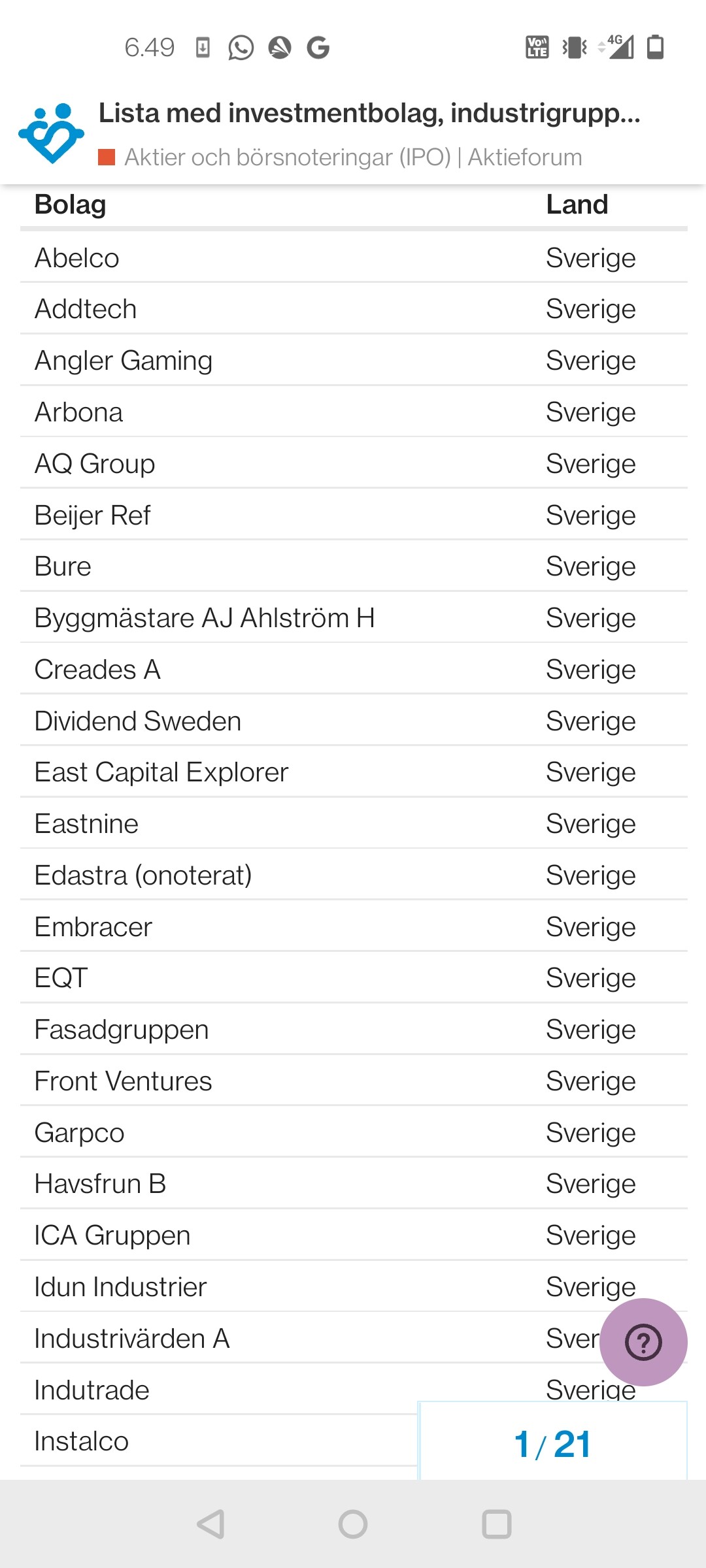

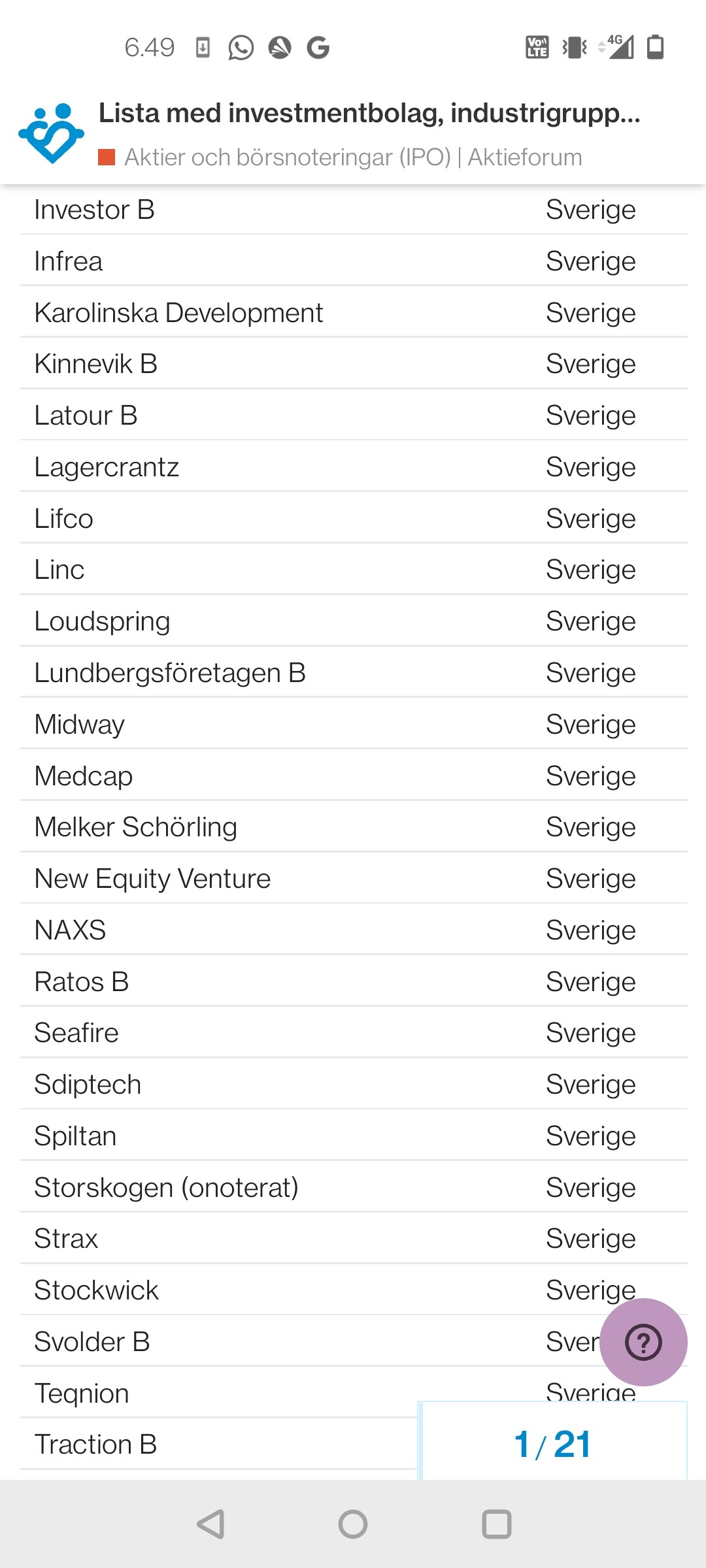

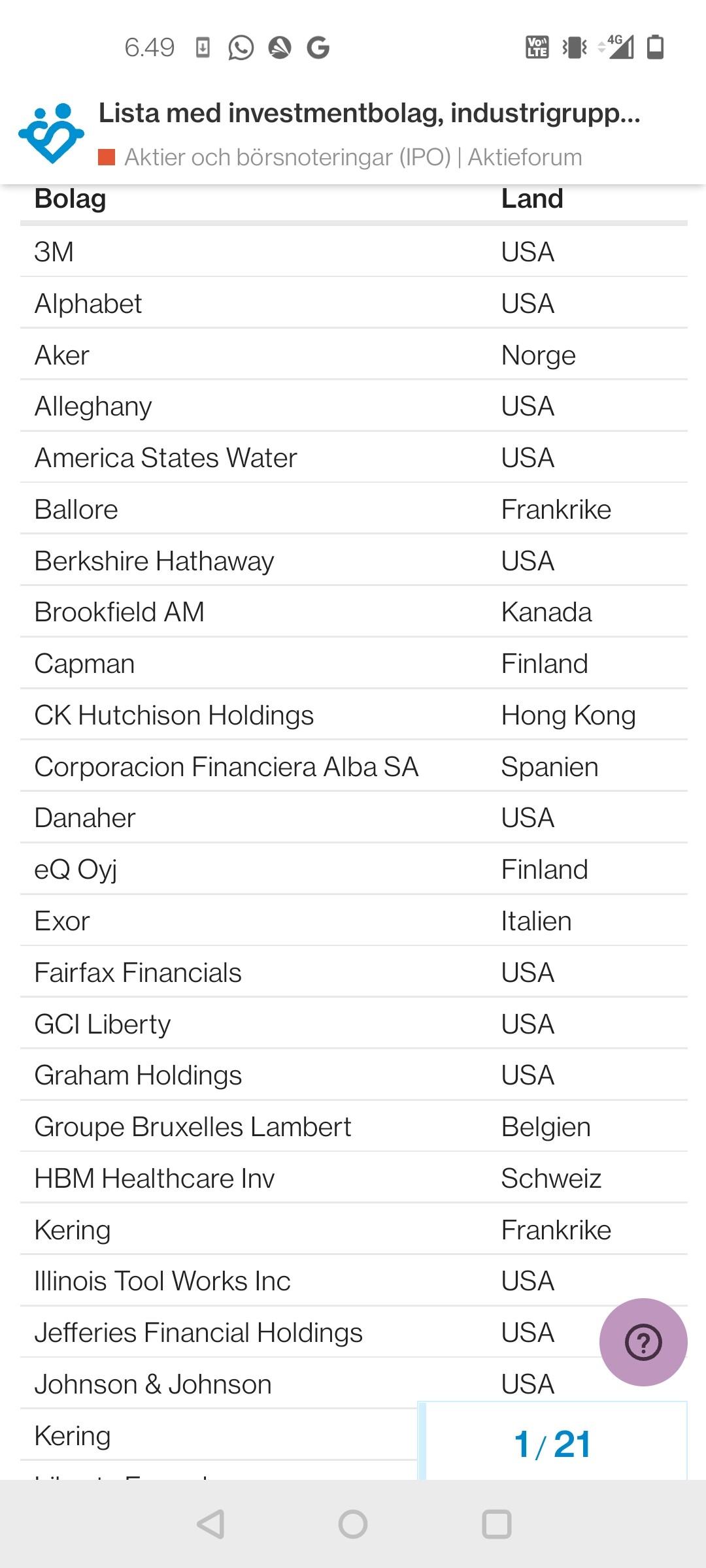

I’m opening a new thread that deals with investing in investment companies. ![]()

It is possible to build the core of a stock portfolio from one or more investment companies, which we can discuss in this thread.

Possible discussion topics include:

- Why do you invest in an investment company?

- Which investment companies have you chosen for your portfolio and which companies do you consider to be the highest quality?

- Do you have an investment company in mind that you feel hasn’t received the visibility it deserves on the forum yet and that you’d like to introduce to others?

- Do you have a buying and selling strategy you’d like to share?

- What are the advantages or disadvantages of investing in holding companies? What should be considered when investing in them?

- Thoughts on diversification?

- Just share any thoughts related to the topic

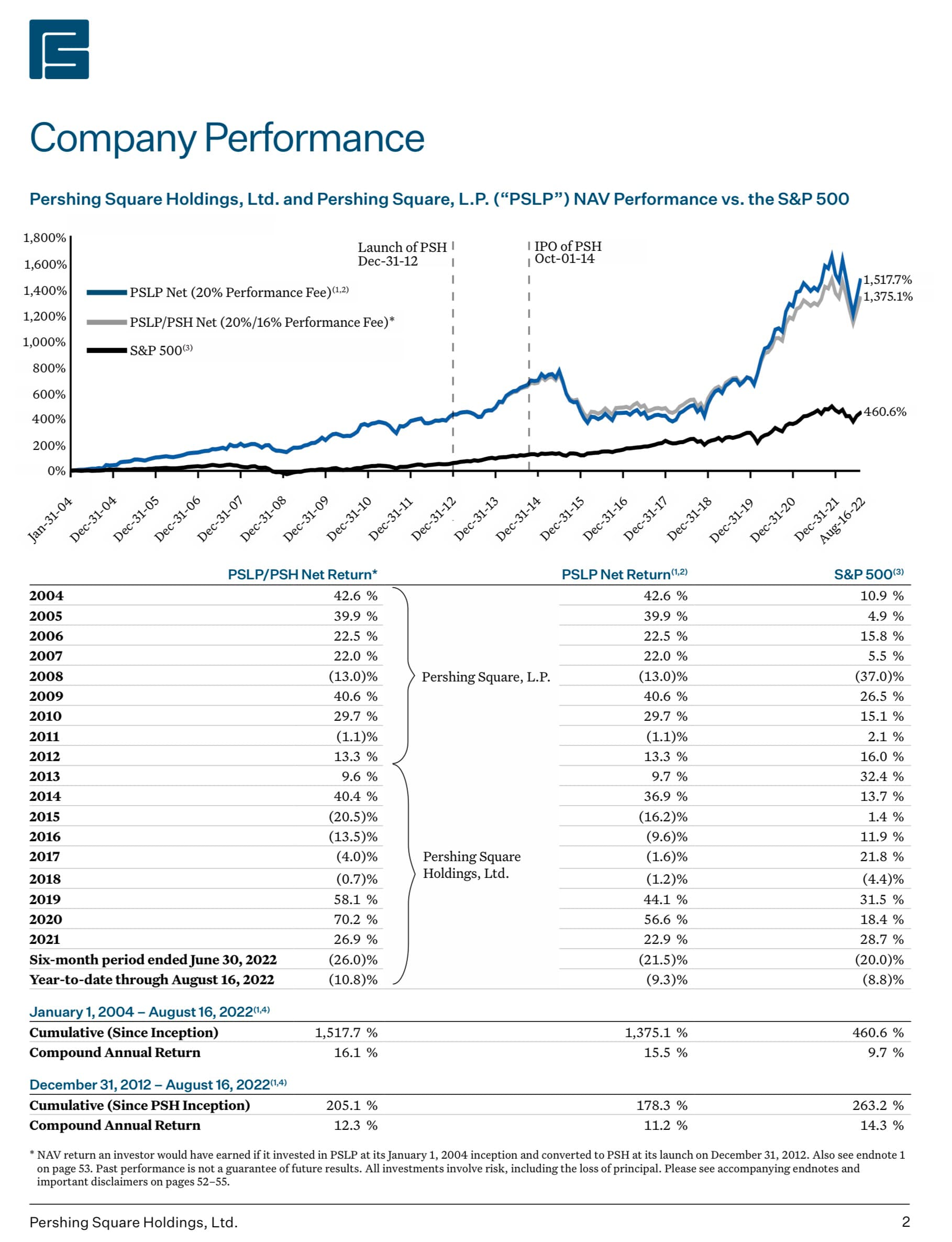

I currently own some Investor, Sievä and Sampo. Berkshire is of course also familiar, even though I don’t own it yet. I like investment companies because they generally require significantly less monitoring and oversight than “direct stocks”. A certain carefree nature, simplicity, and a diversified portfolio managed by professionals. Additionally, it’s nice to buy if you can get it below book value - a free lunch always tastes good. ![]()

It would be interesting to find new potential investment targets in this area and discuss this niche of stock investing.

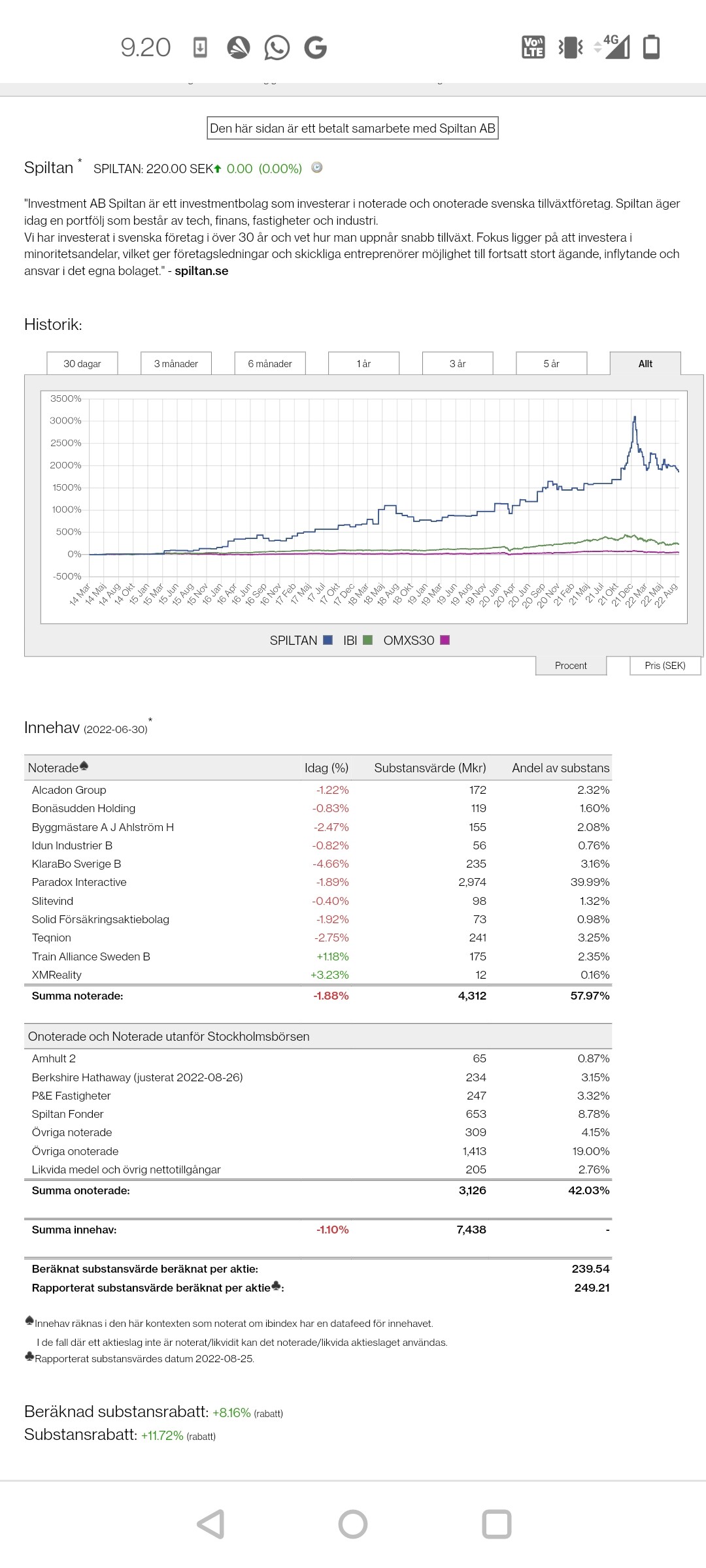

For your information, a handy link to the ibindex.se website, where it’s easy to check the nearly real-time book valuations of investment companies on the Stockholm Stock Exchange.