn’t go very deep; the article is mainly an introduction for Swedish investors.

Interestingly, according to the Swedish broker Avanza, over 1,300 of their clients own Kempower. For comparison, just over 600 Avanza clients own QT.

https://www.affarsvarlden.se/analys/kempower-finsk-tillvaxtmaskin

6 Likes

Nissan will also gain access to the Supercharger network.

Same thoughts. I actually made a meme for the meme thread the other day. Lots of fear-mongering and doom-and-gloom scenarios. One crack and pretty much everything collapses. That crack hasn’t shown up yet. Of course, the threats must be taken seriously, but you shouldn’t let them prevent a buying decision. But yeah, time will tell. Let’s hope for the best.

This is the main reason why I got involved. Not the only one, of course, but the most significant. Passenger car traffic is electrifying at a fast pace, but we are only at the first kilometer of the marathon. If Kempower gets even a moderate slice of this, things will turn out well.

Additionally, it’s worth noting Kempower’s focus on the heavy-duty side. There is a picture I posted earlier in this thread that explains the matter. It has been estimated that the construction of charging units for heavy vehicles will even surpass the construction of passenger car charging units.

Edit: image added

5 Likes

Exactly, the European Automobile Manufacturers’ Association (ACEA) yesterday released data on new car registrations in June:

-

June was historic, as for the first time ever, the share of battery electric cars in European Union new registrations was higher than the share of diesel cars…

-

The combined share of battery electric vehicles (BEVs) or plug-in hybrids (PHEVs) in new registrations was 23 percent in June, while the corresponding share in June 2022 was 19 percent.

(=In total, approximately 1.045 million new passenger cars were registered in the European Union area in June, which is about 18 percent more compared to June 2022.)

7 Likes

That is a good chart showing how the commercial vehicle segment is expected to grow over 40x by 2030.

Over 25% of Kempower’s revenue comes from the commercial vehicle segment (CMD slide), so they are already very well positioned in that market.

5 Likes

The topic of @Omavaraisuushaaste’s latest blog post is Kempower (and Spinnova too). In my opinion, the text remains quite superficially critical regarding Spinnova; its momentum/activity is gradually picking up.

12 Likes

Thanks for sharing @Koala! The Spinnova comment wasn’t meant to diss the company itself or serve as a business analysis of it, but rather to highlight the main point of the whole post about how difficult it was to analyze both at the start of the journey—and honestly, still is. And how, at least for now, the journeys have been very different, with Kempower going from one positive surprise to another, while the other journey has involved very clear challenges.

Stocks like Kempower often cause unnecessary FOMO and self-flagellation among investors for not realizing it was a clear winner—even though that is pure hindsight. Kempower is truly a once-in-a-decade stock, given how smooth its journey has been.

Regarding Kempower, it should indeed be added that the company is, as discussed in this thread, only at the very beginning of its journey. A frequently repeated, but according to statistics, often forgotten piece of wisdom is that it pays to hang onto winners for much longer than feels comfortable, as can be seen from the scenarios in the text. In a couple of years, the multiples could be completely melted away if the train stays on the tracks.

This is why I wanted to bring up that (overly) optimistic scenario in the text, as even Inderes’ estimates are conservative if interest rates were to fall or if Kempower were to receive even more macroeconomic or regulatory tailwinds for its business.

28 Likes

I skimmed through that comprehensive article from the Omavaraisuushaaste (Self-Sufficiency Challenge). I’ll have to read it again more carefully when I have the time; it was such interesting stuff.

This caught my eye, as a Kemppi fanatic:

What can you pay for a company that grows year after year at a pace never seen before in the history of the Helsinki Stock Exchange?

Is this true? Is it really like that? Not even Nokia during its crazy years, Revenio, or someone? Whatever the case, the momentum is incredible. The Helsinki Stock Exchange is just lagging and flatlining, but this one hero just keeps pushing against the headwind.

9 Likes

I’m feeling a bit of FOMO about this. So far, I’ve been watching from the sidelines, occasionally kicking the tires and reminding myself that what goes up must come down. The P/E ratio is a staggering 521, in the same league as Nvidia galloping on AI hype, which signals FOMO and significant overvaluation considering short-term earnings potential. But you do wonder: could this really have the potential to be the “next Nokia”? The markets are obviously massive, but does Kemppi have a real competitive advantage compared to its rivals?

8 Likes

The system’s total efficiency advantage etc. is about 30% better than competitors, which is decisive. User convenience is also the best possible. Tesla’s chargers push power at the same speed to every car at a charging hub, but Kempower distributes power intelligently, giving the most to the one with the emptiest battery. It also slows down the charging slightly once 80% is reached. Just 7 min and you can go 150 km! For many competitors, expanding a charging hub will be expensive. I added more today; in my opinion, it’ll be €60 by Christmas or even by the time of the Q3 release..

8 Likes

The total power of the charging hub determines how much power can be delivered per car. Kempower can, for example, provide 150 kW continuously throughout a 0–100% state of charge. The car determines how much it can receive at any given percentage. If a car can only receive, for instance, 30 kW, the remaining power of the charging hub is distributed among the others currently charging.

1 Like

What do you mean, the best possible? For the consumer, Tesla is specifically better. Power is always available. At a Kempower station, you can’t be sure, but that’s not Kempower’s fault.

In a sense, it’s pretty much all the same to Kempower what Tesla does. Tesla doesn’t sell chargers to others. Tesla is both a hardware manufacturer and a charging operator, so Tesla decides what kind of user experience it wants. Which means fast charging for everyone in all situations. Kempower’s hardware is also capable of that, but the operator can then ruin the user experience with their own specifications. For example, a station with a maximum power of 150 kW and five chargers. In that case, with a full station, it might happen that everyone is just trickling in electricity at 30 kW.

But. Rarely, if ever, are we in a situation where a bunch of cars arrive at the charging station at the same time with completely empty batteries. People arrive and leave at different times. Towards the end of the charging cycle, the power demand is lower, leaving capacity for those who arrived later. This is precisely where Kempower’s advantage lies over other hardware manufacturers who sell hardware to operators. Dynamic power distribution. You don’t need to install an absurdly large grid connection at the charging station, as the full capacity is actually almost never needed. It reduces costs.

And there are certainly locations where you can’t get a grid connection that meets Tesla’s requirements. Tesla won’t go there. An operator using Kempower can.

8 Likes

If such requirements exist, then at least the Akaa Supercharger hardly meets them. I was late for a meeting last autumn when the car only got 40 kW instead of 100+ kW, even though pre-heating was done. And it wasn’t the only poor experience at that site.

Last year, Inderes wrote in a comprehensive report that:

However, we estimate that the competitive moats created through patenting are of minor significance in the overall picture, as somewhat similar functionalities can be developed using several different technical solutions. We do, however, estimate that Kempower has a technological lead over most competitors, for example, in the field of power management. Developing similar features could take competitors several years, especially for those players who have not invested with comparable intensity in R&D and their own power management technology.

So, when determining the company’s value, I think this is a fairly central question: how long can this lead last? When will a product with relatively similar features and pricing be released by competitor X?

1 Like

It’s quite rare to find charging sites (with more than two chargers) where the maximum site power is only up to 150 kW. Many cars can draw that much power on their own.

Tesla’s older second-generation chargers share power with the adjacent car, so they don’t have smart power distribution yet; instead, those wanting faster charging have had to pull up to a charger with a different number. That is, 1A and 1B share power between them, as do 2A and 2B, etc. The newer V3 chargers can deliver up to 250 kW, but this requires a significant total capacity to ensure everyone can charge at full power. I don’t know if Tesla uses any kind of load balancing in its latest chargers, but Kempower is certainly top-tier.

By digging around online, I found from the “Tesla grapevine” that the latest Tesla V3 Superchargers have a total capacity of either 400 kW or 1200 kW, so not all cars will get that 250 kW if there are other chargers in use at the site.

The next question then is whether Tesla can distribute power as intelligently as Kempower. My understanding is that the answer is “not for the time being, at least.”

3 Likes

Yeah, I forgot about those few V2 Supers still in Finland, of which Akaa is one. If I recall correctly, there are six of these older V2 Supercharger sites in Finland. For a long time now, only V3s have been installed. This year alone, at least six V3 sites have been added, and old ones have been expanded. In V2, the maximum charging power for a single car is indeed around 150 kW, and additionally, the power is shared between two stalls, as @Bjorninen wrote. There’s been some ongoing issue with Akaa for a long time. Perhaps the grid connection is limited for some reason. Hopefully, all these V2s will eventually be upgraded to V3s.

Yes, but the point was just to show that the charging experience is not in Kempower’s hands alone. And it’s not necessarily relevant to the consumer which technical implementation is used to get their car charged quickly. As long as it happens. These are actually matters between Kempower and the customer. Hopefully, the customer understands what and how it’s worth installing. There’s probably a place for a Kempower salesperson to guide the customer in the right direction, but ultimately, the customer decides what kind of experience they want to offer.

There’s some grumbling online about the fact that at least some locations in the ABC Lataus network have underpowered charging sites. However, the criticism there is specifically directed at S Group, not Kempower.

Tesla reveals very little info about the technical implementation of the Superchargers. But true, at a site with 16 Superchargers, probably not every single car would get 250 kW if everyone started charging at the same time with an empty and warm battery, but there is plenty of capacity. However, this happens with almost 0% probability. My own experience last summer from Sweden: we arrived at a Supercharger and got the last spot. The car did pull 250 kW, but it doesn’t charge at that power for long. The charging power of those who arrived before us had already dropped according to the charging curve, so there was plenty of capacity. And when our charging power dropped after a while, the person who came after us got full power again, and so on.

I don’t know about that, and in my opinion, it doesn’t matter for Kempower. If, say, service station chain X wants to establish its own fast charger network, the option is to get the hardware from, for example, Kempower, Alpitronic, or Siemens. Tesla is not an option. You can put a Tesla charger in the service station yard, but then your own network remains unbuilt.

If you specifically want your own network, Kempower is, in my opinion, the best you can currently get on the market. Let’s make that clear. The intention was by no means to diss Kempower.

14 Likes

It would be very interesting if Kempower eventually ended up on Sandy Munro’s radar. This would increase US consumers’ awareness of the differences between chargers. In fact, I expect Munro to visit the factory in Lahti within a few months. In any case, a visit is very likely to happen shortly after the US factory is completed, if not sooner. This visit will certainly boost US consumers’ awareness of different charger manufacturers. Sandy Munro is known to be far from impressed with Electrify America’s chargers; in fact, he absolutely trashed them in a recent video. I suspect Kempower’s chargers will make the exact opposite impression on Sandy. Can’t wait for that…

10 Likes

Those EA chargers have a bad reputation in the States, apparently due to their reliability. No more solid facts than that.

The Tesla charging experience is quite pleasant for a Tesla driver, as the charger recognizes the car automatically and the car’s charge port door opens from the charger handle, among other small things. It feels like a polished package. Tesla definitely brings Apple to mind in many ways.

For instance, on IO-Tech, there are bad experiences even with Kempower (Kemppi) chargers, but in my opinion, this was the fault of ABC, which builds charging hubs that are too small. It’s frustrating to drive to a high-power charger and only get something like 40kW from it.

4 Likes