Greetings to the forum,

I thought I’d open a thread for this German food industry player. Below is some information and my own thoughts on the company. The screenshots are from the company’s own CMD presentations. Let’s see if we can get a discussion going; if so, I can write more later, at least about the risks and competitors.

What does HelloFresh do?

HelloFresh is originally a German food industry player that sells meal kit packages to consumers as a weekly subscription service. HelloFresh customers receive 2-5 meals per week delivered to their homes. Recipes for these meals are delivered, along with pre-measured ingredients, which the customer can cook themselves at home. HelloFresh has already expanded to 17 countries, including all Nordic countries except Finland. In Finland, similar meal kits are sold by many much smaller local companies.

HelloFresh has several brands under which the service is sold. Most sales occur under the HelloFresh brand, and this brand has become almost synonymous with similar meal kits in several markets. Meals marketed under the HelloFresh brand cost, for example, about €4-5 per meal in its home market of Germany. In addition, HelloFresh has the EveryPlate brand in certain markets, which focuses on a lower price point, GreenChef, which focuses on organic and vegan portions at a higher price, and Factor, which sells ready-to-eat meals delivered to homes. Smaller brands include Chef’s Plate and the recently acquired Youfoodz.

HelloFresh can maintain higher margins compared to traditional grocery stores for three reasons. Firstly, HelloFresh buys raw ingredients directly from producers, eliminating intermediaries from the chain. Secondly, HelloFresh can optimize its processes so that food waste is only a fraction of what traditional grocery stores produce. Thirdly, HelloFresh’s production processes are refined and automated so that inventory levels are consistently very low and net working capital is negative.

HelloFresh’s customer acquisition has been optimized so that, on average, a new customer acquired for the subscription service repays the marketing costs associated with customer acquisition in about three months, thanks to strong unit economics. This is one of HelloFresh’s greatest strengths.

HelloFresh’s stock is listed on the Frankfurt Stock Exchange under the ticker HFG and was included in the DAX index last year.

Xetra

Yahoo Finance

Recent History and Future

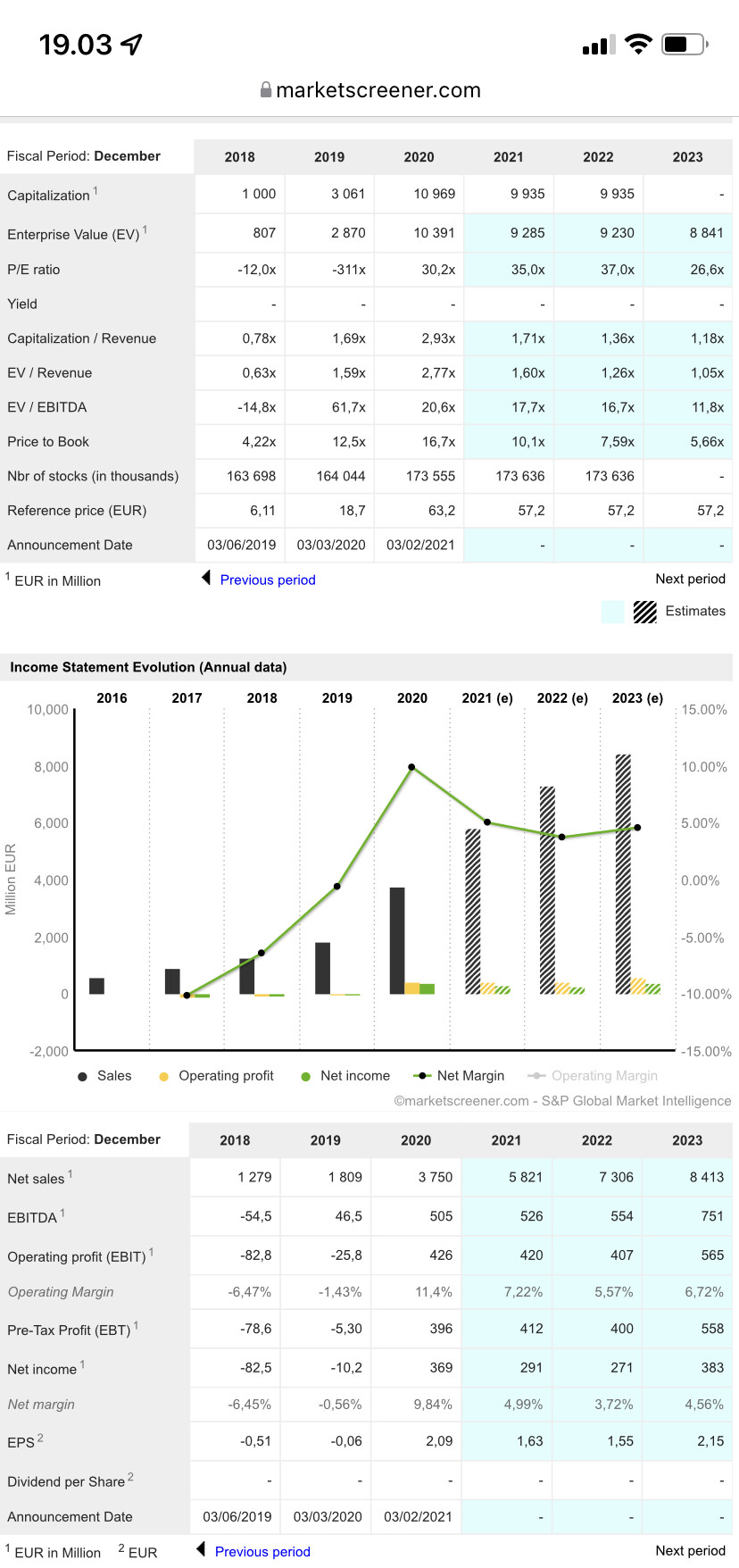

HelloFresh turned its operations (adjusted EBITDA) profitable in 2019, just before the COVID-19 pandemic provided a significant tailwind for the company in 2020. Revenue grew from €1.8 billion in 2019 to €3.8 billion in 2020. Last year’s revenue looks set to rise to around €5.9 billion.

Adjusted EBITDA has also grown to over €500 million in 2020 and 2021 despite significant growth investments.

For the current year, HelloFresh has guided for 20-26% revenue growth, driven by new geographical openings. Margins, however, are guided for slight downward pressure due to inflation (HelloFresh has stated it will not raise prices and will instead focus on revenue growth at the expense of grocery stores) and burdened by large growth investments (developing the technology team, opening and automating new distribution centers).

Long-Term Growth Strategies

In the longer term, HelloFresh has stated its goal of achieving €10 billion in revenue and a 10-15% adjusted EBITDA margin by 2025. Of these, at least the revenue target seems easily achievable, and the company has shown it can also maintain high margins if it so desires.

Future growth will come from several sources:

- Geographical expansion to 2-3 new markets per year. Last year, for example, services were launched in Norway, Japan, and Italy.

- Offering additional services to existing customers, e.g., in the form of desserts, extra portions, breakfasts, and the HelloFresh Market (ordering individual ingredients outside of recipes) already trialed in the Benelux countries.

- Bringing brands already launched in the USA to Europe and other markets. Of these, Green Chef and Factor, in particular, look promising.

- Improved margins through automation of distribution centers and better utilization rates as the scale increases.

Competitive Advantages

HelloFresh has managed to outperform almost all competitors in many markets. Notable among these is Blue Apron, which was still the market leader in the USA market a few years ago but now only generates a fraction of HelloFresh’s sales. Nor have traditional grocery stores yet found a way to compete with a similar service, despite numerous attempts.

HelloFresh’s best competitive advantage is its brand, which in many markets is a “top-of-mind” brand when it comes to meal kit services. In many countries, this is due to a first-mover advantage, but in America, for example, the company has managed to displace strong local competitors after entering the market later.

Now that HelloFresh has grown to be clearly the largest player, economies of scale and process optimization are a big part of their competitive advantage. Smaller players cannot compete on price, and those traditional grocery stores that could drive down prices have not adapted to a similar service due to HelloFresh’s unique logistics. Data utilization is also one of HelloFresh’s strengths, and the recipe selection can be optimized for customers using data and artificial intelligence.

A weakness is the easy substitutability of the service. If a more attractive competing product appears on the market, consumers can easily switch to a new service with as little as a week’s notice. On the other hand, the evolving digital services of traditional grocery stores may close HelloFresh’s digital lead.

Valuation and Return on Capital

The stock price has fallen significantly in recent weeks and is just under €60 at the time of writing, which means a market capitalization of approximately €10.3 billion. Based on the results of the last 12 months, this means (based on my own calculations) the following multiples:

P/E = 30x

EV/EBITDA = 20x

EV/S = 1.9x (drops to 1.8x if Q4 results meet guidance)

Return on capital has been at a high level since the beginning of 2020. Below are the key figures at the time of writing based on the results of the last 12 months.

ROE = 41.4%

ROIC = 31.6%

ROA = 16.4%

Additional Material

HelloFresh IR pages

Business Breakdown podcast about the company (highly recommended for those interested)

2020 CMD slides

2021 CMD slides