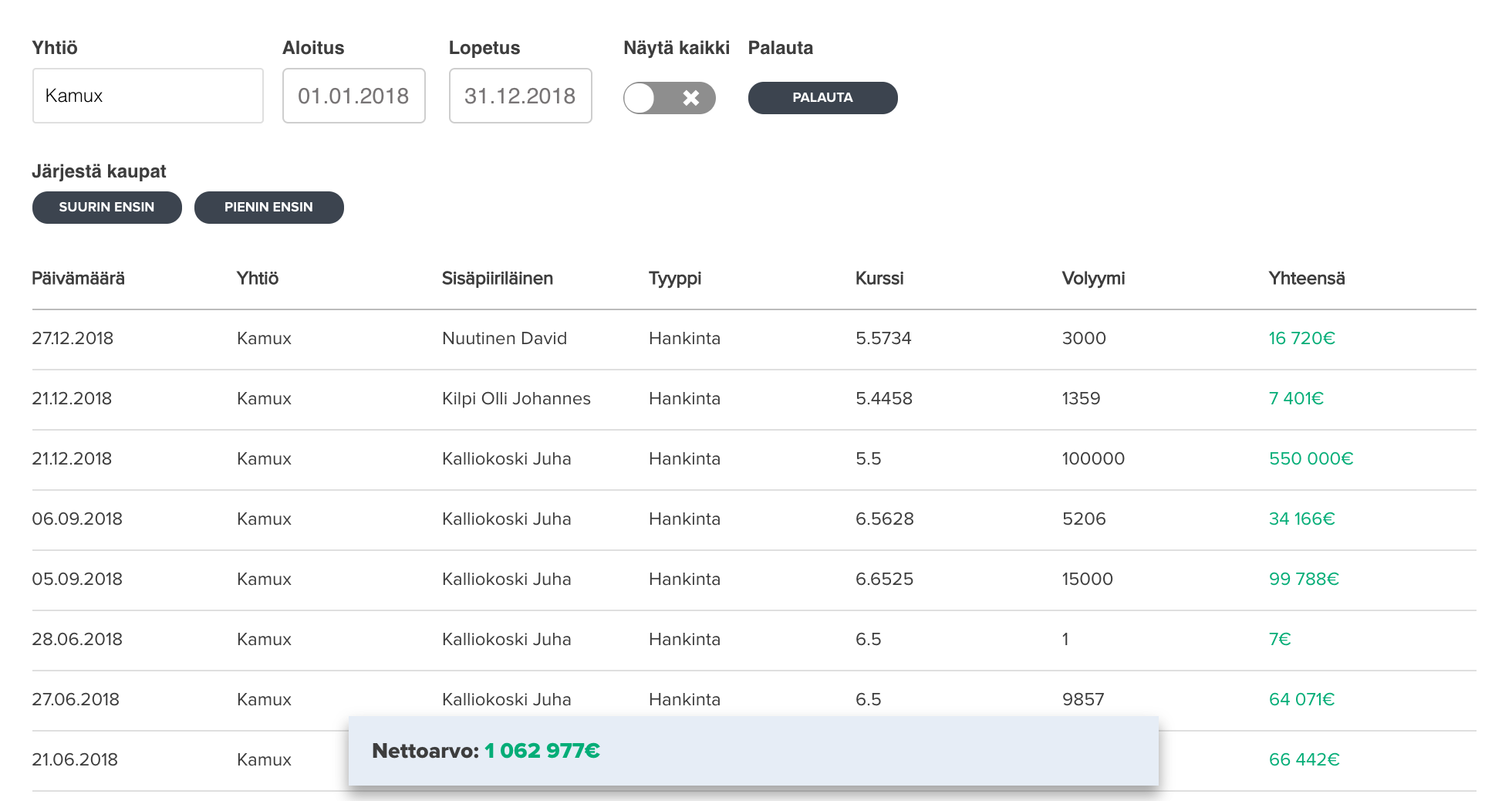

The management sets an example. Kalliokoski bought an additional 550,000 euros worth of shares for his Christmas present.

https://www.inderes.fi/fi/tiedotteet/kamux-oyj-kamux-oyj-johdon-liiketoimet-10

The management sets an example. Kalliokoski bought an additional 550,000 euros worth of shares for his Christmas present.

https://www.inderes.fi/fi/tiedotteet/kamux-oyj-kamux-oyj-johdon-liiketoimet-10

A board member still scraped a slice.

At Kamux, insiders bought over a million shares in 2018 on top of already substantial holdings.

…and additionally, the Trafi register mess at the end of the year

→ Well, that’s an interesting Q4 coming up.

https://twitter.com/kamuxsuomi/status/1087356277670449152

Keeping the workforce happy ![]()

Edit: Apparently, encouraged by the previous one, some employee decided to commit big time to the job ![]()

![]()

Kamux seems to be doing quite well. I bought it for my portfolio at around 6 euros and added a bit more at 5.6-5.7 euros.

From the quarterly report presentation, I got the impression that there had been some difficulties in Sweden, but that a working recipe had been found and Germany had been opened promisingly.

It also seems that stores have been opening at a nice pace and the management has been buying shares. I imagine this will also become a decent dividend payer in my portfolio in a few years. We’ll see if there’s a need to add more. The position has been opened, however.

Kamux’s Updated Financial Targets:

Kamux’s new mid-term annual financial targets are:

* Revenue growth over 10%

* Operating profit margin at least 4%

* Dividend at least 30% of net profit

Kamux’s previous mid-term financial target was to grow revenue to at least EUR 700 million with an operating profit margin of 4-5 percent in 2019 and at least 5 percent operating profit margin in the long term, and to distribute at least 30 percent of net profit as dividends.

Kamux does not publish short-term outlooks.

“The company continues its profitable growth. We are determinedly executing our strategy, and our internationalization is progressing. Our vision is to be Europe’s #1 used car retailer,” says Kamux CEO Juha Kalliokoski.

The market didn’t seem to believe in that EUR 700 million revenue for 2019, so its reduction shouldn’t be a big surprise.

It appears Kamux is lowering its financial targets by reducing its 2019 revenue guidance. The long-term operating profit target was also lowered.

From a valuation perspective, this is a “value warning” ![]()

At least for Kesko, sales of used cars seemed to go well despite Trafi’s confusion at the end of the year:

The year for car sales was successful overall, even though the WLTP emission measurement method caused significant disruptions to car sales across Europe at the end of the year. Porsche’s development was particularly strong, with its first registrations growing by over 60% in Finland. SEAT’s and Volkswagen’s market shares also strengthened. The industry’s operating profit improved, influenced by stable sales development in maintenance, aftermarket, and used cars. During the year, we also launched new mobility services, such as leasing products and car-sharing services, and electric car charging points in connection with K-stores, which enables increasing customer flows across industry boundaries. We expect the market disruption caused by WLTP to normalize by the end of the first quarter of the current year. The car trade strategy is based on comprehensive cooperation with the world’s leading car manufacturer, the Volkswagen Group, in accordance with which the selection will be expanded this year to include the Bentley model range.

Does anyone else think this is currently priced cheaply?

@Verneri_Pulkkinen is Kajaani still shouting at your coffee table “buy, buy Kamux at five and a half now that you can get it…”?

I haven’t bought this one, but the pricing seems very affordable considering the multiples.

I don’t know if you noticed, but I added Kamux to Verkkis’s peer group in the last report. The companies have surprisingly much in common: both have an agile business model that revolves around low prices and efficient inventory turnover, and a significant portion of their earnings comes from financing services.

Haha, you shouldn’t take what’s “shouted” in the office as a permanent indicator. ![]() Yu bought some a while ago, according to the buy/sell thread. I guess the theses haven’t changed.

Yu bought some a while ago, according to the buy/sell thread. I guess the theses haven’t changed.

Kamux is an aggressive market conqueror

The used car market last year was predictably stable.

“In 2018, 630,078 used cars were registered as sold in Finland, of which 571,544 were passenger cars. Growth compared to 2017 was a modest 0.3%.”

https://m.nettiauto.com/artikkeli/vaihtoautokauppa_suomessa_vuonna_2018

I’m just wondering, what’s currently priced into Kamux’s share price? Growth has been pretty decent, but the stock price has fallen.

Q3 video from the fall. Note: after the video was shot, the share price dropped another 10%!

From around 8 minutes 30 seconds, this topic is discussed a bit. In my opinion, Inderes’ view has remained unchanged since this video, and Kamux itself refined its outlook closer to Inderes’ forecast in January.

Based on the video, Kajaani is waiting for the market to wake up to cheap pricing… Also, the stock’s poor liquidity and unsexy/poorly reputed industry cause it to “fly under the radar”?

Perhaps next week I’ll grab another slice, waiting for TP…

I bet there will be an upward correction…

I’m hopeful. Kamux is my most recent significant purchase. I started buying at around 6 euros and continued at 5.7.

By the way, Kamux Q4 press conference tomorrow. This is the last webcast of the earnings season on InderesTV unless there’s another surprise ![]() https://www.inderes.fi/fi/videot/kamux-q42018-tilinpaatostiedote-132019-klo-1100-alkaen

https://www.inderes.fi/fi/videot/kamux-q42018-tilinpaatostiedote-132019-klo-1100-alkaen