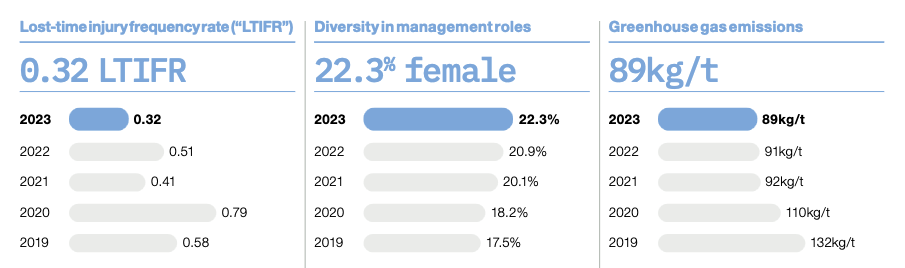

Ferrexpo is the world’s third-largest producer of iron ore pellets. The iron ore pellets produced by the company are high-quality (65%/67% Fe) and have low carbon emissions (89kg/t):

Ferrexpo has three operational mines and a processing plant in the Poltava region, far from the front lines. In addition, the company has many untapped deposits and unexplored opportunities for additional mining operations in the surrounding area, so the company’s mining operations have a bright future.

Iron pellets are transported from the mining area abroad primarily through a port located near Odesa, so keeping maritime connections open is critical for Ferrexpo. Some volume can also be transported via the Danube and through rail connections to Europe, but Ukraine has only a limited amount of rail capacity, and without functioning sea routes, production must be restricted significantly.

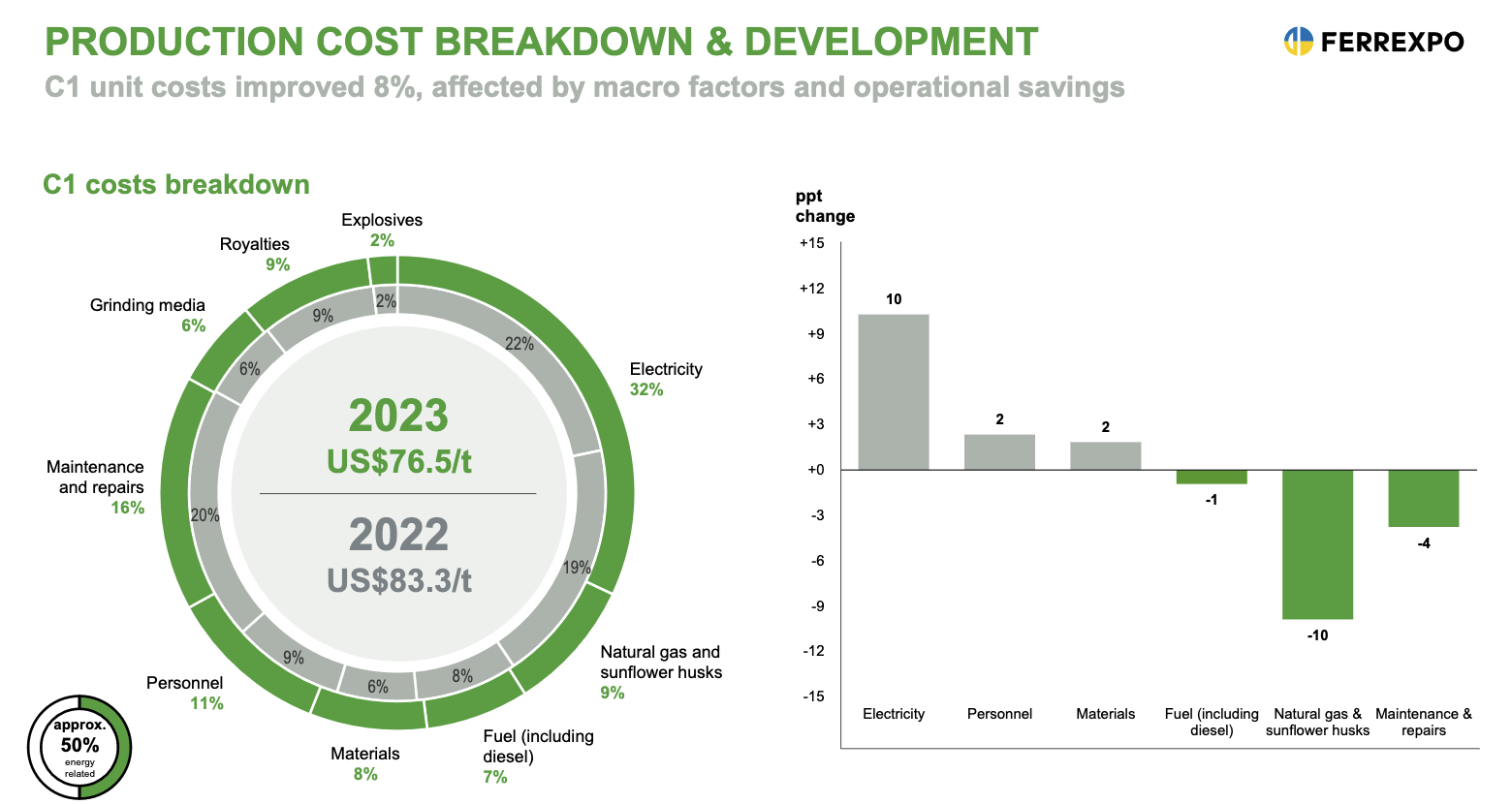

The cost profile of the mines is very moderate, and there is plenty of room to cut costs as production scales up and the war ends. About half of the costs are due to energy expenses, so unfortunately, Russian missile strikes against Ukraine’s energy infrastructure are weighing on the company’s cost side.

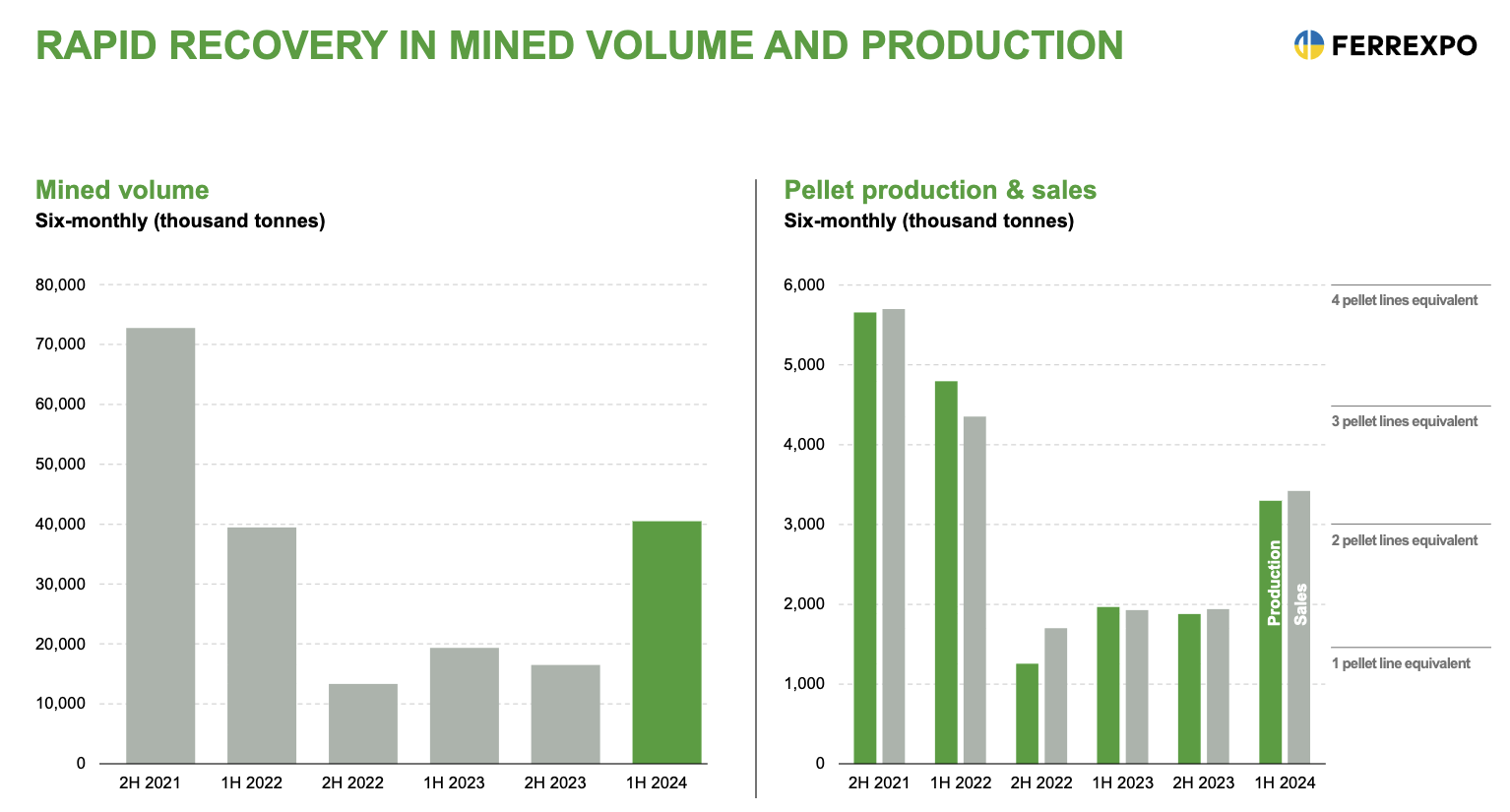

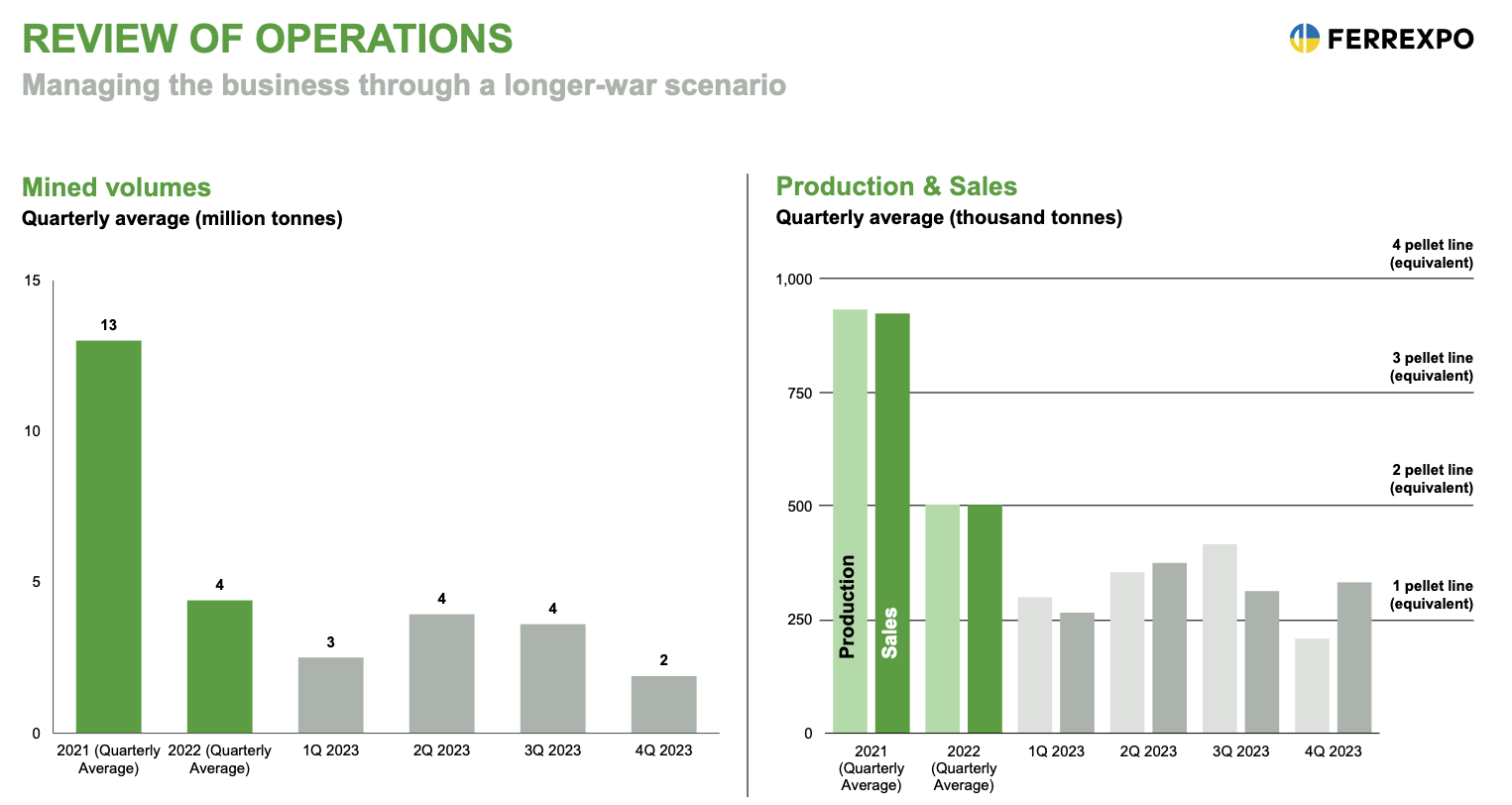

The production and sale of iron pellets has suffered immensely due to the war in Ukraine, and the company’s four pellet lines are significantly underutilized. Production is limited by, among other things, electricity supply, availability of transport equipment, labor availability, the mobilization of workers to the front, and workers moving to Western Ukraine for fear of a Russian breakthrough.

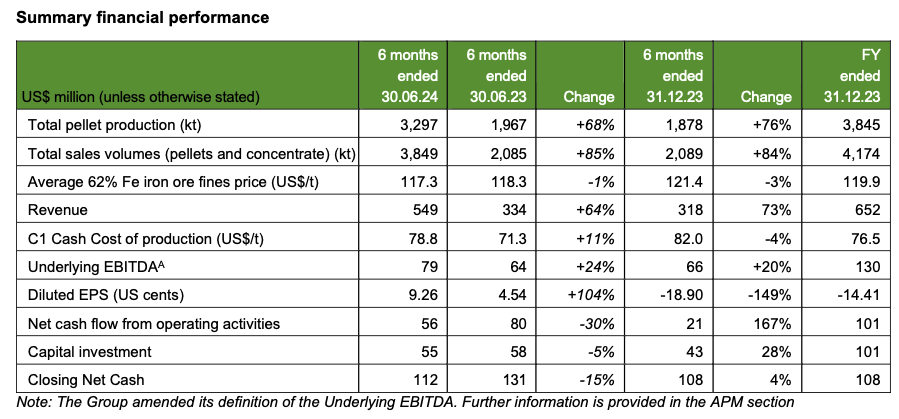

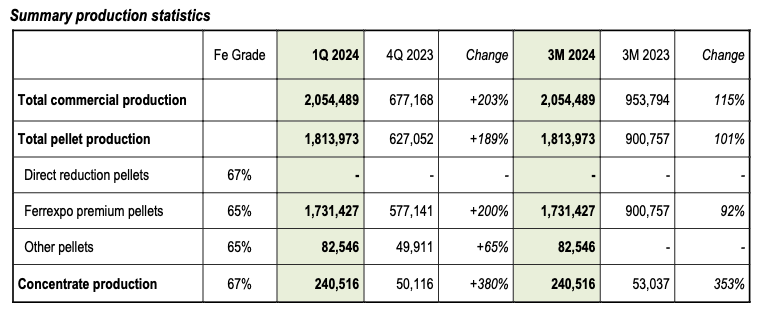

Fortunately, 24Q1 began to show clear signs of recovery in production as the company finally begins to demonstrate an ability to adapt to the wartime situation and Black Sea shipping routes have started to function. Production grew by +200%, and just under two million tonnes of pellets were produced in the quarter, which is already a respectable figure, as before the war production was about three million tonnes per quarter.

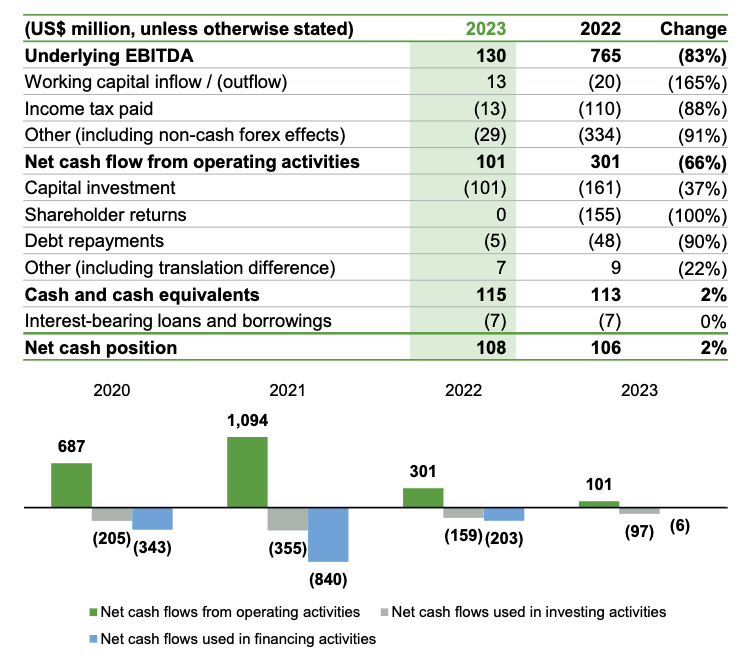

If production continues at these high levels, Ferrexpo will be deeply profitable. Operations could generate a cash flow of +500 MUSD, with a nice amount remaining even after mandatory investments (-100 MUSD – -150 MUSD). The company’s market value at the time of writing is just under 400 MUSD, so it is a true value stock.

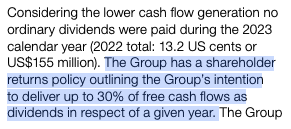

Most importantly, strong cash flow would enable the resumption of dividend payments. The plan is to pay out 30% of Free Cash Flow as dividends, so the “investor’s paycheck” could be quite substantial at these share prices.

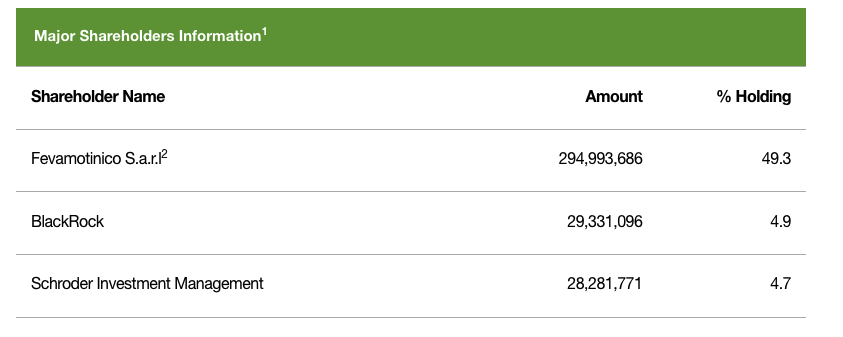

The company’s ownership structure is somewhat messy. Founder-oligarch Kostyantyn Zhevago, who owns about half of the firm, is in exile in France, and the Ukrainian state seized his holdings in late 2022. The management has changed at a rapid pace, and former executives have faced corruption and other charges at such a rate that it is somewhat unclear to me who actually owns the company. Ukraine is a quite corrupt country, so there is some degree of risk regarding the nationalization of the company or the misappropriation of funds.

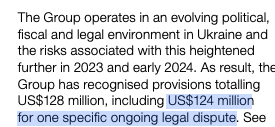

Ferrexpo has a vast number of various legal cases ongoing, but of critical importance is particularly a 124 MUSD dispute that the company has lost in lower courts and whose next Supreme Court hearing is on May 27th. Losing that would be disastrous for the company’s stock price and could lead to unpredictable consequences.

Despite all the corruption and war, ESG efforts are progressing. Ferrexpo aims to halve carbon emissions by 2030 and achieve net-zero emissions by 2050.

This company genuinely has ten-bagger potential. If you have the knowledge, the skill, the courage, and that famous vision, an armchair general could potentially forge massive returns from this stock ![]()

Investor materials:

https://www.ferrexpo.com/investors/results-reports-and-presentations/

Investor calendar:

https://www.ferrexpo.com/investors/financial-calendar/