Competitors have been mentioned in the message from @Vuh found in the thread, which contains a table of Enento’s peer group.

I’ve gathered information here about Enento’s competitors.

First, a summary. In a Kauppalehti article from October 2021, the competitive situation is summarized. According to the article, Enento competes, for example, with Dun & Bradstreet and Experian Plc, which has a turnover of over five billion dollars.

Competitive situation in 2015 (prospectus)

Let’s first look at the information from Enento’s 2015 prospectus. This information from the prospectus is now quite outdated, but it also illustrates the volume of corporate restructuring. Many changes have occurred in the competitive environment during Enento/Asiakastieto’s short time on the stock exchange.

(Source:

Prospectus 2015, pages 61-62.)

Corporate restructurings that have occurred since the publication of the prospectus include at least these:

So now Enento’s main competitor is Dun & Bradstreet. Intrum and Lowell compete with Enento in credit information.

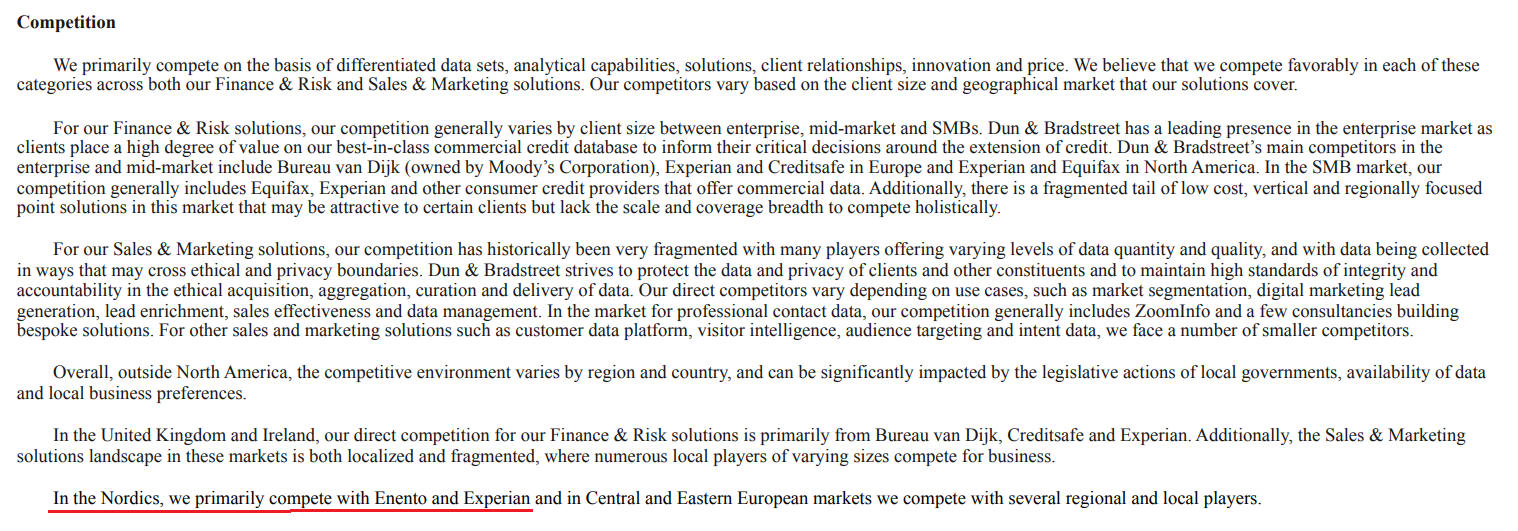

Dun & Bradstreet

Dun & Bradstreet (NYSE:DNB) describes the market’s competitive situation in the 2023 10-K report. (Link: 10-K 2023.pdf)

The company described the Nordic competitive situation with the exact same words in the 2022 10-K report as well. In previous 10-K reports, the Nordic countries were not commented on, as the Bisnode acquisition and DNB’s expansion into the Nordics took place in January 2021.

According to DNB, the main competitors in the Nordics are Enento and Experian, which is also mentioned in the OP peer group referred to at the beginning of the message.

Experian

Experian is listed on the London Stock Exchange (LON:EXPN), but its headquarters are in Dublin, Ireland. According to the 2022 annual report, revenue already exceeded 6 billion.

Report: https://www.experianplc.com/media/4480/experian_ar2022_web.pdf

In addition to Dun & Bradstreet, Experian’s competitors include Equifax Inc (NYSE: EFX) and Fair Isaac Corp (NYSE: FICO).

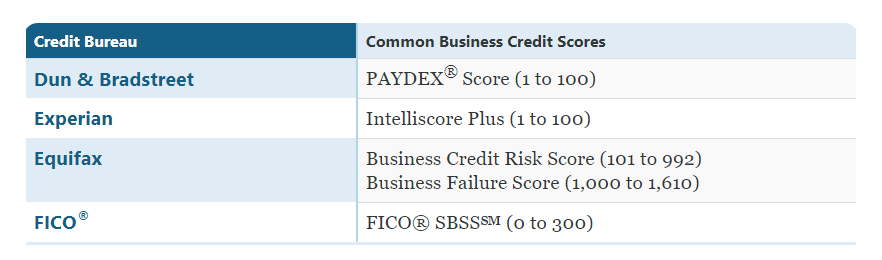

All four companies collect information on the borrowing of corporate clients and share various key figure data with their customers. Among these, the most common in Finland seems to be D&B’s Paydex indicator, which describes payment delays.

The Paydex indicator probably spread to Finland when the Swedish company Bisnode expanded into the Finnish market sometime in the 90s and began offering Dun & Bradstreet’s information services. Bisnode has also published guides in Finnish on interpreting credit information reports: Bisnode - Guide to interpreting international credit reports.pdf

Based on a brief search, I didn’t find references to the Nordic competitive situation in Experian Plc’s reports. Experian’s offices are listed on their website, with locations found in Norway and Denmark, among others, but somewhat surprisingly, Sweden is not on the list. → Contact us | Experian plc

Experian’s cooperation should also be noted here.

In 2014, Experian established the Nordic Credit Alliance (NCA) with Asiakastieto. According to UC’s website, the partnership between UC, Asiakastieto, and Experian provides information on over three million companies and 14 million private individuals in the Nordic countries. → Collaboration - UC

Bankruptcy statistics for Finland, Sweden, Norway, and Denmark are also produced as a collaboration between Enento and Experian. The latest bankruptcy update seems to be from the beginning of last year.

More start-ups and fewer bankruptcies in the Nordics during 2021 than prior to the pandemic - Enento

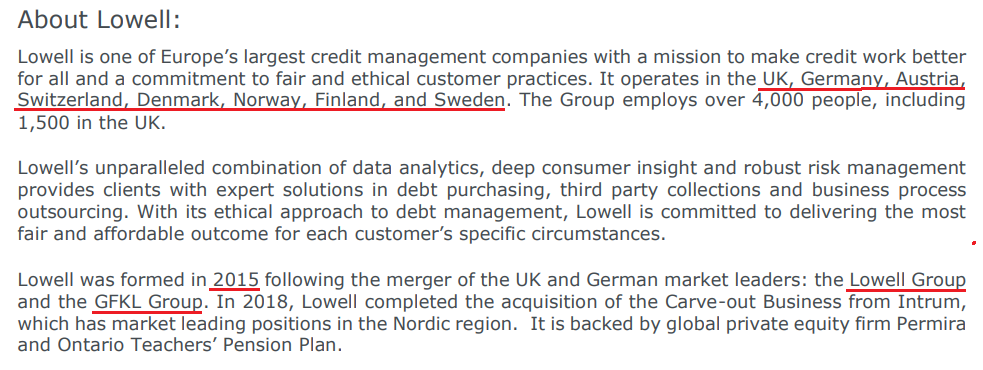

Lowell Ltd

I already mentioned Lowell Ltd at the beginning of the message, so a few more notes on it. According to Lowell’s website, Lowell was formed in 2015 as a result of the merger of two market leaders. The UK market leader Lowell Group and the German GFKL Group merged.

Source: Lowell’s results reports, all of which can be found here: Performance and Governance

Lowell’s parent company is Garfunkelux Holdco 2 S.A. According to the LEI register, subsidiaries of the Luxembourg-based Garfunkelux include Lowell Sweden and Lowell Finland.

If we look at returns, the returns of publicly listed companies have diverged slightly over the last 5 years. FICO has been the best investment. Equifax and Experian have progressed at the same pace. Those who invested in Enento and DNB have fared the worst.

DNB has not met the expectations set by analysts. In February 2023, DNB published its Q4 report. For the fourth quarter, North American revenue grew by 1.4%, but conversely, international revenue fell by 5.6% to 160.1 million dollars.