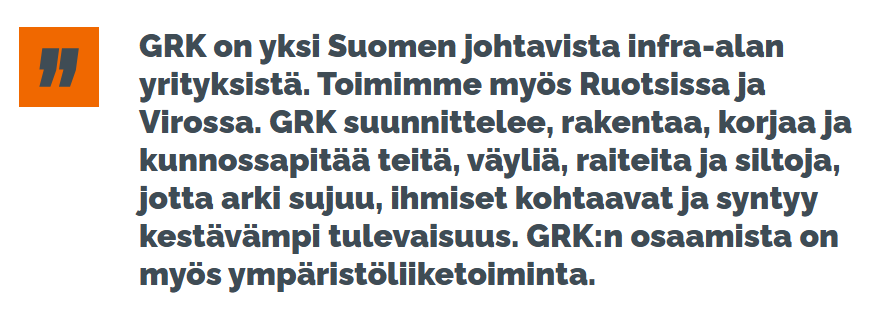

GRK Infra Oyj plans an initial public offering and sale, and to list its shares on the Nasdaq Helsinki stock exchange list. GRK is a Finnish infrastructure construction group operating in Finland, Sweden, and Estonia. GRK’s core expertise lies in the execution of diverse infrastructure construction projects, project management for large and small projects, and extensive railway expertise.

Listing announcement

The stock listing has been awaited for several years; here are the latest articles:

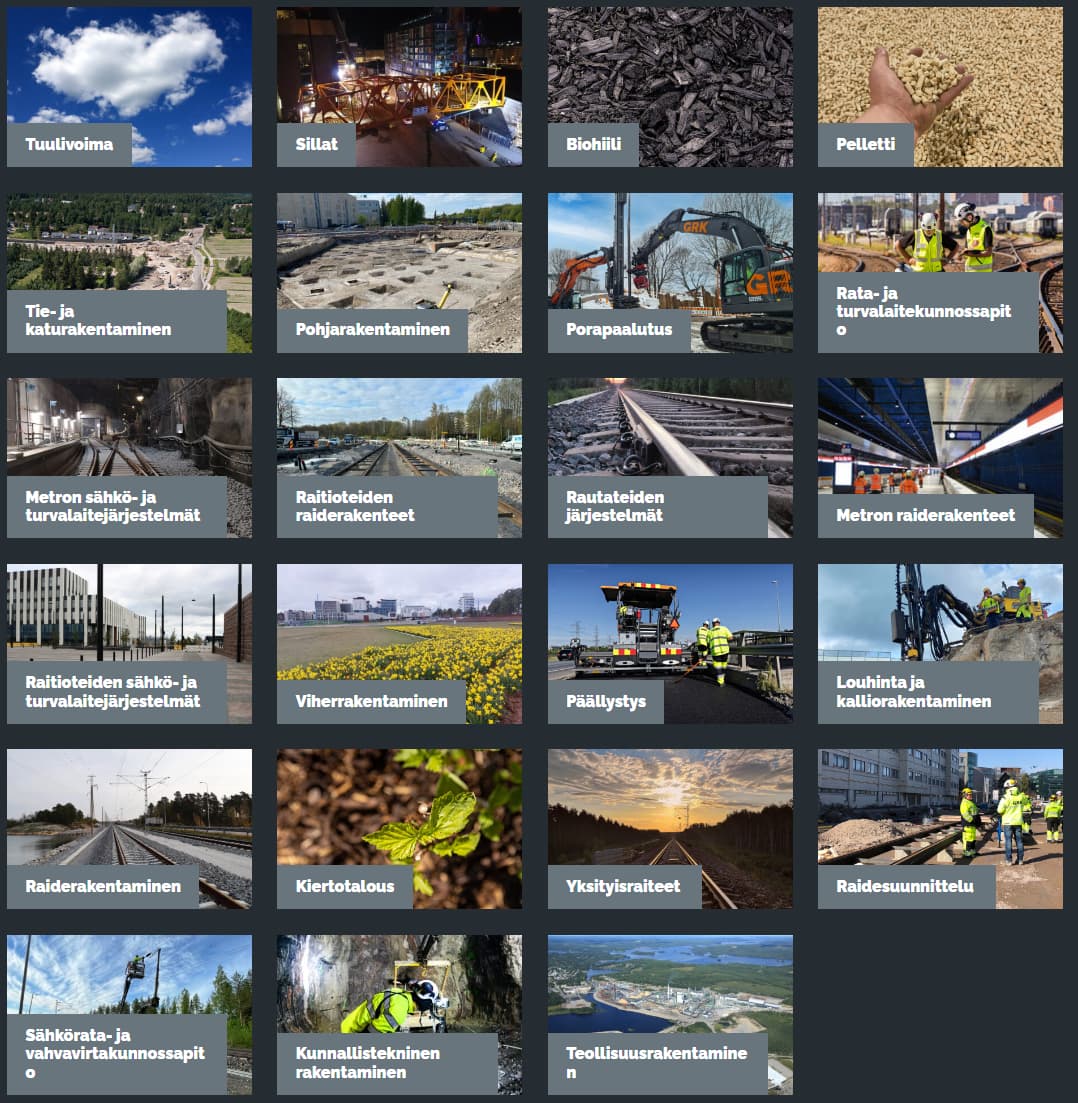

Services:

GRK’s core expertise includes the execution of diverse infrastructure construction projects, project management for large

projects, and extensive railway expertise.GRK offers services from design to construction and maintenance. Our clients include

state administration, municipalities and cities, and the private sector. GRK operates in several projects

in cooperation with other companies in the infrastructure sector.

The service selection is at least comprehensive

Company Structure

The GRK Group consists of the parent company GRK Infra Oyj and three country companies in Finland, Sweden, and Estonia.

GRK Infra Oyj acts as the parent company of the group, employing the group’s administration. Business operations are carried out by the country companies.

In Finland, GRK Suomi Oy is responsible for business operations, whose services include civil engineering and road construction, paving, rail business, and environmental business.

- Parent company GRK Infra Oyj, which owns the country companies

- The country company operating in Finland is GRK Suomi Oy

- The country company operating in Sweden is GRK Sverige AB

- The country company operating in Estonia is GRK Eesti AS

2024 figures from the earnings release

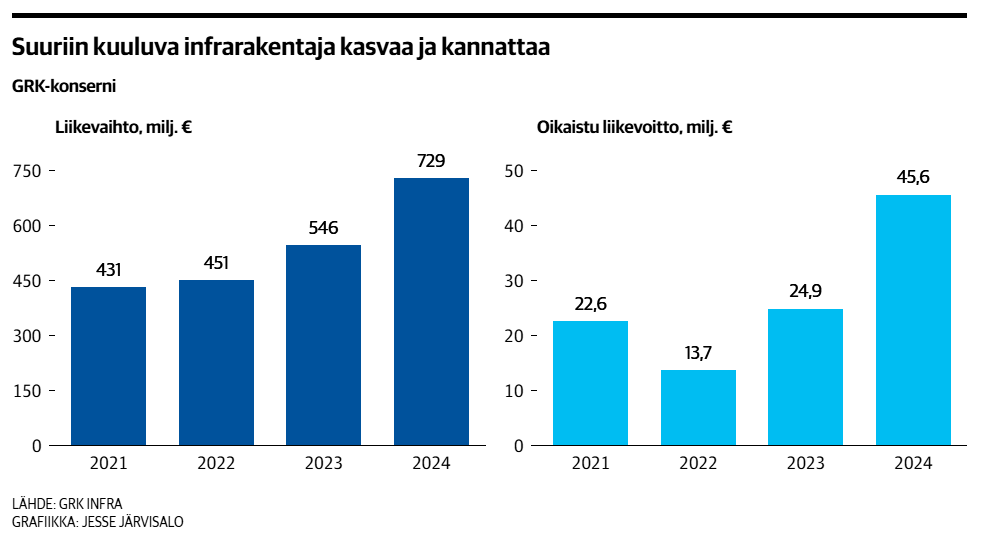

Revenue grew significantly, operating profit almost doubled

January-December 2024 in brief (IFRS):

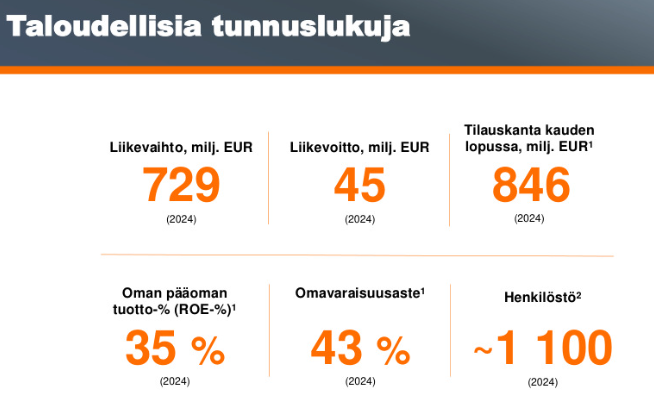

- Revenue grew by approximately 33 percent to EUR 728.6 (546.2) million.

- Adjusted EBITDA was EUR 61.3 (38.0) million, or 8.4 (7.0) percent of revenue.

- EBITDA was EUR 60.9 (37.7) million, or 8.4 (6.9) percent of revenue.

- Adjusted operating profit was EUR 45.6 (24.9) million, or 6.3 (4.6) percent of revenue.

- Operating profit was EUR 45.2 (24.2) million, or 6.2 (4.4) percent of revenue.

- Equity ratio was 42.9 (39.9) percent.

- Return on capital employed was 150.1 % (47.8 %) percent.

- Order book grew to EUR 845.6 (568.3) million at year-end.