The charging power you mentioned, “5-90% with an average of 137kW,” is not possible for that car. You might reach that as a peak power when the battery is nearly empty (unlikely), but definitely not as an average power.

4 Likes

That may well be the case, which is why I was surprised by the power output myself, as I thought 100 kW was the maximum. I’ll have to take some photos if I head that way again this summer to get some data saved.

3 Likes

Kempower chargers are available with both 400V and 800V technology (and Kempower identifies which one is in use) and as fast as the investor’s wallet allows. What you get from ABC-lataus tells you nothing about Kempower; the S-Group has only purchased a few power modules for the cabinets. It is not worth going to a charger with a 40% battery state of charge, or at least you won’t get the speeds made possible by the car and charger technology, and it becomes more expensive with per-minute priced chargers (though these are starting to be a disappearing pricing model). If you want fast Kempower charging here, Recharge is the solution. In short, Kempower offers the best usability for users and is a sensible choice for the investor thanks to its satellite solution and load sharing. So, don’t be worried.

12 Likes

I already posted this in the Enersense thread, but I thought it might interest some people here as well.

The Q&A included the following question: How does Enersense Charging’s product range and capability compare to Kempower?

Pauli and Aapeli answered this question together. ![]()

2 Likes

I’ve been following the company from the sidelines for about a year, but without buying. I can’t say much about the business itself, but this might provide some value to you:

I’ve owned Harvia for a longer time, and during the 2021 boom, the market was performing really well y/y. However, weakness started showing in the q/q figures towards the end of the year. In my opinion, the q/q trend wasn’t really reflected in the valuation yet. When the previous year’s peak results were caught up in Q4/2021, the valuation took a massive beating.

So, I suggest monitoring the valuation and growth from a q/q perspective as well, despite all the hype. Back then, the Harvia thread resembled the Kemppi thread—proper bull mania.

19 Likes

Below is the press release on the matter. I wondered for a couple of seconds if this was such a big deal that even Siili’s CEO was involved in the release, but I got the names Tomi Ristimäki (Kempower) and Tomi Pienimäki (Siili) mixed up. ![]()

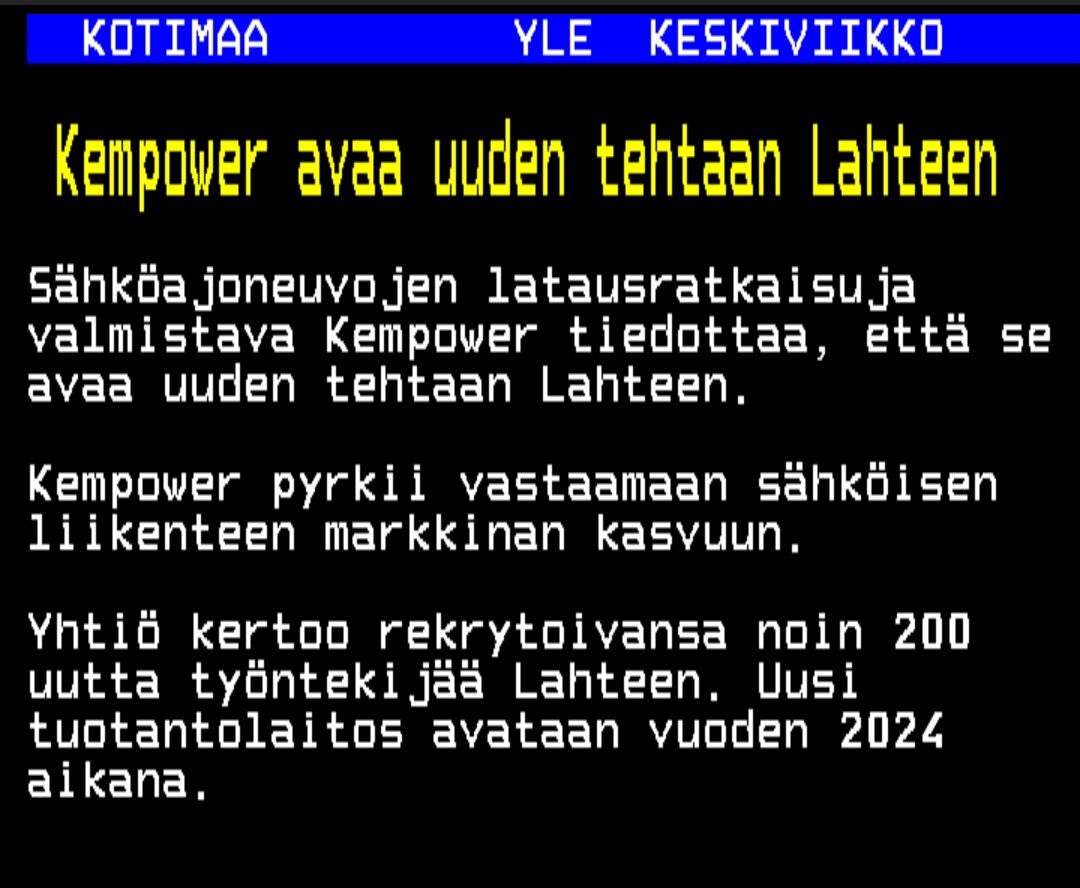

"Kempower, a manufacturer of electric vehicle charging solutions, is expanding its operations and opening a new production facility in Lahti. The company has signed a letter of intent for a lease, comprising a total of approximately 10,000 square meters of new space, along with an option to expand the premises in the future.

- Kempower is opening a new production facility for fast-charging solutions in Lahti to meet the growth of the electric transportation market.

- The new premises have a floor area of 10,000 square meters and are suitable for production, research, and office use.

- Kempower estimates it will recruit approximately 200 new employees in Lahti during 2024–2025.

- The new production facility will be opened gradually during 2024."

17 Likes

OP’s Asta Friman and Henri Parkkinen talked about Neste and Kempower.

OP Analysis has selected five strong long-term stocks that are particularly suitable for a long-term investor’s portfolio. First up are Kempower and Neste, led by senior analyst Henri Parkkinen.

11 Likes

@Pauli_Lohi provided his comments on Kempower’s European growth plans.

Kempower announced it is doubling its production capacity in Europe by opening a new factory in Lahti during 2024. The decision is in line with the company’s financial targets and supports our growth forecasts. We see no need for forecast changes, but we view the progress of the strategy as a confidence-boosting signal. Furthermore, the company stated it is considering additional capacity in Europe during 2024-25, which, if realized, could enable even stronger growth than the financial targets in the medium term.

7 Likes

Here is an article from Salkunrakentaja about Kempower; for those who have read Inderes’ materials more closely, there shouldn’t be much new here, but it’s a fairly good and concise piece. ![]()

“With our new facilities, we are able to meet the growing demand for reliable fast charging solutions. By concentrating product development and research close to production, we can continue to grow cost-effectively and centralize top expertise in electric mobility in Finland,” says Kempower CEO Tomi Ristimäki.

The expansion of Kempower’s facilities in Lahti is part of the company’s growth strategy and its goal to be among the industry’s five largest players in Europe and North America by 2030. By the end of this year, the company will also open a new production facility in Durham, North Carolina.

9 Likes

What is its position in that DC charging market compared to Kempower, since you have clearly researched it?

2 Likes

I haven’t researched it. If anyone knows the company in question better – I’d be happy to receive information. I’m just noting that it’s on a strong rise, and at the same time, I’m wondering how HOT the charging markets as a whole are right now.

Seppo Saario a while ago regarding Kempower:

9 Likes

Wallbox seems to be primarily focused on the AC side with its products. On the DC side, they have the Supernova charger, which is available in 60 and 150 kW power outputs (split between two cars). My guess is that they contain a varying number of 15 or 30 kW power modules. The power modules and charging cables appear to be in the same unit, so I don’t see anything revolutionary here compared to Kempower’s “hype boxes.”

8 Likes

In the future, there must be charging stations for electric passenger cars every 60 kilometers. They must have a power output of at least 400 kilowatts.

For trucks and buses, charging stations must be available every 120 kilometers.

23 Likes

What an amazing company.

58 Likes

I don’t think there’s ever been any reason to assume otherwise ![]()

![]()

It just bugs me that these positive profit warnings always pop up right when I’m considering adding to my position.

3 Likes

- Operational EBIT increased to EUR 13.9 million (EUR 1.8 million), 19.2% of revenue (8.5%)

Unless profitability was somehow exceptionally weak this time last year, my reaction when reading the positive profit warning was:

![]()

![]()

![]()

![]()

Seasonal variation probably has an impact, but the result grew by 100% in a single quarter.

It reminds me a bit of the Kahoot hype days, hopefully the continuation doesn’t repeat the same way as it did there ![]()

By the way, that’s quite a majestic upgrade:

2023 revenue; EUR 280–310 million assuming that exchange rates do not have a significant impact (2022 revenue: EUR 104 million, previously published revenue forecast on 14.4.2023 was EUR 240–270 million)

Even the analyst has to raise their forecasts more significantly, since the previous one was under 270m. This year, growth will almost certainly still be over 200%; the question is, can we still get triple-digit growth % next year, contrary to the analyst’s current forecast?

The classic “I’d be rich by now if I hadn’t sold” ![]() . Well, luckily I kept at least 12 shares for my “forever hold”.

. Well, luckily I kept at least 12 shares for my “forever hold”.

Edit, there was at least some warning in the positive profit warning after all ![]()

Kempower expects significantly higher fixed costs for the second half of 2023.

32 Likes

I think the most crucial factor for Kempower’s future is EU decisions (+subsidies!), which are forcing industry players to invest.

In the future, there must be EV charging stations for passenger cars every 60 kilometers. Their capacity must be at least 400 kilowatts.

For trucks and buses, charging stations must be available every 120 kilometers.

14 Likes

Yes, and most importantly:

-

“We believe that our proven, agile, and scalable production model creates a solid foundation to meet demand in the coming years,” says Kempower’s CEO Tomi Ristimäki.

-

Kempower, which provides a “good charging experience,” is a highly respected charging brand among electric vehicle drivers…

15 Likes