Have you compared the adjusted NAV and the share price for the same day?

2 Likes

My habit when a report is released has been to look at the adjusted NAV and compare it to the current share price (at that stage, the IBI Index usually shows the previously reported value). It’s just a rough ballpark estimate. Investor is now at a historical high relative to its net asset value (NAV).

Edit: I’ll add my own questions here, as Jussi_Koskinen’s question reminded me of these.

- Has anyone looked more closely into the IBI Index calculation? From memory, unlisted holdings are included as adjusted estimates based on the latest report. Are there any adjustments made between reports?

- Does anyone use the actual calculated unadjusted NAV? Has anyone tracked it over a longer period? Has anyone found an IBI Index-like analysis for it?

- My own thought is that Investor AB’s adjusted value is the “best estimate at the time.” There is, of course, always the possibility of window dressing or, on the other hand, a misjudgment by the company. Has anyone dug deeper into the adjusted values and done a comparison?

8 Likes

Let’s run a small poll to see what kind of weight people have for Investor (A+B share series combined) in their investment portfolios? In this case, let’s only count listed holdings in the investment portfolio (excluding investment properties, forest land, etc.).

I would be interested in taking a large(r) weight in Investor for my portfolio, as the track record over time is so strong (it has beaten the S&P 500 indices etc.) and I don’t see the same kind of continuity risk here as with, for example, Berkshire Hathaway, where success has been concentrated in Buffett and Munger, who don’t have direct (comparable) successors. At Investor, generation after generation is raised to continue creating shareholder value. Perhaps fresh blood is also well-suited to staying on the pulse of global trends and investment allocation.

But when you think about it, it is quite a concentrated portfolio after all, as indices also tend to be. 20% ABB, 12% Atlas Copco, 8% SAAB, 7% AstraZeneca (=47%).

Currently, I have a 17% weight in Investor (and an additional 5% weight in EQT). If I sell one larger high-risk investment this year, I’ve been considering allocating the proceeds to Investor, which would raise its weight in my portfolio to around 50%. Of course, while writing this message, I realize the absurdity of my reflections, as I currently have 30% of my portfolio tied up in a single lottery ticket, while at the same time, I’m worrying about whether I’d dare move that sum into Investor, which is certainly 100x lower risk ![]()

Here is the poll itself:

- <5%

- 5-15%

- 15-25%

- 25-35%

- 35-50%

- 50%<

0

äänestäjää

13 Likes

Thanks for the thought-provoking post. The content itself is simple and an excellent example of the saying by the other legend mentioned in that message: investing is simple, but hard. In reality, people want returns, and in the end, the style matters very little.

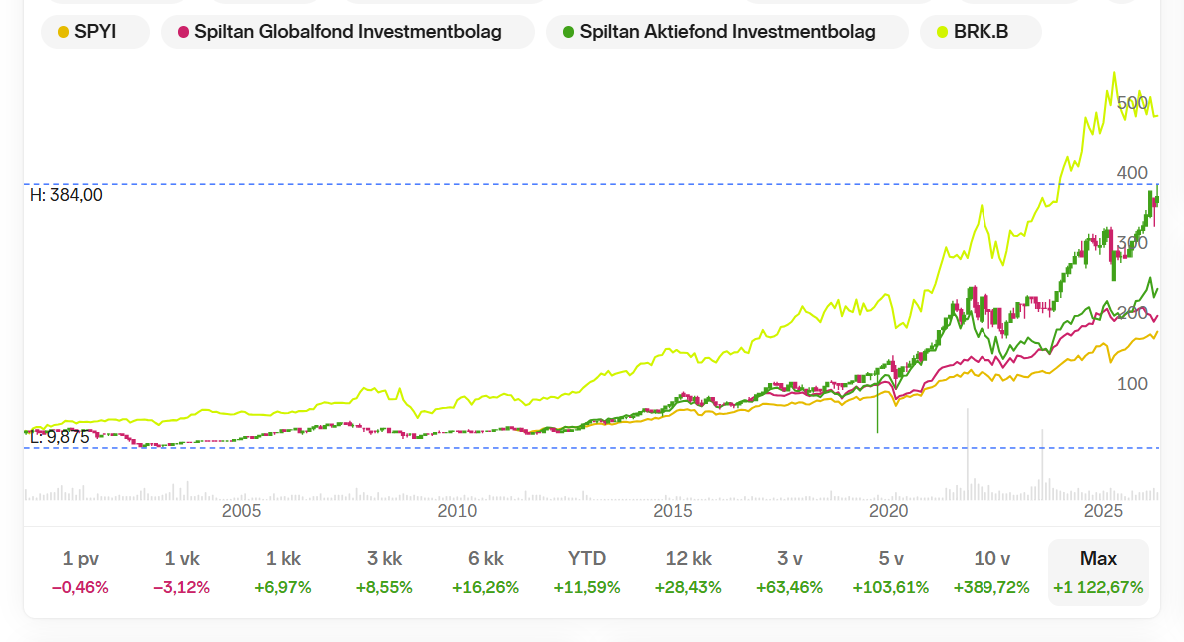

In its simplicity, the alternative presented is one of the simple ones: jump on board with those who know what they are doing. If you use the Nordnet service, comparing them is easy. Diversification has its price, but it helps you sleep better at night. In the chart, Investor is shown with candlesticks, and for comparison, Berkshire, the Spiltan Investmentbolag fund, and Spiltan Aktiefond Investmentbolag. Diversification leads to less volatility, but it comes at a cost. Just as a baseline, there is the SPYI ETF, which includes all stocks. I should note that all these investments are quite excellent/brilliant.

As for my own solution, I am invested in all of them, with Investor having the largest weight. This discussion has now sparked intentions to add to my positions.

14 Likes

I’ve been a long-time believer in Investor myself, but I have now liquidated my position. The portfolio’s valuation multiples are starting to be quite tight, and at the same time, the discount to NAV has disappeared, which is to some extent historic. As the portfolio is heavily concentrated, the benefit gained from Investor decreases somewhat when the performance of a single company (ABB) becomes so significant anyway. Investor is also not an investor that would cash out on its weaker return expectations and move capital to more attractive places; instead, it remains a steadfast owner in its portfolio companies. In that sense, it differs from, for example, BH, which does under certain circumstances cash out its listed holdings and reallocates capital to new places. I also wouldn’t be completely at ease regarding the new generation of Wallenbergs, as there really isn’t a track record yet, even though the family has historically been good at this. Who knows what kind of AI hype fanatics might have grown up there.

I suppose the main point of investing in Investor is to get into the same boat as an excellent owner. At the moment, I see the most attractive option as following the portfolio companies, and if an attractive buying opportunity opens up in one of them, one could seize it. At least you’d know the company has a high-quality owner.

6 Likes

I bought Investor before the turn of the millennium after reading an article about the company in a magazine, not an investment publication. According to it, Investor’s share is the Swedish royal family’s largest and long-term investment, and the stock has been the most profitable on the Stockholm Stock Exchange over the last hundred-year period. When I then looked into the stock’s valuation, I was surprised that the price was cheaper than the value of the shares Investor owned, even without the unlisted holdings. I immediately made a large 300 kSEK purchase and since then I have just followed the trend growth of the share price and dividends. There has been one split, and today the value of the position exceeds 300 kEUR.

Buy and hold from here on as well. The company’s discount relative to the value of its holdings has narrowed, but I would argue that the Wallenbergs’ management is not a cost but added value.

32 Likes

I started buying last year, and it’s now my largest holding at about a 16% weight. I intend to increase the weight to around 25% over the longer term. I view this as diversification against US and AI stocks, and as a better alternative to a Europe ETF. To some extent, one blindly trusts management’s ability to develop the portfolio companies, but the long-term share price performance is also quite something. If this were to go completely south, you know what, those Swedes would lose even more!

3 Likes

The CEO there is not a Wallenberg. Of the 13 people on the board, 3 are Wallenbergs, including the chairman Jacob Wallenberg (70y). So expertise will come from elsewhere than just within the family.

7 Likes

Yes – that was exactly my point. Jacob Wallenberg, Marcus Wallenberg, and Peter Wallenberg Jr. are all senior figures who have had impressive careers related to Investor. Due to the natural cycle of life, their time in the business world is coming to an end, and a new generation of Wallenbergs is stepping in.

Of course, the company’s CEO is an outsider, and there are an incredible number of other top professionals. However, if we are honest, ultimate power still rests with family representatives, both within Investor itself, on the boards of its portfolio companies, and in Swedish business more broadly. When looking at Investor’s most central portfolio companies, Jacob Wallenberg, Marcus Wallenberg, and Peter Wallenberg Jr. have been Investor’s representatives on the boards of these companies for the last 15–20 years. In Investor’s profile, the most essential work is done precisely behind the scenes of individual companies, bringing the perspective of a key owner to the decision-making. That is what long-term ownership is, and Investor has historically been excellent at it. Those are big shoes that someone needs to fill. In Investor’s case, it would be ideal if those individuals belonged to the family, as has often been the case until now. There is a different depth to decision-making when it is not just about one’s own job, but about much larger things.

8 Likes

Investor states that its management model is based on its network (nätverk), by which they mean that they know top executives on a global scale when recruiting board members for their portfolio companies. It can be flattering when a Wallenberg calls and proposes a discussion about a board membership. It is at this very stage that the family exercises its tangible power. After that, Investor’s CEO represents the family, communicating with the appointed board members about operational matters. “When you have chosen a capable board member, don’t micromanage. Trust.”

5 Likes

I checked the box “3.5% of the wife’s portfolio”. The only reason for the low weighting is that the recently started accumulation program has been on hold due to the rapid rise in price.

2 Likes