Maybe those customer-specific prices don’t need to be pulled out of thin air:

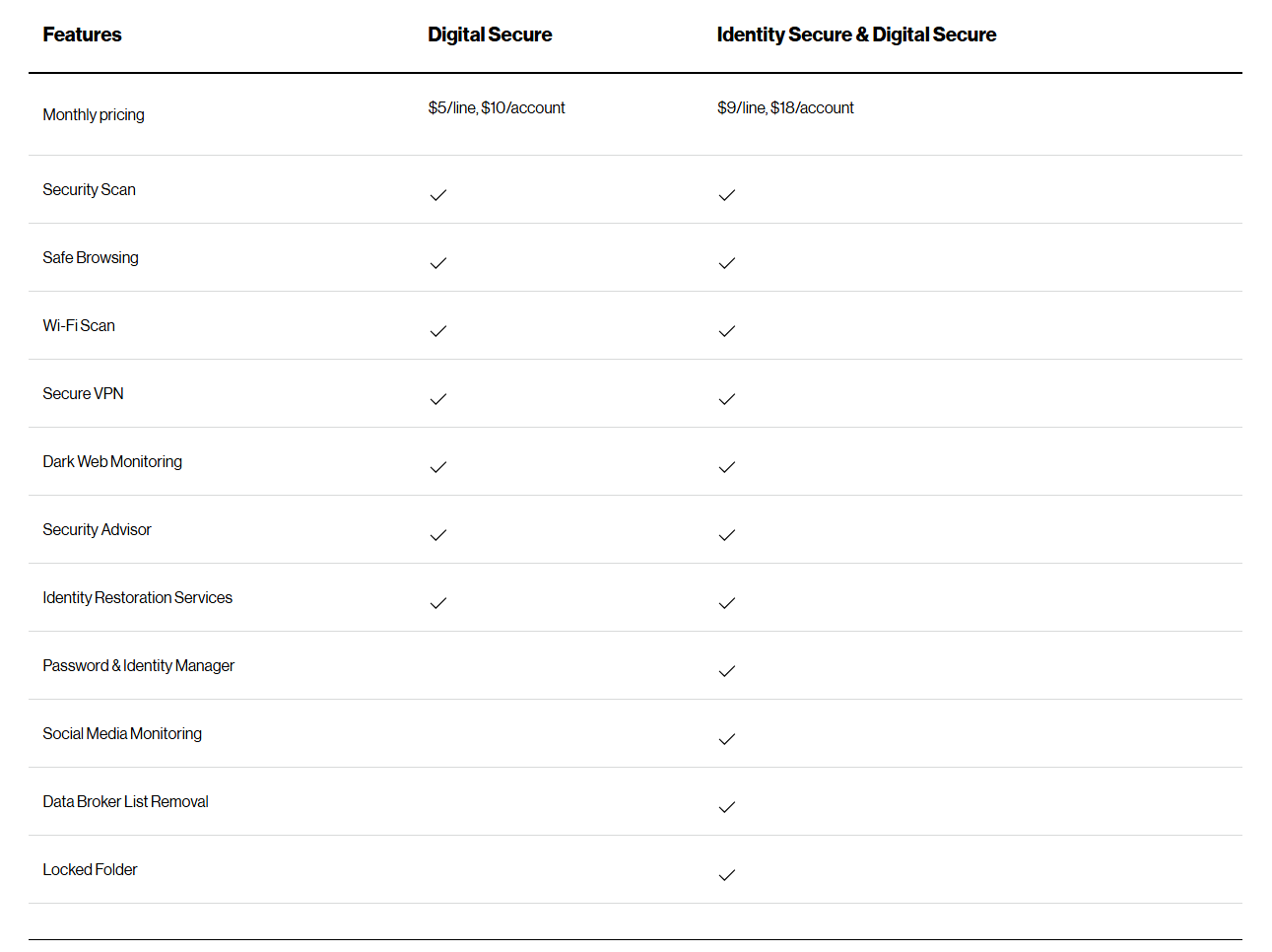

If we now assume that Verizon, for instance, keeps half of the price for themselves (likely a pessimistic assumption from F-Secure’s perspective) and assume an average monthly fee per customer of, say, $14/account. Then 15M/year → would give a little over 2M subscribers. So that’s the order of magnitude. Well, that half for Verizon should certainly motivate them quite a bit to add more customers (of course they have costs from this too, but the margin is likely quite nice).

So, with these estimates, one could see potential for even 10x growth regarding this customer account.

In any case, the magnitude is likely in that 1-10% range, and probably closer to the lower end than the upper end.

As for what the so-called full realistic potential of this account could be, that causes a bit of uncertainty. There is a difference here between an account and the term ‘line’. Verizon says they have 146.6M “total wireless retail connections” and 16.8M “fixed wireless access and fiber broadband connections” (Verizon Fact Sheet | About Verizon). So there are probably many accounts that include multiple connections (they are pushing hard to sell bundles of fixed internet + phones, or even all the household’s phones for one price). Of course, the broader the package, the more it pays for them to offer a little extra as a bonus, such as cybersecurity. For F-Secure, I would imagine the revenue comes primarily through accounts, I presume.

And now it’s good to remember that this is just one Tier 1 account.

No matter how you look at it, there is clearly potential for significant growth here.