Emeco (Earth Moving Equipment COmpany) Holdings Limited is an Australian company founded in 1972 that provides mining equipment rental, mining services, and spare parts and maintenance services.

According to the company, they offer around 1,000 units of various rental equipment, stating: “With the world’s largest mining rental fleet, combined with Force’s rebuild capability, Emeco provides cost and pricing advantages that enable us to capture market share.”

The company went public in 2006.

Emeco’s fiscal year ends on June 30th, and the company reports semi-annually.

Emeco’s CEO is Ian Testrow, who joined the company in 2005 and has served as CEO since 2015. (Testrow’s shareholding is ~3%, total insider ownership is ~4%).

Market Cap: $392M AUD (Jan 27, 2023)

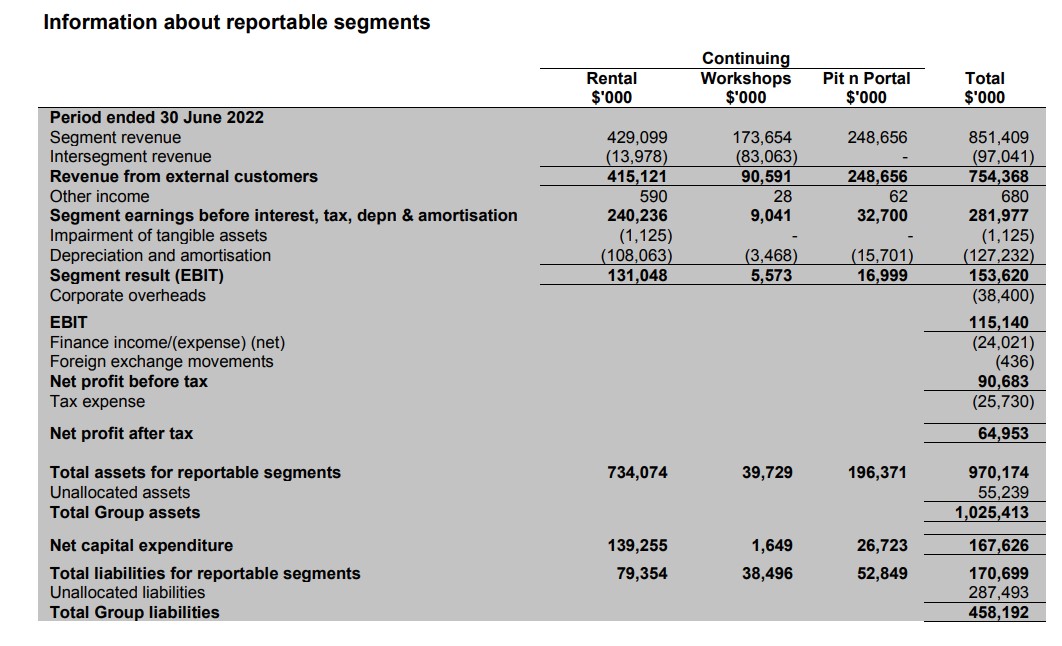

Revenue: $754.4M

EBITDA: $245.7M

EBIT: $115.1M

Net Profit: $65M

(FY2022 figures, fiscal year ended June 30, 2022)

Website:

Operations were expanded abroad even before the IPO. Geographic expansion continued after listing, but by 2018, all international operations had been divested. Instead, the company has continued to grow in its home country through acquisitions.

Emeco was loss-making from fiscal year 2013 to 2018, after which earnings have remained positive and the balance sheet has strengthened. Dividends, which were suspended in spring 2013, were reinstated in autumn 2021. Free cash flow has also been at a good level since FY2018, with the exception of a weaker FY2019.

Debt resulting from corporate restructurings has been refinanced on better terms in recent years, and loan repayments and acquisitions have been partly funded by equity raisings. Consequently, the number of shares has increased significantly: 261,720,000 shares in FY2018 vs. 535,493,000 in FY2022. (The figures account for the 10:1 reverse stock split on Oct 27, 2018.)

As of June 30, 2022, net debt was $245.5M AUD, and interest expenses in FY22 were $21.6M AUD vs. $33.8M AUD in FY21.

During FY2022, in September 2021, share buybacks were initiated. During the fiscal year, 17 million shares were repurchased at an average price of $0.90 AUD, totaling $15.6M AUD. Buybacks have continued into H1/2023.

Emeco has three segments:

- Rental (Equipment rental)

- Pit N Portal (Mining services, including equipment rental)

- Workshops (Maintenance and spare parts services, external and internal)

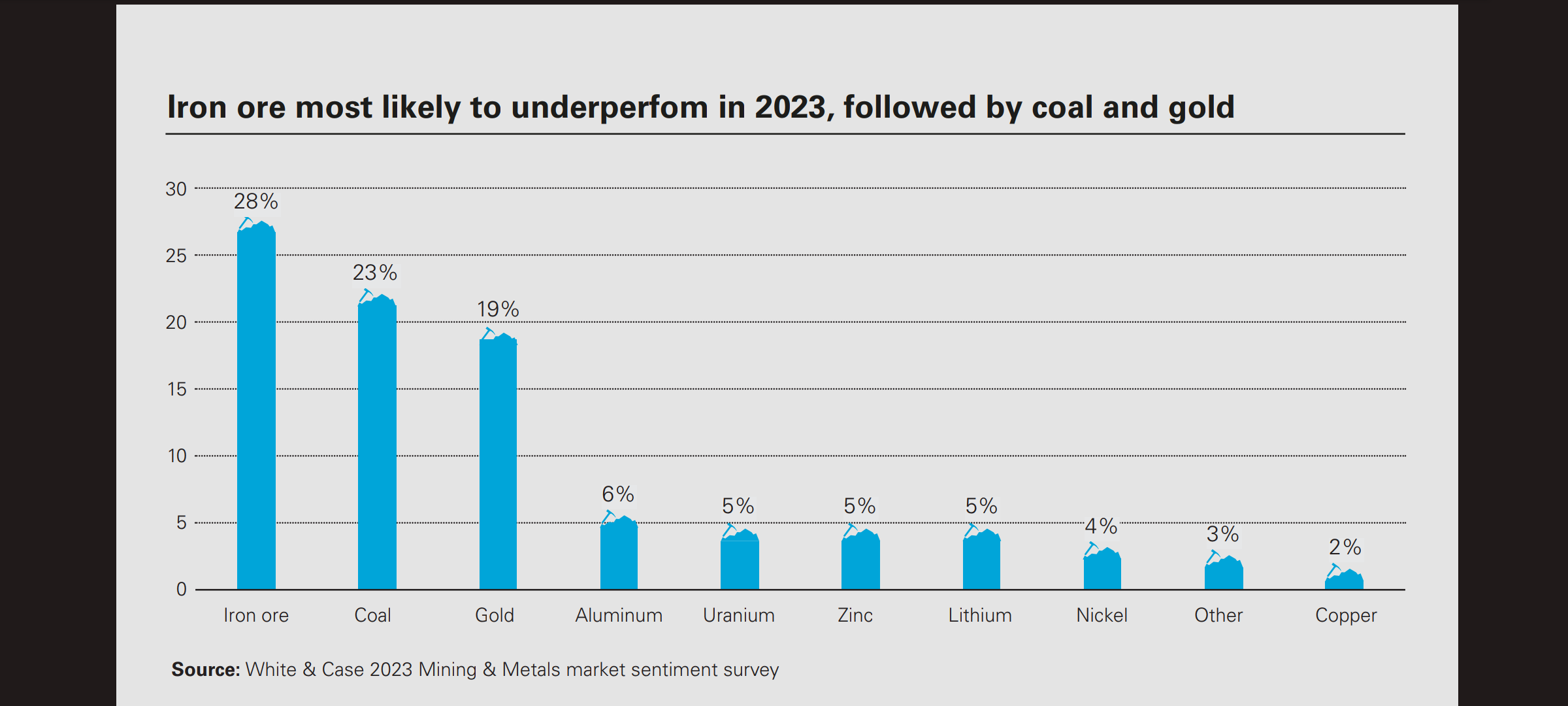

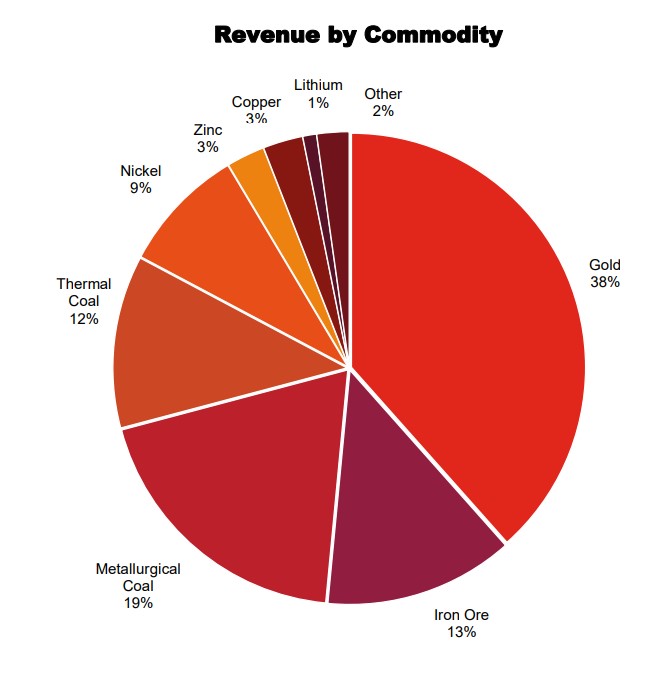

Pie chart of customer distribution by commodity at the end of FY2022. (According to the FY2021 investor presentation, there were over 150 customers):

Value trap?

The stock price has been in a freefall since the IPO, so why wouldn’t the same trend continue in the future?

The company has returned to the home market from its overseas adventures, and the debt burden of past years has been (almost) shed. There are positive signs in the air, such as the aforementioned share buybacks and cancellations, the reinstatement of dividends after a years-long break, a streak of positive earnings, strong cash flow, and FY2023 guidance: “We therefore are providing full year guidance of between $245 to $260 million.” (= Operating EBITDA, FY2022 $250M)

Not much seems to be expected of Emeco, but it likely doesn’t need to achieve much at this valuation level.

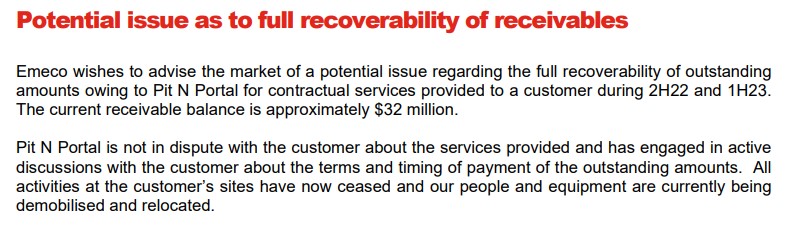

The guidance above does not account for the October 2022 announcement regarding a $32M doubtful debt from a Pit N Portal customer.

“We are very disappointed by this given our historically low levels of credit losses.” (From the CEO’s AGM speech on Nov 17, 2022)

I tried googling Emeco’s total market size and searching through investor presentations, but I haven’t found a clear answer yet; I’ll likely have to inquire with them directly.

There seem to be several competitors; Emeco only appears on the second page of Google for the search term “australia mining equipment rental.” I’ll need to look into these more closely as well.

Here, Mark Ackroyd, CEO of a competitor, National Group, lists the benefits of equipment rental for mining operators: https://www.australiahqj.com/2021/07/21/the-benefits-of-equipment-rental-in-the-mining-industry-according-to-national-group/

This is my first post on the forum; I hope this scratch-the-surface overview makes some sense ![]() I’m happy to receive any feedback and corrections to any factual errors.

I’m happy to receive any feedback and corrections to any factual errors.

P.S. There is some discussion about Emeco on the Australian investment forum https://hotcopper.com.au/, if you’re interested.

P.P.S. Disclaimer: I bought my first Emeco shares today, Jan 27, 2023, before the crack of dawn.