I thought I’d open my own thread for IBM, which I’ve been following more or less actively for almost 20 years.

The company certainly needs no introduction; founded 109 years ago, its history includes countless turns and products that make the IBM brand very well known even today. If we fast-forward to the events of the last couple of years, the markets are currently following these things in particular:

In the spring, Indian-born Arvind Krishna started as the company’s CEO, from whom a rainmaker like Satya Nadella (Microsoft’s CEO) is certainly hoped for. Compared to his predecessor Ginny Rometty, Arvind is more of a technology person, and he is supported by Jim Whitehurst, who served as RedHat’s CEO until spring.

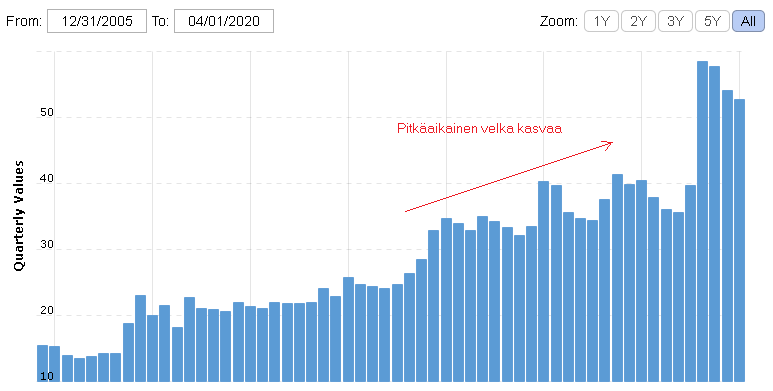

IBM acquired RedHat two years ago for $34 billion in the largest acquisition in its history. To finance this transaction, IBM has heavily indebted itself. RedHat is not being integrated into the rest of IBM but operates as an independent company.

RedHat’s business is growing, but it accounts for less than 10% of the entire company’s revenue, and the growth is not enough to compensate for the contraction of other parts of the company.

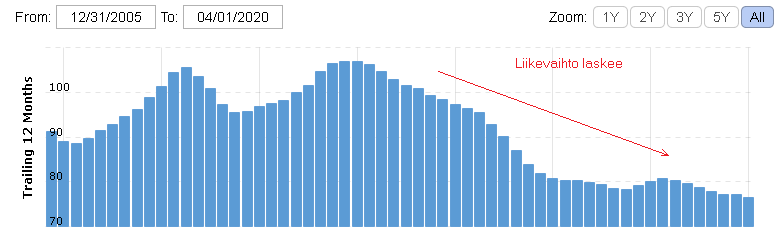

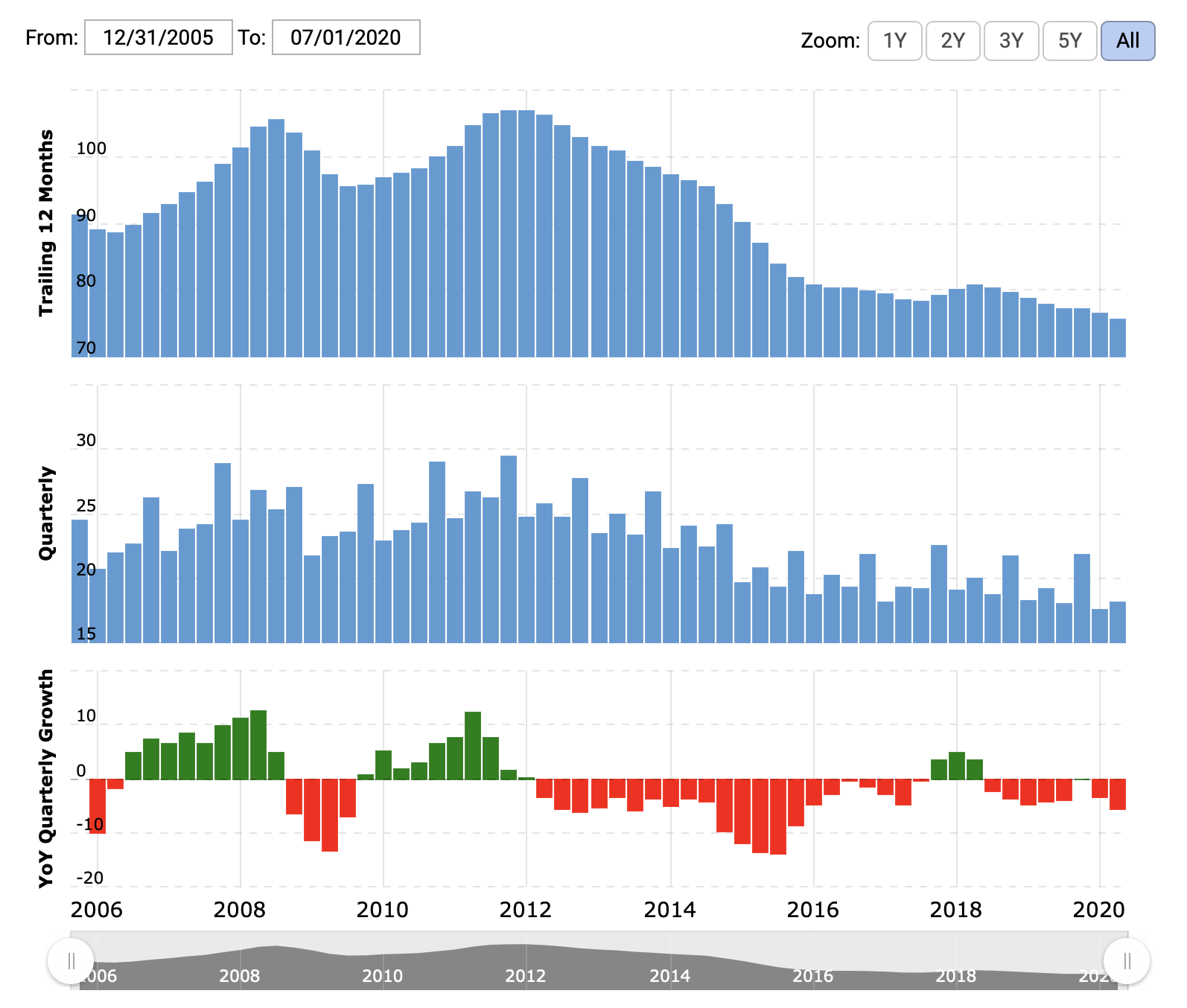

For the past 10 years, the company’s traditional cornerstones (IT outsourcing business, i.e., GTS, traditional software, hardware) have shrunk as cloud solutions have taken over the markets. IBM has built its own IBM Cloud offering both organically and by acquiring companies (e.g., Softlayer in 2013), but it has fallen far behind AWS, Azure, Google Cloud, and other medium-sized players.

About 5 years ago, the company made significant investments in the healthcare sector under the Watson Health brand, aiming to combine IBM’s technology solutions (e.g., Watson AI) with healthcare industry solutions (e.g., Truven Analytics, Explorys, Phytel, Merge Healthcare, and many other acquisitions). These have not been discussed much lately.

The company will report its Q2 results among the first on July 20, 2020.

From SeekingAlpha, one recent analysis of the company can be highlighted, which quite commendably dissects the company’s Q1 results and financial position:

A difficult place to innovate… Cloud providers have taken off, and the consulting market is also divided among small local firms. The legacy market is slowly melting away. On the other hand, there’s a huge amount of fat to cut, meaning numbers can be improved by restructuring and buying revenue.

Looking at stock prices, CGI and even Fujitsu have performed better?!

I personally wouldn’t touch this legacy side from an investment perspective. Except I do have MSFT, which benefits a lot from this mainframe/server farm → cloud scenario.

In recent years, IBM has possibly even risen to become the world’s number one (no metric offered for this) in the development of quantum computers. They also have a few quantum computers ready, and it’s even possible to code programs for some of them via the internet, if quantum coding is successful.

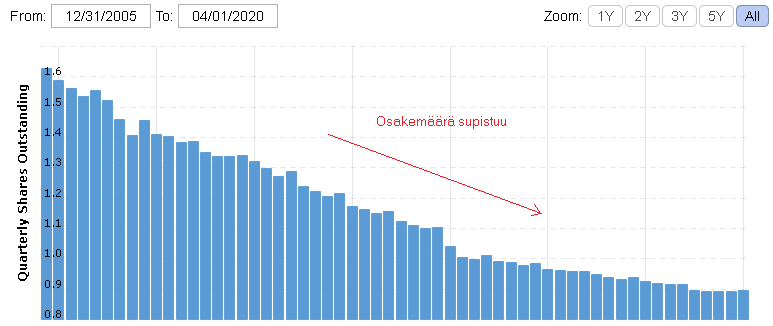

It doesn’t help even if they generate 30% free cash flow for the market capitalization. Do I want to be involved with a company that truly squanders its earned money on share buybacks at these multiples? This is a common problem with American companies in general. If you’re dissatisfied with the share price development, try paying a 30% dividend. In practice, investors are left watching a painfully slow-growing dividend while the share price stagnates and the debt burden increases.

Oksaharju probably recommended IBM years ago, and I joined in too. It’s been a miserable investment; even considering dividends, it’s still slightly at a loss. I don’t know if it’s worth selling at the current price, as long as the company remains a dividend aristocrat. The dividend alone brings a very good return, and a price increase would be a bonus.

Good analysis, thanks @Juippi. IBM has indeed been wasting its funds for years by buying huge amounts of its own shares, which has kept earnings per share at a very good level while revenue has been contracting. At the same time, its main competitors have increased their R&D budget many times over, while IBM’s budget is still hovering around 6 billion, where it was 13 years ago.

As for IBM’s investments in quantum computers, this is an unknown card whose significance is still difficult to assess. There is a lot of hype-generated magic dust around quantum computing, and it must be remembered that quantum computers are not general-purpose like traditional computers, but are suitable for specific use cases. According to the CNET article below, the quantum computing market would be “only” 9 billion dollars at the end of the decade, which is a rather insignificant market compared to the general cloud market.

Yep, back in the day, they said there’d only ever be one supercomputer the size of a house, and that would be it. Or something along those lines. Now you can get a better computer even from the market, one that can’t even be compared.

IBM’s and, for example, Google’s approach to quantum technology is generally quite different.

Here’s an article explaining the matter (critically regarding IBM):

The size of the market will only become clear once we know what can actually be achieved with quantum computing in the first commercial applications. Personally, I don’t trust such estimates, as they cannot be based on anything sensible. If these breakthroughs, for example, in encryption technology, then the defense sector in different countries alone will gladly pay that 9 billion in total. On the other hand, it’s also probably known that commercial applications are not yet coming to market in the very near future.

Well, the first games have already been made for a quantum computer. Secondly, my vision for the future is that the “smarter” cities become, the more dynamic the control of cities and traffic will be. Dynamic processes might benefit from quantum mechanics. Or maybe not. I haven’t delved very deep into the matter.

IBM suspended share buybacks a year ago. With the freed-up cash flow, it accelerated the repayment of debt related to the Red Hat acquisition. The company estimated, in connection with its Q2 announcement, that its free cash flow would be approximately $12 billion this year. Dividends will consume about $5.5 billion of that. It is certain that dividend increases will be nominal in the coming years. However, debt will decrease substantially.

IBM’s Q2 report didn’t promise a major turnaround yet, even though both revenue and profit exceeded the very low consensus estimates. The -5.5% decline in revenue compared to last year’s Q2 continues the cycle of contracting revenue that began in 2012.

By the way, don’t be fooled by the “Total Cloud revenue” included in the earnings reports. It’s a distortion caused by tagging, which creates the impression of a growing cloud business. This figure includes business from all units (GBS, GTS, Systems, and Cloud & Cognitive SW) that is somehow related to the cloud. IBM’s own public cloud revenue is included in the Cloud & Cog SW unit’s figures, and that unit’s revenue grew by a mere 3%.

IBM:s rapidly growing cloud business has not received the appreciation it deserves. Since most of the revenue comes from segments with declining revenue, the valuation multiples for the entire company have remained low compared to other cloud operators.

The solution announced yesterday to split the company in two seems very promising. This could create a lot of value.

Interesting news. This is also a historically significant turning point, as during IBM’s major crisis in the 90s, splitting IBM into pieces was strongly on the table, but the then-CEO Lou Gerstner decided to keep the company together. History showed Gerstner’s decision was correct then; now we’ll have to wait a few years to see how things turn out this time.

However, I wouldn’t start celebrating just yet. The GTS (Global Technology Services) being spun off from IBM now was indeed the company’s least profitable part and experienced the biggest decline in revenue. However, it hasn’t been the root cause of IBM’s dismal struggles in cloud services, at least in recent years. Of course, this change will free up some resources (financial + human) to develop IBM’s core business.

Turning a ship around is slow, with revenue continuing its familiar decline in Q3. Forecasts had already been screwed down so low a couple of weeks ago that there were no surprises left.

This is how I’ve understood it. As far as I know, the entire share capital of NewCo will be distributed to existing IBM shareholders, and IBM itself won’t even remain a minority shareholder. In this respect, it differs from, for example, the sale of the PC business in 2005, when IBM became a significant owner of Lenovo (I recall with about a 20% stake).

Regarding dividends, it has been promised that the combined dividends of the remaining IBM and NewCo would be at or above the current dividend level. Of course, this should not be taken too seriously, as NewCo, as an independent company, can decide on a completely different dividend strategy.

Another significant piece of news related to IBM is that a major staff reduction program was launched in November in Europe, affecting about 10,000 employees, which is about 15-20% of the European headcount. The organization is also being streamlined in the United States, apparently on a slightly smaller scale.

The thing works exactly as @PureProfit said. More information can be found in IBM’s own press release:

The proposed separation is expected to be effected through a pro-rata spin-off to IBM

shareowners that will be tax-free for U.S. federal income tax purposes. The transaction is

subject to customary closing conditions, including Form 10 registration with the U.S. Securities

and Exchange Commission, receipt of a tax opinion from counsel, and final approval by IBM’s

Board of Directors. The separation is currently expected to be completed by the end of 2021.

“Pro-rata spin-off” practically means a situation where the old owners of a company receive shares of the new company in the same proportion as they own shares of the old company (i.e., if you own 1% of the old company → you also own the same 1% of the new company).