I recently wrote in the Note thread about their view that it’s not worth looking for acquisitions from Germany because the downturn in the automotive industry pushes players to seek growth from other sectors. This, in turn, intensifies competition and squeezes margins.

@Verneri_Pulkkinen, do you have any educated guesses as to how much the automotive industry currently has a monetary production deficit compared to some good previous years, and how the magnitude of this production deficit relates to new defense, infrastructure, etc. investments?

I noticed that Lacon seems to be not only in the defense sector but also heavily in public infrastructure, such as rail transport. If we assume, in a basic model, that large investments are made in infrastructure and defense that replace or even surpass the lost automotive industry production, then Lacon is, at least based on its references, quite reasonably positioned. Of course, Lacon’s revenue has decreased, so that also tells us something. However, if it had increased, how much higher would the price tag have been?

I consider this a good purchase in the sense that an opening in Germany has been desired for years. I don’t remember how many years it has been since it was mentioned that the key targets for establishing our own facility are the USA and Germany. Now both have been taken care of, and the geographical coverage is exceptionally well diversified.

I have also started to lean towards the view that NOTE’s Lind-Widestam is an optimistic speedster. When things are going well (usually with his own company), he exults that this is just the beginning and things will only get better soon (lately they haven’t). And when things are going badly somewhere in the EMS sector, then… well… the beginning of the end. In the stock market, excellent returns are often made when one knows how to buy something valuable whose price is not high because others don’t consider it valuable. I don’t know anything about buying companies, but could the same logic apply there?

Lacon’s price is not cheap, but it’s not really expensive either. If it provides significant exposure to Germany’s and other Central European’s expanding infrastructure and defense investments, now might be a good time to make such a deal.

Without taking a strong stance on whether Note’s or Incap’s view on the multidimensional question is more correct, I cannot, however, believe that the reflections of the German automotive industry’s problems on the EMS sector would remain only within Germany’s borders. Goods, however, move mostly freely in mainland Europe, and the automotive industry’s supply chains are complex and multidimensional, so surely this should be more widely visible in Europe. So far, Nordic EMS companies have achieved relatively healthy profitability in Europe, whereas challenges have likely been more on the side of volume growth than margins (i.e., prices).

The automotive industry is largely high volume / low mix production, where different players are strong compared to Nordic contract manufacturers focused on high mix / low volume (of course, this is just a general rule and, to my understanding, Incap also supplies products to the automotive industry, at least from Slovakia). The transition also doesn’t happen overnight, but as the demand problems of the big players persist, overcapacity naturally tends to spill over, in one way or another, to other tables as well.

Regarding Incap, it would be interesting to hear how the free trade agreement between India and the EU affects Incap. As I understand it, volumes at the Indian factories are already high, but there is still plenty of capacity for expansion. @Antti_Viljakainen, it would be great to hear your comments on this.

Free trade is definitely positive for export companies like Incap, especially in the long run. In the short term, however, there may not necessarily be direct effects that are radically visible in the figures, unless the trade agreement acts as a specific trigger for a customer to shift production to India.

Europe is the largest market for Incap’s Indian factory (i.e., the lion’s share of VE deliveries), and there is capacity to take on more customers. Comments from the India factory visit, where this topic was touched upon, can be found here.

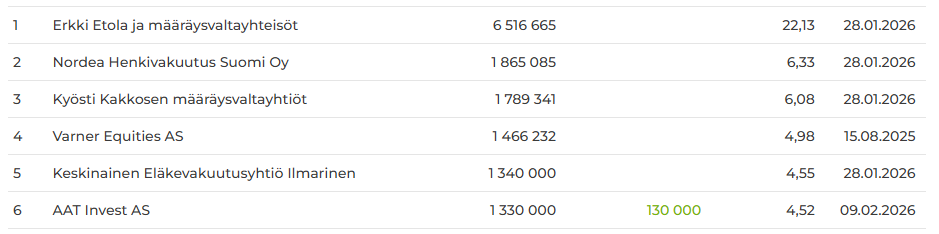

The Norwegian guy has snapped up some more shares for his portfolio again, 130,000 shares this time.

Seems like a pretty smart guy based on the article, and he must be since he’s also invested in Incap

for many making money as investors, a big problem is that they want to do it quickly without looking for so-called “reasonably priced stocks where the herd is not.”

Incap Group’s financial statements release for January–December 2025 will be published on Thursday, 26 February 2026 at approximately 9:00. Finnish and English reporting materials will be available at that time on the company’s website at https://incapcorp.com/fi/raportit-ja-esitykset/.

Webcast

The company will hold a webcast in English on Thursday, 26 February 2026 starting at 11:00. The results will be presented by Incap Corporation’s President and CEO Otto Pukk and CFO Antti Pynnönen.

During the webcast, questions can be submitted through the webcast platform’s Q&A function at the address mentioned above. Questions can also be addressed to President and CEO Otto Pukk and CFO Antti Pynnönen here in the Inderes discussion forum. The answers will be published on the company’s own website and in this discussion thread.

Incap Group’s financial statements release for January–December 2025 will be published on Thursday, 26 February 2026 at approximately 9:00 EET. At that time, reporting materials in Finnish and English will be available on the company’s website at https://incapcorp.com/reports-and-presentations/.

Webcast

The company will hold a webcast on Thursday, 26 February 2026 at 11:00 EET. The result will be presented by Incap Corporation’s President and CEO Otto Pukk and CFO Antti Pynnönen.

During the webcast, questions can be asked through the webcast Q&A function at the address mentioned above. Questions can also be addressed to President and CEO Otto Pukk and CFO Antti Pynnönen here in the Inderes discussion forum. The answers will be published on the company’s website and in this thread.

Recent years have been quite volatile for Incap. Quarterly revenue growth fluctuated between +40% and -30% during 2024-25. The most recent headwinds were related to US tariffs imposed on India. Growth was -16% y/y in Q3 2025, but revenue growth could be as high as +53% y/y in Q3 2026 due to the Lacon acquisition. Overall, in our view, it makes sense for Incap to acquire new customers in order to broaden its customer portfolio and smooth out operational volatility. Reduced volatility and improved predictability could also support the company’s valuation multiples. Our fair value range remains at EUR 11.7-14.3 per share, based on our DCF analysis and backed by a peer group comparison. Incap’s 2026E P/E and EV/EBIT combined are currently 35% below the peer group median.

Here are the preview comments from Antti ahead of Incap’s Q4 results on Thursday.

We expect the company’s Q4 figures to have declined quite clearly from the strong comparison period, as Europe’s sluggish economic situation, US trade policy uncertainty, and currency exchange rates have slowed down the business. However, the main focus of the report will be the 2026 guidance, which, to meet expectations, should indicate clear growth in both revenue and operating profit (including inorganic support from the recently completed Lacon acquisition). Incap is unlikely to pay a dividend this year either, as the company will likely allocate its capital toward executing its growth strategy.

Hanza is an interesting company. Hanza also seems to have had a very impressive stock performance over a one-year period.

To my eye, the website also looks a bit more professional than Incap’s. Ultimately, performance is what counts, of course, but I don’t understand that clowning around at all. P.S. I still own way too much Incap and I really hope the company starts performing at Hanza’s level.

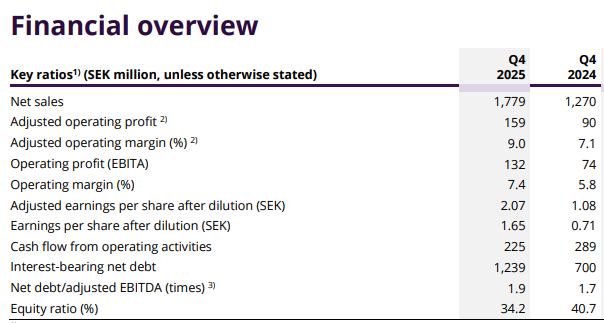

Revenue for the fourth quarter of 2025 was EUR 55.3 million (10–12/2024: EUR 59.3 million). This was a decrease of 6.7% from the comparison period. At comparable exchange rates, revenue was EUR 58.8 million, representing a 0.1% decrease from the comparison period.

Operating profit (EBIT) was EUR 6.9 million (EUR 8.6 million), or 12.5% of revenue (14.4%). This was a decrease of 19.4% from the comparison period.

Adjusted operating profit (EBIT) was EUR 8.0 million (EUR 8.9 million), or 14.4% of revenue (14.9%). This was a decrease of 10.2% from the comparison period.

Net profit for the period was EUR 5.1 million (EUR 7.8 million).

January–December 2025 highlights

Revenue was EUR 214.6 million (1–12/2024: EUR 230.1 million). This was a decrease of 6.7% from the comparison period. At comparable exchange rates, revenue was EUR 221.2 million, representing a 3.9% decrease from the comparison period.

Operating profit (EBIT) was EUR 25.3 million (EUR 29.2 million), or 11.8% of revenue (12.7%). This was a decrease of 13.3% from the comparison period.

Adjusted operating profit (EBIT) was EUR 26.1 million (EUR 30.1 million), or 12.1% of revenue (13.1%). This was a decrease of 13.5% from the comparison period.

Net profit for the period was EUR 14.0 million (EUR 22.7 million).

Earnings per share was EUR 0.47 (EUR 0.77).

In December 2025, Incap signed an agreement to acquire Lacon Group, an electronics manufacturing services (EMS) provider and original design manufacturer (ODM), with production in Germany and Romania. The acquisition was completed in February 2026, and Lacon Group’s figures will be consolidated into Incap Group’s reporting starting from 20 February 2026.

Incap Corp.’s Board of Directors proposes to the Annual General Meeting that no dividend be paid for the 2025 financial year. Incap is focusing on organic and inorganic growth, and the company has a clear plan for potential M&A targets.

“Incap’s Q4 revenue was in line with our expectations, but adjusted profitability clearly exceeded our forecasts, supported by a strong product mix. Exchange rates masked the stability of organic demand, as at constant currencies, revenue was practically at the level of the comparison period. The guidance for 2026 was as expected and indicates clear growth supported by the Lacon acquisition.

Revenue in line with our expectations – currencies mask organic stability

Q4 revenue of EUR 55.3 million was practically in line with our estimate (EUR 55.7 million) and decreased by 6.7% from the comparison period. Adjusted for exchange rates, however, the decline was only 0.1%, indicating that organic demand was practically stable. Revenue rose by 6.8% from Q3, supporting the company’s previous comment that the bottoming out of demand occurred in Q3. Full-year revenue of EUR 214.6 million was practically exactly in line with our estimate (EUR 215 million).

Q4 adjusted operating profit of EUR 8.0 million (margin 14.4%) exceeded our estimate of EUR 6.6 million by about 21%. The margin remained close to the level of the comparison period (14.9%) on significantly lower revenue, which is an excellent performance in the EMS industry. The positive impact of the product mix likely explains part of the beat, as on a quarterly level, the mix can fluctuate relative profitability significantly. Full-year adjusted operating profit of EUR 26.1 million exceeded our estimate (EUR 24.7 million) by about 6%, and the beat was specifically weighted toward Q4.

One-off items and bottom lines

In Q4, EUR 0.9 million in one-off items were recorded, which likely relate to the preparation of the Lacon acquisition. These weighed on the reported operating profit (EUR 6.9 million), which still exceeded our estimate (EUR 6.5 million). Full-year EPS of EUR 0.47 was exactly in line with our estimate, even though the full-year net profit (EUR 14.0 million) decreased by 38.5% from the comparison period – the difference is explained by exceptionally favorable exchange rate effects in financial items during the comparison period.

Guidance as expected – Lacon raises 2026 figures

The company expects 2026 revenue and comparable EBITA to be “clearly higher” than in 2025. The wording is as expected and includes the inorganic impact of the Lacon acquisition completed in February. The guidance includes the usual reservation for unexpected changes in the business environment, which is noteworthy especially as uncertainty in US trade policy continues. No dividend will be paid; instead, capital will be allocated to implementing the growth strategy – as we expected.”

Great result! I was anxiously waiting to see what would come out, but we got a solid result with a good outlook. Now I can press the coffee maker’s power button without a worry.