This could be a good target. Strong and well-known brands, at least here in Finland, and the fact that toilet paper is also needed when the chips are down and the economy isn’t doing well. I’ll have to start monitoring it and researching it a bit more closely. What could be behind the recent share price development?

Right now, it feels like all stocks that are even slightly on the rise have the same kind of climax. You shouldn’t invest based on the shape of a graph, but it immediately gives me bad vibes.

Excellent company. I have been a shareholder of Essity after its spinoff from SCA.

This company ticks all my boxes: defensive, good leadership, brands etc. Only problem, as with the rest of the market, a bit pricey for my taste at the moment, even though SEK is rather weak. I rather own Essity than Kimberly-Clark.

This is a long term investement for me (as is also Visa, Sampo, Novo Nordisk). Will increase my share holdings in the future for sure.

If someone wants to add Essity be sure to follow insider trading (to get an idea of a good entry point), as their have been in recent years rather broad activity (not only the usual suspect buying like the CEO) and most have been adding (very few if none have been selling). I think the latest purchase was around 270-280 SEK.

I usually use Finansinspektionens register to look for insider trading patterns.

Essity is definitely a company that I would like to own. I completely agree with you, the stock seems to be a bit pricey despite the decent growth in net sales. I will most likely open my Essity position if the share price drops below 270 SEK.

At least aging population, longer life expectancy, growth in world population and income(Essity is present on emerging markets) as well as increased awareness of the importance of hygiene(emerging markets). How well these trends will translate to revenue growth for Essity is of course a more difficult question.

STOCKHOLM (Nyhetsbyrån Direkt) Louise Svanberg, board member of Essity, bought 3,100 B-shares in the hygiene products company on Wednesday.

This is according to a report to the Financial Supervisory Authority’s insider register.

The purchase was made at a price of 306 kronor and was thus worth almost 1 million kronor.

Louise Svanberg, who previously was CEO of the language course company EF and who was elected to Essity’s board in 2016, owns 15,000 shares in Essity, according to the company’s website. It is not stated when this information was last updated.

Revenue decreased from last year, but increased from Q2. Profitability improved and the goal is to increase it further.

The B-share dipped surprisingly much, even though the dividend will be paid next week. The A-share, with lower trading volume, stayed at its levels better.

Essity’s results, published at the end of last month, were pretty much in line with the previous year. The share price has been sluggish, even though the company is financially sound and has stable sales. Perhaps the company is a bit boring… I’ve been wondering if I should sell my shares and seek a better return.

Essity is by its nature a ‘boring’ company. But for me its one of the best quality companies in the Nordics (I am a value, long-term investor.)

If you have a long-term time horizon and have the patience to wait owning this share it will eventually prove to be successful.

The short term catalyst: the end of the worldwide corona lockdowns, which will increase the use of Essity products (in airports, in hotels, restaurants, schools etc). Corona will create more awareness of hygiene products. Here the strong Essity brands will prosper.

The long-term catalyst is the fact that people in the western (rich) socities are living longer and will drive the demand of Essity related products.

Any thoughts about the Q1 report and acquisitions? For me the company seems interesting and boring at the same time Kind of worrying that sales are way lower than Q1 2019. 2020 is naturally a tough comparison.

Essity will have a couple of rough quartals ahead of them. That is given, due to lockdowns and costs concerns driven by mass price increases.

But that said, Essity is doing everything right, and if I want to be in this space I prefer Essity over KMB, which is heavily in debt (as it uses the American way to boost it share price by spending way to much money on share buy backs).

I am bullish on the long-term view of Essity. But owning Essity as you indicated requires patience, which is hard to find among investors these days.

edit: I do like that Essity pursues (‘small’) bolt-on acquisitions, rather than big, as these usually do not have a favorable outcome (especially) for the buyer.

Much has happened since the last post. Over the past three years, Essity has diversified by making numerous acquisitions:

2021

-Full acquisition of ABIGO Medical and Asaleo Care (previously partial ownership).

-Ownership stake in Productos Familia S.A. was increased to 95.8%.

-Acquired sports tape brands Coach, Elastikon, and Zonas from Johnson & Johnson.

-Acquisition of AquaCast Liner, a manufacturer of waterproof cast liners.

-Acquisition of wound care company Hydrofera.

2022

-Acquisition of Legacy Converting, Inc., a wiping products company.

-Acquisition of Modibodi, a leakproof apparel company.

-Acquisition of Knix Wear Inc., a leakproof apparel company.

There have also been divestments. Essity sold its Russian operations in 2023. I wonder if peers KMB and PG have done so yet? The most recent divestment is the sale of the Hong Kong-listed subsidiary Vinda. Essity has owned approximately 50% of Vinda. As I understand it, the tender offer is still awaiting final approval, but if completed, it will bring 19bn SEK into the company’s coffers.

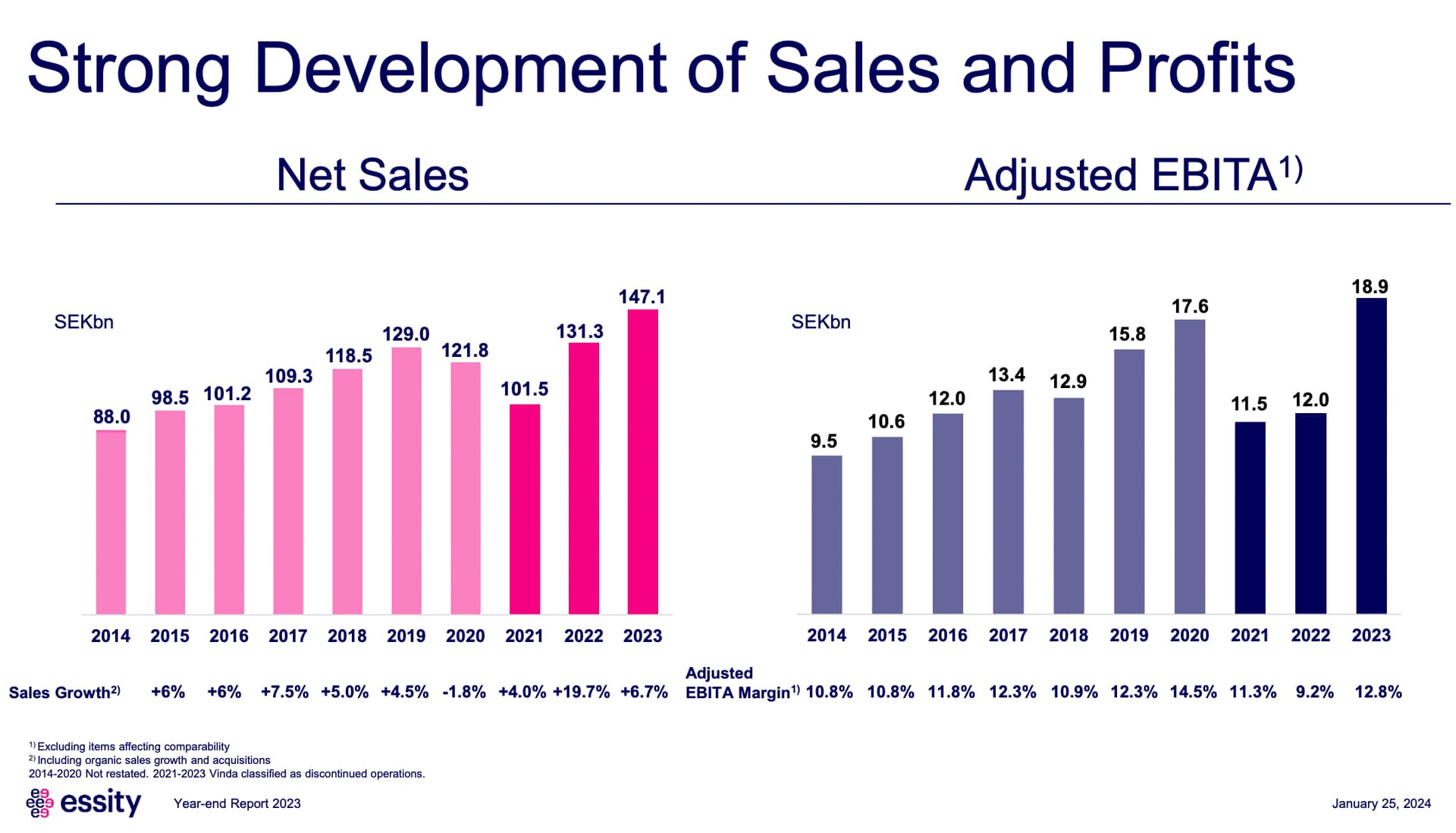

The image of Essity is still easily associated with Lotus, Tena, or Libero. The company’s strategy has been to reduce the share of the toilet paper and diaper business and increase higher-margin new products, mainly through acquisitions. If you consider Kimberly-Clark or P&G too expensive at the moment, Essity is starting to be a noteworthy “hold” stock with significantly more attractive valuation multiples and a reasonable debt profile. ROCE according to the 2023 financial statements was 14.4%. The dividend was increased and is 7.75 SEK.

2023

• Net sales increased 12.1% to SEK 147,147m (131,320). Sales growth, including organic sales growth and

acquisitions, amounted to 6.7%, of which volume accounted for -3.7%, price/mix for 9.5% and acquisitions

for 0.9%.

• Operating profit before amortization of acquisition-related intangible assets (EBITA) increased 68% to SEK 16,607m (9,876)

• Adjusted EBITA increased 57% to SEK 18,898m (12,047) and the adjusted EBITA margin increased 3.6 percentage points to 12.8% (9.2)

• Profit for the period continuing operations increased 84% to SEK 9,517m (5,165)

• Earnings per share continuing operations increased to SEK 13.44 (7.28) and adjusted earnings per share continuing operations increased 51% to SEK 17.56 (11.60)

• Operating cash flow increased 130% to SEK 17,685m (7,680)

• Return on capital employed increased to 14.4% (8.9) and the adjusted return on capital employed increased 5.5 percentage points to 16.4% (10.9)

Essity has very high-quality businesses. The company went public at a valuation that was a bit too high, but the valuation has now settled at reasonable levels. If growth continues, the company’s value should catch up at some point. I would consider it a company with a similar growth profile to Huhtamäki. No major dividend yield as a starting point, but a fairly significant growth option that has been well-realized historically.

Personally, I like companies where the product portfolio remains relatively similar from year to year. It’s nice to build a compounding effect on something that doesn’t need to be reinvented every year.

In Essity’s case, we saw how the consumer ultimately pays for inflation and that strong companies have pricing power.

Essity is a quality company that is boring in a good way, so its news/releases aren’t really followed in real-time. On March 4, it was announced that authorities have approved the sale of the Vinda stake to the bidder. Essity will receive the previously announced 19bn SEK from the sale.

And the dividend (7.75 SEK) goes ex-dividend on Friday, March 22.

Let’s continue the almost dead discussion about a quality company.

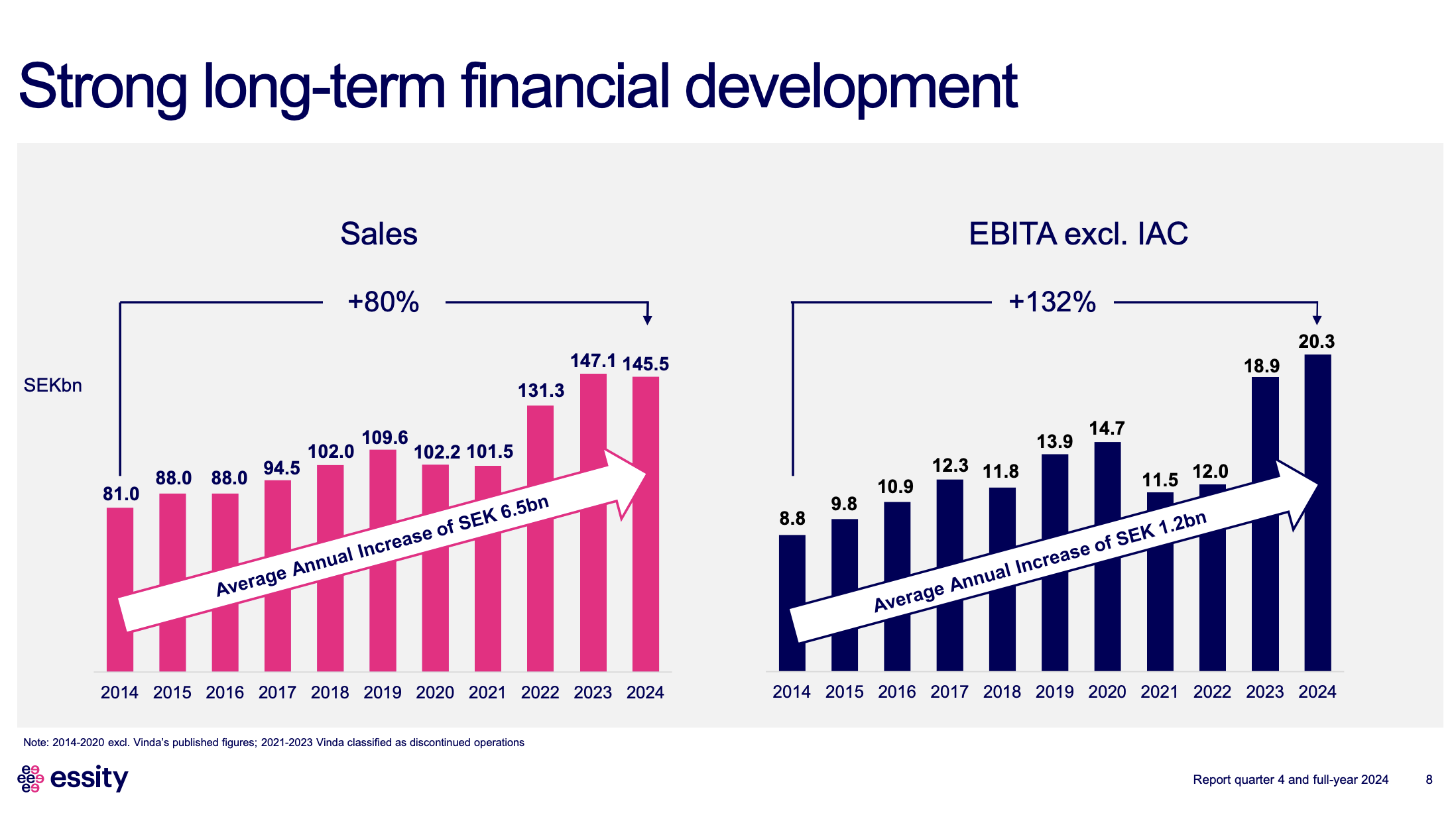

Essity has continued its steady progress. The dividend is growing again and the balance sheet keeps improving. The company is starting to have the strength to either buy back more of its own shares or embark on complementary acquisitions. I would definitely consider it among the best Nordic companies. A deadly boring and profitable company. The strategy to grow from traditional bulk products to higher value-added products has worked. For example, the Health & Medical segment achieved an 18% EBITA margin, which I would consider excellent.